1. Introduction: The Quiet Force Behind Most Millionaires

When people imagine wealth, they often picture entrepreneurs building billion-dollar startups, celebrities signing massive contracts, or investors making lucky bets on hot stocks. While these stories capture attention, they are not how most wealthy individuals actually build their fortunes.

Research across the U.S., UK, Canada, Australia, and Western Europe consistently shows that the majority of millionaires are:

- Teachers

- Engineers

- Nurses

- Accountants

- Small business owners

- Corporate professionals

Not celebrities. Not lottery winners. Not tech moguls.

So how did they become wealthy?

Through compound interest.

Compound interest is the financial equivalent of gravity. It works silently, continuously, and relentlessly—regardless of whether you understand it or not. The difference is whether it is working for you or against you.

It doesn’t require:

- High income

- Financial genius

- Perfect market timing

- Risky speculation

What it does require:

- Time

- Consistency

- Discipline

- Patience

Albert Einstein is often quoted as calling compound interest the “eighth wonder of the world.” Whether or not he actually said this, the concept itself deserves the title.

“He who understands it, earns it. He who doesn’t, pays it.”

That quote perfectly summarizes financial reality. Those who understand compounding grow wealth quietly and steadily. Those who don’t end up paying compounding through debt, missed opportunities, and inflation erosion.

This article will explain:

- What compound interest truly means

- Why time matters more than money

- How small, boring investments can become millions

- Where and how to invest

- How to avoid common traps

- A step-by-step roadmap to apply this in real life

By the end, you’ll understand why compound interest is not just a financial concept—it’s a life strategy.

2. What Is Compound Interest? (In Simple Terms)

Let’s define compound interest clearly and simply.

Compound interest is the process where interest is earned not only on the original investment but also on previously earned interest, creating exponential growth over time.

In other words, your money starts earning money, and then that money starts earning money too.

Compound Interest Explained for Beginners

This creates a snowball effect—just like rolling a small snowball down a hill. At first, it grows slowly. But as it rolls further, it becomes larger, heavier, and grows faster.

Step-by-Step Breakdown:

- You invest money.

- That money earns interest or returns.

- The interest gets added to your balance.

- Your new, larger balance earns interest.

- The cycle repeats—over and over.

Simple Example:

Let’s say you invest $1,000 at an annual return of 10%.

- End of Year 1:

$1,000 × 10% = $100 interest → Balance = $1,100 - End of Year 2:

$1,100 × 10% = $110 interest → Balance = $1,210 - End of Year 3:

$1,210 × 10% = $121 interest → Balance = $1,331

Notice:

- Year 1 interest = $100

- Year 2 interest = $110

- Year 3 interest = $121

You’re earning interest not just on your original $1,000, but also on the interest itself.

That’s compounding.

For a deeper explanation of how compounding works in finance, you can read this detailed guide on compound interest explained.

3. The Difference Between Simple Interest and Compound Interest

Understanding this difference is critical to understanding wealth creation.

Simple Interest

Simple interest means you earn interest only on your original investment, not on previously earned interest.

Formula:

Simple Interest = Principal × Rate × Time

Example:

- Principal: $1,000

- Rate: 10%

- Time: 10 years

Interest = $1,000 × 10% × 10 = $1,000

Final amount = $1,000 + $1,000 = $2,000

Compound Interest

Compound interest means you earn interest on:

- Your original investment and

- All interest that has already been earned.

Formula:

Compound Interest = P × (1 + r)ⁿ

Where:

- P = Principal (initial investment)

- r = Annual rate of return (as a decimal)

- n = Number of years

Example:

- P = $1,000

- r = 10% = 0.10

- n = 10

Final amount = $1,000 × (1.10)¹⁰ ≈ $2,593

That’s nearly $600 more than simple interest—without investing any extra money.

Now extend this to 20, 30, or 40 years, and the difference becomes tens or hundreds of thousands of dollars.

4. Why Time Is More Powerful Than Money

Most people believe that investing more money is the key to building wealth. While money helps, time is far more powerful.

Time is the most valuable asset in compounding because compounding is exponential, not linear.

Let’s Compare Two People:

Person A:

- Starts investing at age 25

- Invests $200 per month

- Stops at age 35 (invests for 10 years)

- Total invested = $200 × 12 × 10 = $24,000

Person B:

- Starts investing at age 35

- Invests $200 per month

- Continues until age 65 (invests for 30 years)

- Total invested = $200 × 12 × 30 = $72,000

Assume both earn 10% annually.

By age 65:

- Person A ends up with more money than Person B—even though Person B invested three times as much.

Why?

Because Person A gave their money an extra 10 years to compound.

Key Insight:

Time does more work than money.

Every dollar invested early works harder than a dollar invested later. This is why starting early—even with small amounts—can outperform starting late with large amounts.

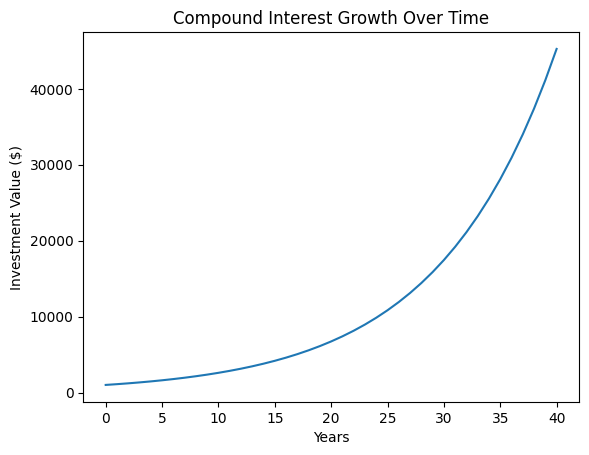

5. The Mathematical Magic: How Compounding Works

Let’s visualize how compounding works over time using a single $1,000 investment at 10% annually.

| Year | Balance |

|---|---|

| 0 | $1,000 |

| 5 | $1,611 |

| 10 | $2,593 |

| 15 | $4,177 |

| 20 | $6,727 |

| 25 | $10,834 |

| 30 | $17,449 |

| 35 | $28,102 |

| 40 | $45,259 |

Notice:

- It takes 20 years to grow from $1,000 to about $6,727.

- But in the next 20 years, it grows from $6,727 to over $45,000.

This happens because the base keeps getting larger, and each percentage return is applied to a bigger amount.

This is why wealth often seems to “appear suddenly” later in life, even though it’s the result of decades of quiet, boring compounding.

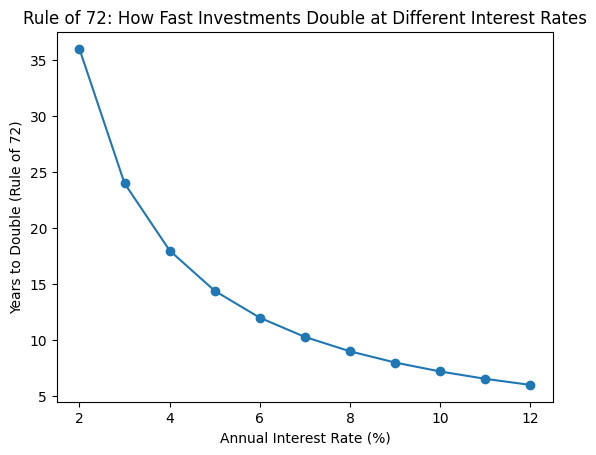

6. The Rule of 72: A Shortcut to Growth

The Rule of 72 is a simple mental math shortcut to estimate how long it takes for your money to double.

Formula:

Years to double = 72 ÷ Annual rate of return

The Rule of 72 is a quick way to estimate how long it takes for an investment to double. Simply divide 72 by the annual interest rate.

Examples:

- At 8% return:

72 ÷ 8 = 9 years - At 10% return:

72 ÷ 10 = 7.2 years - At 12% return:

72 ÷ 12 = 6 years

This rule helps you quickly compare investment opportunities and understand the power of higher returns over time.

For example:

- Money earning 4% doubles in ~18 years.

- Money earning 10% doubles in ~7 years.

That difference compounds massively over decades.

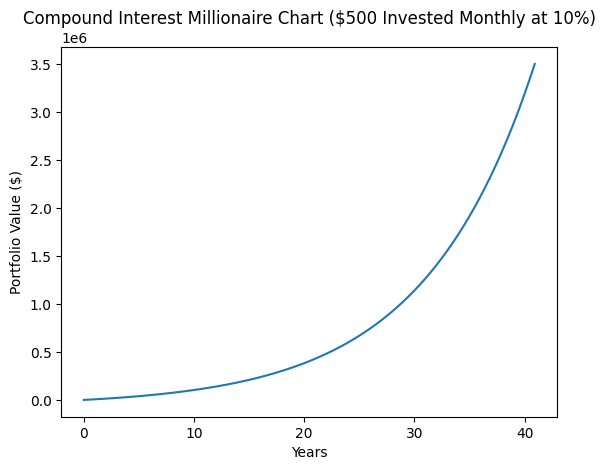

7. Real-Life Example: From $100 a Month to $1 Million

Let’s apply compounding to a realistic, everyday scenario.

Scenario 1:

- Monthly investment: $100

- Annual return: 10%

- Time horizon: 40 years

Total invested = $100 × 12 × 40 = $48,000

Final value ≈ $530,000

Scenario 2:

- Monthly investment: $200

- Annual return: 10%

- Time horizon: 40 years

Total invested = $200 × 12 × 40 = $96,000

Final value ≈ $1,060,000

That’s how ordinary, middle-income individuals can become millionaires—without inheritance, without business ownership, and without high salaries.

The key is:

- Starting early

- Being consistent

- Letting compounding do the work

8. Starting Early vs. Starting Late: A Wealth Gap Study

Let’s compare two fictional individuals to illustrate the power of starting early.

Emma (Early Starter):

- Starts investing at age 22

- Invests $250 per month

- Stops at age 32

- Total invested = $250 × 12 × 10 = $30,000

Noah (Late Starter):

- Starts investing at age 32

- Invests $250 per month

- Continues until age 65

- Total invested = $250 × 12 × 33 = $99,000

Assuming a 10% return:

- Emma ends up with more money than Noah—even though she invested less than one-third of what Noah invested.

Why?

Because Emma gave her money 10 extra years to compound.

Key Lesson:

The cost of delaying investing is greater than almost any other financial mistake.

9. The Psychology of Compounding: Why Most People Miss It

If compound interest is so powerful, why don’t more people take advantage of it?

Because it conflicts with human psychology.

Humans are wired for:

- Immediate gratification

- Visible progress

- Short-term rewards

Compounding offers:

- Delayed gratification

- Invisible progress

- Long-term rewards

In the early years:

- Progress feels slow

- Balances grow gradually

- Results seem insignificant

This causes people to:

- Stop investing

- Chase “get rich quick” schemes

- Panic during market downturns

- Withdraw money early

But the people who build wealth are the ones who:

- Stay consistent when progress feels boring

- Continue investing during market crashes

- Ignore short-term noise

- Trust the long-term process

Wealth is not built by intelligence—it is built by behavior.

10. Where to Earn Compound Interest (Best Asset Classes)

Not all financial assets compound equally. Here are the most powerful compounding vehicles:

- Stock Market (Index Funds & ETFs)

- Dividend-Paying Stocks

- Retirement Accounts

- Real Estate

- High-Yield Savings Accounts (for safety, not growth)

Let’s explore each.

11. Compound Interest in the Stock Market

Historically, stock markets in developed countries have returned:

- 10% annually according to research on historical stock market returns

- ~8–10% in most developed markets

This return comes from:

- Capital appreciation (stock prices rising)

- Dividends (cash payments to shareholders)

When you:

- Stay invested

- Reinvest dividends

- Avoid panic selling

You experience true compounding.

Example:

$10,000 invested in a broad U.S. stock market index fund at 10%:

- After 10 years: ~$25,937

- After 20 years: ~$67,275

- After 30 years: ~$174,494

- After 40 years: ~$452,592

Add monthly contributions, and the numbers grow exponentially.

12. Dividend Reinvestment: The Accelerator Effect

Dividends are periodic cash payments that companies make to shareholders from their profits.

When you reinvest dividends:

- You buy more shares.

- Those shares generate more dividends.

- Those dividends buy even more shares.

This creates a self-reinforcing compounding loop.

Over long periods, dividend reinvestment has accounted for:

- 30–50% of total stock market returns in many markets.

It is one of the most powerful—and most overlooked—wealth accelerators.

13. Compound Interest with Retirement Accounts

Governments in Tier-1 countries offer tax-advantaged retirement accounts that dramatically enhance compounding.

United States:

- 401(k) – Employer-sponsored retirement plan

- IRA (Traditional & Roth) – Individual retirement accounts

United Kingdom:

- ISA – Individual Savings Account

- SIPP – Self-Invested Personal Pension

Canada:

- RRSP – Registered Retirement Savings Plan

- TFSA – Tax-Free Savings Account

Australia:

- Superannuation – Mandatory retirement savings system

These accounts:

- Allow investments to grow tax-free or tax-deferred

- Reduce or eliminate annual tax drag

- Increase long-term compounding power

Example:

$6,000 invested annually for 30 years at 10%:

- In a taxable account: ≈ $988,000

- In a tax-advantaged account: ≈ $1,130,000+

That’s over $140,000 more, purely from better compounding conditions.

Retirement investment regulations and tax benefits are overseen by financial regulators like the U.S. Securities and Exchange Commission

14. Compound Interest with Index Funds and ETFs

Index funds and Exchange-Traded Funds (ETFs) are among the most effective compounding tools because they are:

- Low-cost (low expense ratios)

- Diversified (spread risk across many companies)

- Consistent (match market performance)

- Evidence-based (outperform most active managers long-term)

Examples:

- S&P 500 Index Fund

- Total Stock Market Fund

- Global Equity ETF

Lower fees = more money stays invested = faster compounding.

A 1% difference in annual fees over 40 years can reduce your final wealth by 25–30% or more.

15. Compound Interest with Real Estate

Real estate compounds in three powerful ways:

- Property Appreciation – The value of the property increases over time.

- Rental Income – Tenants pay rent, generating cash flow.

- Mortgage Paydown – Each payment reduces your debt, increasing your equity.

When rental income is reinvested and properties appreciate, you experience a form of compounding.

Example:

- Buy a rental property.

- Use rental income to pay down the mortgage.

- Property value increases.

- Equity grows.

- Use equity to purchase another property.

This creates a cycle of:

Assets generating assets.

16. The Dark Side: How Compound Interest Works Against You (Debt)

Compound interest is neutral—it works in both directions.

If you earn it, you build wealth.

If you pay it, you lose wealth.

High-interest debt compounds against you, especially:

- Credit cards

- Payday loans

- High-interest personal loans

Example:

$5,000 credit card balance at 20% APR:

- Making only minimum payments could take 20+ years to repay.

- Total interest paid could exceed $7,000—more than the original balance.

Debt uses the same compounding force—but in reverse.

That’s why eliminating high-interest debt is a financial emergency, not just a budgeting issue.

17. Inflation vs. Compounding: The Hidden Battle

Inflation reduces the purchasing power of money over time, as shown in long-term inflation data published by the Federal Reserve

If inflation is 3% annually, $100 today will only buy what $74 buys in 10 years.

If your money earns:

- 1% in a savings account

- Inflation is 3%

Your real return is:

1% – 3% = –2%

That means your money is losing value every year—even though your account balance may be rising.

Compounding only builds real wealth when your returns exceed inflation.

That’s why:

- Cash is safe but not wealth-building.

- Investing is essential for long-term financial survival.

18. How Much Do You Need to Invest to Become a Millionaire?

Let’s answer this practically.

Assumptions:

- 10% annual return

- 40-year investment horizon

| Monthly Investment | Final Value |

|---|---|

| $100 | ~$530,000 |

| $150 | ~$795,000 |

| $200 | ~$1,060,000 |

| $300 | ~$1,590,000 |

| $500 | ~$2,650,000 |

Becoming a millionaire is not about earning millions—it’s about consistently investing hundreds.

How Small Investments Can Turn Into Millions

Even small monthly investments can grow dramatically over time thanks to compound interest. Consistently investing a fixed amount every month allows returns to compound and accelerate wealth growth.

19. Step-by-Step Blueprint to Harness Compound Interest

Here’s your actionable roadmap:

Step 1: Start Immediately

Even $25 or $50 per month is enough to begin. Waiting costs more than starting small. Before investing aggressively, it’s wise to first build a solid emergency fund to protect yourself from unexpected expenses.

Step 2: Automate Investments

Set up automatic transfers to your investment accounts so investing happens without willpower.

Step 3: Use Tax-Advantaged Accounts First

Maximize employer matches, then contribute to IRAs, ISAs, RRSPs, or Superannuation.

Step 4: Invest in Low-Cost Index Funds

Avoid high-fee funds and stock picking. Use broad market funds.

Step 5: Reinvest All Dividends

Don’t spend dividends. Let them buy more shares.

Step 6: Stay Invested Through Market Volatility

Market crashes are not failures—they are opportunities to buy more at lower prices.

Step 7: Increase Contributions Over Time

As income rises, increase your investments. Lifestyle inflation kills compounding—avoid it.

20. Common Mistakes That Kill Compounding

Avoid these at all costs:

- Starting Too Late

- Stopping During Market Crashes

- Withdrawing Early

- Chasing High-Risk Speculation

- Paying High Fees

- Not Reinvesting Dividends

- Keeping Too Much in Cash

- Ignoring Inflation

- Carrying High-Interest Debt

- Trying to Time the Market

Each mistake interrupts the compounding process—and costs you years or decades of growth.

21. How Technology Makes Compounding Easier Than Ever

Modern technology has democratized investing:

- Robo-advisors automatically manage portfolios.

- Fractional shares allow investing with small amounts.

- Automatic payroll deductions make investing effortless.

- Mobile investing apps provide access anywhere.

- Global ETFs allow worldwide diversification.

You no longer need:

- A financial advisor

- A large capital base

- Advanced financial knowledge

Compounding is now accessible to almost everyone.

22. Case Study: Ordinary People Who Became Millionaires

Case Study 1: The Teacher

- Invested $300/month in index funds for 35 years.

- Never picked stocks.

- Never timed the market.

- Retired with over $1.8 million.

Case Study 2: The Engineer

- Maxed out retirement accounts.

- Reinvested dividends.

- Stayed invested through three market crashes.

- Retired with $3+ million.

Case Study 3: The Nurse

- Started at age 23.

- Increased investments with every raise.

- Avoided lifestyle inflation.

- Retired early with financial independence.

None of these people were wealthy to start.

None had insider knowledge.

All used the same force: compound interest.

23. FAQs About Compound Interest

Q: Can compounding work with small amounts?

Yes. In fact, small amounts are the foundation of compounding.

Q: What rate of return should I expect?

Historically, global stock markets have returned 8–10% annually over long periods.

Q: Is compounding guaranteed?

No. Markets fluctuate. But long-term compounding across diversified assets has been one of the most reliable wealth-building forces in history.

Q: What if I already started late?

Start now. The second-best time to invest is today.

Q: Is compounding better than business income?

They serve different purposes. But compounding is often more reliable, less stressful, and more predictable than entrepreneurship.

24. Final Thoughts: Why Compounding Is the Closest Thing to a Financial Superpower

Compound interest is not just a financial concept—it is a law of wealth creation.

It rewards:

- Patience over urgency

- Discipline over emotion

- Consistency over intensity

- Long-term thinking over short-term gratification

You don’t need:

- A six-figure income

- A finance degree

- Perfect timing

- Risky bets

You need:

- Time

- Consistency

- Low-cost investing

- Emotional discipline

And most importantly, you need to start.

Because the greatest enemy of compound interest is not market crashes—it’s delay.

Every year you wait, you give up thousands—or hundreds of thousands—of dollars your future self could have had.

So start today.

Invest consistently.

Let time do the heavy lifting.

Because compound interest doesn’t just grow money—it builds freedom.