1. Introduction: Why Safe Investing Matters More Than Ever

We live in a world of financial uncertainty.

Housing prices continue to rise faster than wages in most Tier-1 countries. Healthcare costs are climbing. University education is more expensive than ever. Government pension systems are under pressure due to aging populations. Inflation quietly erodes the purchasing power of money sitting in savings accounts.

At the same time, investing has become easier than ever. With a smartphone and a few clicks, anyone can buy stocks, ETFs, cryptocurrencies, or other assets. Yet this ease of access has created a paradox: more opportunity, but more emotional risk.

People are overwhelmed by:

- Market crashes and sudden downturns

- Sensational financial news

- Influencer-driven investment hype

- Fear of missing out (FOMO)

- Fear of losing money

As a result, many people:

- Delay investing altogether

- Chase trends

- Buy at market peaks

- Panic sell during downturns

This behavior doesn’t just reduce returns — it destroys wealth.

That’s why safe, systematic investing matters more than ever. And that’s exactly what Dollar-Cost Averaging (DCA) offers.

DCA removes emotion from investing. It replaces guesswork with discipline. It transforms investing from a stressful decision into a predictable habit.

This article will explain:

- What DCA is

- Why it works

- How to use it

- When it’s most powerful

- When it may not be ideal

By the end, you’ll understand not only how to use DCA, but why it’s one of the safest and most reliable wealth-building strategies ever created. Dollar-Cost Averaging (DCA) is not just a strategy — it’s a long-term system that protects investors from emotional mistakes and poor timing decisions.

2. What Is Dollar-Cost Averaging (DCA)?

Simple Definition

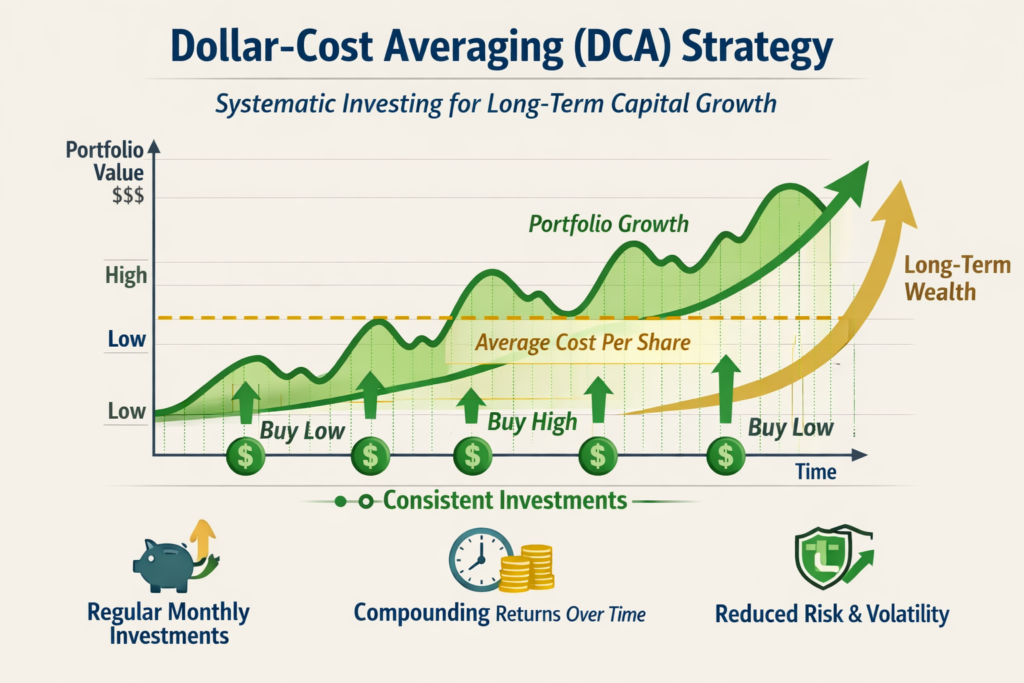

Dollar-Cost Averaging (DCA) is an investment strategy where you invest a fixed amount of money at regular intervals, regardless of whether the market is rising, falling, or moving sideways.

Instead of trying to guess the best time to invest, you invest consistently — weekly, biweekly, or monthly — over a long period of time.

Expanded Definition

Dollar-Cost Averaging is a method of spreading investment risk over time by making consistent, periodic investments into the same asset or portfolio. This reduces the impact of market volatility and lowers the average price paid per unit of investment over time.

At its core, Dollar-Cost Averaging (DCA) is a form of systematic investing that removes randomness and replaces it with structured, repeatable investment behavior.

Why the Name?

- Dollar: Refers to investing a fixed amount of money (not a fixed number of shares).

- Cost: Refers to the price you pay for the asset.

- Averaging: Refers to the process of smoothing out your purchase price over time.

Example (Simple)

You invest $500 every month into a stock market index fund.

- When prices are high → You buy fewer shares.

- When prices are low → You buy more shares.

Over time, this results in a lower average cost per share than if you invested all your money at once at a random point in time.

This strategy does not attempt to predict the market. It simply participates in the market consistently.

3. Key Terms Explained (In Plain English)

Before we go deeper, let’s clarify some important terms used throughout this article.

1. Investment

An investment is the act of putting money into an asset (like stocks, bonds, or real estate) with the expectation that it will grow in value or generate income over time.

2. Asset

An asset is something you own that has value and can produce income or appreciation. Examples include stocks, bonds, real estate, and businesses.

3. Stock

A stock represents ownership in a company. When you buy a stock, you own a small piece of that company.

4. ETF (Exchange-Traded Fund)

An ETF is a basket of many stocks or bonds bundled together and traded like a stock. For example, an S&P 500 ETF holds shares of 500 large U.S. companies.

5. Mutual Fund

A mutual fund is similar to an ETF, but it is typically bought and sold directly through a fund provider, often at the end of the trading day.

6. Index Fund

An index fund is a type of ETF or mutual fund that tracks a specific market index, such as the S&P 500 or a global stock market index.

7. Volatility

Volatility refers to how much and how quickly an asset’s price changes. High volatility means large price swings; low volatility means more stable prices.

8. Compounding

Compounding is the process where your investment earnings generate their own earnings over time. This creates exponential growth.

9. Average Cost Basis

Your average cost basis is the average price you paid per share over time. DCA lowers this by buying more shares when prices are low.

4. Why Humans Are Bad at Timing the Market

This behavior is well documented in behavioral finance principles, which show that emotions often override rational investment decisions.

The biggest obstacle to successful investing is not a lack of money, education, or opportunity — it is human psychology.

How the Brain Works

Humans evolved to:

- Seek pleasure

- Avoid pain

- Follow the crowd

In financial markets, this translates to:

- Buying when prices are rising (pleasure + FOMO)

- Selling when prices are falling (pain avoidance)

- Following what others are doing (herd behavior)

Unfortunately, this behavior leads to buying high and selling low — the exact opposite of successful investing.

Example: The Boom-Bust Cycle

Let’s look at a common pattern:

- Market rises → News is positive → People feel confident → They invest.

- Market peaks → Optimism is extreme → Everyone is buying.

- Market crashes → Fear takes over → People panic and sell.

- Market bottoms → News is negative → People avoid investing.

- Market recovers → Those who sold missed the recovery.

This cycle repeats again and again.

Why Market Timing Rarely Works

Even professional investors struggle to time the market. Research consistently shows:

- Most actively managed funds underperform the market over long periods.

- Missing just a handful of the market’s best days dramatically reduces long-term returns.

- The best days often occur immediately after the worst days — when investors are most afraid.

According to long-term market data from the Standard & Poor’s, missing just a handful of the best-performing days can significantly reduce long-term returns. Historical S&P 500 return data is publicly available via Slickcharts.

DCA Solves This Problem

Dollar-Cost Averaging removes the need to time the market. Instead of asking, “Is now a good time to invest?” you simply invest — every time.

This eliminates emotional decision-making and replaces it with automation and discipline.

5. How DCA Works (With Detailed Numerical Examples)

Let’s explore exactly how DCA works using detailed numbers.

Scenario 1: Monthly Investing in a Volatile Market

You invest $1,000 per month into a fund for six months.

| Month | Price per Share | Investment | Shares Bought |

|---|---|---|---|

| Jan | $100 | $1,000 | 10 |

| Feb | $80 | $1,000 | 12.5 |

| Mar | $70 | $1,000 | 14.29 |

| Apr | $90 | $1,000 | 11.11 |

| May | $110 | $1,000 | 9.09 |

| Jun | $120 | $1,000 | 8.33 |

Calculations

- Total invested: $6,000

- Total shares: 65.32

- Average cost per share: $6,000 ÷ 65.32 ≈ $91.85

Even though the final price is $120, your average purchase price is much lower because you bought more shares when prices were low.

Scenario 2: Investing All at Once (Lump Sum)

Now let’s say you invested the full $6,000 in January at $100 per share.

- Shares bought: 60

- Average cost per share: $100

You would end up with fewer shares and a higher cost basis than with DCA.

Because contributions occur at different price levels, DCA acts as a volatility smoothing strategy in unpredictable markets.

6. DCA vs Lump-Sum Investing: A Deep Comparison

While lump-sum investing may produce higher raw returns in strong bull markets, DCA often improves risk-adjusted returns by lowering emotional and timing risk.

Lump-Sum Investing

Definition: Investing all available capital at once.

Advantages:

- Historically higher expected returns.

- Money is exposed to the market sooner, allowing more time for compounding.

Disadvantages:

- High emotional stress.

- Risk of investing just before a market downturn.

- Difficult for most people to execute confidently.

Dollar-Cost Averaging

Definition: Investing gradually over time.

Advantages:

- Reduces emotional stress.

- Lowers timing risk.

- Encourages consistency and discipline.

- Makes investing accessible to people with limited cash.

Disadvantages:

- May result in slightly lower returns in rising markets.

- Slower initial growth.

Which Is Better?

From a purely mathematical perspective, lump-sum investing often wins on average because markets tend to rise over time. However, investing is not just about math — it’s about behavior.

The best strategy is the one you can stick to during:

- Market crashes

- Economic recessions

- Periods of fear and uncertainty

For most people, that strategy is DCA.

If you’re still deciding between investing approaches, read our detailed comparison on Growth vs Value Investing.

7. The Psychology Behind DCA Success

The reason Dollar-Cost Averaging works so well is that it aligns investing with human psychology instead of fighting against it. Dollar-Cost Averaging works because it aligns with how humans actually behave.

1. Reduces Fear

When you invest regularly, no single investment decision feels overwhelming. You never feel like you’re risking everything at once.

2. Builds Discipline

Investing becomes automatic — like paying rent or utilities. This habit is far more powerful than motivation.

3. Eliminates Regret

You won’t regret investing “too early” or “too late” because you invest continuously.

4. Prevents Emotional Trading

Since your investments are automated, you’re less likely to panic sell or chase market trends.

This psychological advantage is just as important as the financial advantage. Because it requires minimal active decision-making, Dollar-Cost Averaging supports passive wealth building without constant monitoring or emotional interference.

8. Why DCA Is Ideal for Tier-1 Economies

In Tier-1 countries, most people:

- Receive income regularly (monthly or biweekly).

- Have access to employer-sponsored retirement plans.

- Have long life expectancies (often 80+ years).

- Face rising living costs and uncertain government pensions.

These conditions make long-term, systematic investing essential.

Country-Specific Examples

United States

- 401(k) contributions are automatically deducted from paychecks.

- Employer matching encourages regular investing.

- IRAs allow monthly contributions.

United Kingdom

- Workplace pensions are funded monthly by both employers and employees.

- ISAs allow regular, tax-free investing.

Canada

- TFSAs and RRSPs support monthly investing.

- Employer pensions often follow DCA principles.

Australia

- Superannuation contributions are mandatory and invested regularly.

Europe

- Many countries use pension funds and personal investment plans based on monthly contributions.

All of these systems are essentially built-in DCA mechanisms.

9. How DCA Protects You During Market Crashes

Historically, Dollar-Cost Averaging (DCA) has performed exceptionally well during periods of extreme volatility and market crashes. Market crashes are emotionally devastating — but financially, they are often the best time to invest.

Without DCA

During crashes, many investors:

- Stop investing.

- Sell their investments.

- Wait for “certainty” before re-entering.

This behavior locks in losses and misses recoveries.

With DCA

When you continue investing during downturns:

- You buy more shares at lower prices.

- Your average cost basis decreases.

- Your future returns increase when the market recovers.

Example: 2008 Financial Crisis

Markets dropped more than 50%. Investors who stopped investing missed one of the strongest bull markets in history. Those who continued DCA accumulated shares at deeply discounted prices and experienced massive long-term gains.

The same pattern repeated in:

- The dot-com crash (2000–2002)

- The COVID crash (2020)

- The inflation-driven bear market (2022)

10. The Mathematics of Dollar-Cost Averaging

Over decades, this approach supports steady long-term capital growth by combining consistent contributions with market appreciation. Let’s explore the mathematical foundation of DCA.

Key Concepts

1. Average Cost Basis

The average price you pay per share over time.

2. Volatility

Price fluctuations create opportunities to buy more shares at lower prices.

3. Compounding

Returns generate returns over time, accelerating growth.

Example: Compounding with DCA

If you invest $500 per month at an average annual return of 8%, here’s what happens:

| Years | Total Invested | Portfolio Value |

|---|---|---|

| 10 | $60,000 | ~$91,000 |

| 20 | $120,000 | ~$295,000 |

| 30 | $180,000 | ~$745,000 |

| 40 | $240,000 | ~$1,700,000 |

This growth is driven by:

- Consistent contributions.

- Market growth.

- Compounding returns.

The compounding effect over time is what transforms small monthly contributions into significant long-term wealth.

11. How to Start DCA in Stocks, ETFs, and Mutual Funds

When automated properly, DCA becomes a powerful automated investing strategy that operates without requiring constant attention.

Step 1: Choose an Investment Account

Depending on your country, this may include:

- Brokerage account

- Retirement account (401(k), IRA, ISA, TFSA, RRSP, Superannuation)

Step 2: Choose Your Investments

Focus on:

- Broad market index funds.

- Low-cost ETFs.

- Diversified portfolios.

Avoid:

- Speculative assets.

- High-fee products.

- Investments you don’t understand.

Step 3: Set a Fixed Contribution

Choose a sustainable amount:

- $50, $100, $500, or more — depending on your income.

Step 4: Automate

Set up automatic transfers so your investments happen without manual effort.

Step 5: Stay Consistent

Ignore short-term market noise. Do not pause during downturns. Do not chase trends.

12. DCA with Retirement Accounts (401(k), IRA, ISA, TFSA, RRSP, Superannuation)

In retirement accounts, DCA functions as a powerful retirement accumulation method that builds assets steadily over decades.

United States

- 401(k): Contributions deducted automatically from your paycheck.

- IRA: Monthly or annual contributions with tax advantages.

United Kingdom

- Workplace pensions: Monthly contributions from both employer and employee.

- ISAs: Monthly investments into tax-free accounts.

Canada

- TFSA: Tax-free growth and withdrawals.

- RRSP: Tax-deferred growth with retirement focus.

Australia

- Superannuation: Mandatory employer contributions invested over decades.

Europe

- National pension systems and private retirement accounts often use monthly investing models.

These systems are essentially automated DCA machines.

13. How Much Should You Invest Each Month?

There is no perfect number — only a sustainable number.

General Guideline

Invest 10%–20% of your income if possible.

But consistency matters more than the exact percentage.

Examples

- A student investing $50 per month.

- A professional investing $500 per month.

- A high-income earner investing $2,000 per month.

All of these can succeed — if they remain consistent.

Increasing Contributions Over Time

As your income grows, your contributions should grow too. This accelerates wealth building without increasing lifestyle pressure.

14. Common Mistakes That Ruin DCA

Maintaining portfolio discipline is essential for DCA to work effectively over multiple market cycles.

Mistake 1: Stopping During Market Downturns

This destroys the core benefit of DCA — buying more when prices are low.

Mistake 2: Constantly Changing Investments

Frequent switching increases fees and disrupts compounding.

Mistake 3: Trying to Time the Market

Adding complexity reintroduces emotion and risk.

Mistake 4: Not Rebalancing

Over time, your asset allocation may drift. Periodic rebalancing keeps your risk aligned with your goals.

Many investors make avoidable errors — which we explain in Top Investing Myths That Are Keeping You Poor (2026 Guide).

15. Advanced DCA Strategies

1. Value Averaging

Instead of investing a fixed amount, you target a fixed portfolio value increase each period. This can enhance returns but requires more management.

2. Dynamic DCA

You invest more during downturns and less during rallies, while maintaining a base contribution.

3. Windfall Investing

Invest bonuses, tax refunds, or inheritances as lump sums while continuing regular DCA.

16. Real-Life Case Studies

Case Study 1: The 30-Year Investor

Sarah invests $500 per month from age 25 to 55 in an index fund earning 8% annually.

- Total invested: $180,000

- Ending value: ~$745,000

She never timed the market. She simply stayed consistent.

Case Study 2: The Crash Investor

James invested through the 2008 crash, the COVID crash, and the 2022 bear market.

Each downturn felt terrifying — but each one dramatically increased his long-term returns because he continued buying.

17. DCA During Inflation, Recessions, and High Interest Rates

Inflation

Inflation reduces the value of cash. Investing through DCA helps your money grow faster than inflation over time. During inflationary environments, Dollar-Cost Averaging ensures that capital continues working instead of losing purchasing power in cash.

Official inflation statistics can be tracked through the U.S. Bureau of Labor Statistics.

Recessions

Recessions create market downturns — which create buying opportunities for DCA investors.

High Interest Rates

High interest rates often reduce stock prices, increasing the number of shares you can buy with each investment.

For a complete macroeconomic breakdown, see our guide on How to Start Investing in 2026.

18. DCA for Beginners vs Experienced Investors

Beginners

- Use simple index funds.

- Automate contributions.

- Avoid complexity.

Experienced Investors

- Combine DCA with asset allocation strategies.

- Use tax-loss harvesting.

- Rebalance periodically.

But the core principle remains the same: consistent investing over time.

19. How Technology Makes DCA Easier Than Ever

Modern platforms offer:

- Automatic recurring investments.

- Fractional shares.

- Robo-advisors.

- Low-cost ETFs.

- Real-time portfolio tracking.

This removes barriers and makes professional-quality investing accessible to everyone.

20. When DCA Might Not Be the Best Strategy

Lump-Sum May Be Better When:

- You receive a large inheritance.

- You’re investing during a major market crash.

- You have a very long time horizon and high emotional tolerance.

Even then, many investors prefer to DCA for emotional comfort.

21. Final Thoughts: Why DCA Builds Wealth Safely and Reliably

Dollar-Cost Averaging is not exciting. It does not promise overnight riches. It does not rely on luck or genius.

Instead, it relies on:

- Time

- Consistency

- Discipline

- Emotional stability

And these four forces — not timing, not speculation, not prediction — are what actually build wealth.

If you want a strategy that:

- Works in bull markets

- Works in bear markets

- Works during inflation

- Works during recessions

- Works for beginners and experts alike

Then Dollar-Cost Averaging is one of the safest and most reliable long-term investing strategies ever created.

Start small. Stay consistent. Trust the process. Let time and compounding do the heavy lifting.

Over decades, Dollar-Cost Averaging (DCA) has proven to be one of the most reliable wealth-building strategies in modern financial markets.