In the landscape of 2026, the global economy has moved past the volatile inflationary shocks of the early 2020s, yet the fundamental rules of wealth creation remain unchanged. For citizens of Tier-1 economies—the United States, United Kingdom, Canada, and Australia—the path to financial independence is not found in “get-rich-quick” schemes or speculative timing. It is found in the disciplined application of compound interest, tax efficiency, and global diversification.

If you’re wondering how to begin investing in 2026, the process is far simpler—and more accessible—than ever before.

This guide serves as a professional-grade manual for transforming from a saver into a serious long-term investor. This 2026 investing blueprint is designed for anyone serious about building long-term wealth.

1. Why Investing Matters More Than Ever in 2026

If you are holding the majority of your net worth in cash, you are not “playing it safe.” You are opting for a guaranteed, slow-motion loss of purchasing power. Understanding how to start investing in 2026 begins with recognizing how inflation quietly erodes wealth.

For anyone starting to invest in 2026, the goal is not speculation—it is disciplined ownership of productive assets.

The Silent Erosion: Inflation

Inflation is rarely a sudden explosion; it is a quiet thief. In Tier-1 nations, central banks generally target a 2% inflation rate. While this sounds negligible, the cumulative effect over a career is devastating.

- The 10-Year Outlook: At a 3% average inflation rate, $100 today will purchase only roughly $74 worth of goods in a decade.

- The 30-Year Outlook: Over a standard 30-year working career, that same $100 retains only about $41 of its original value.

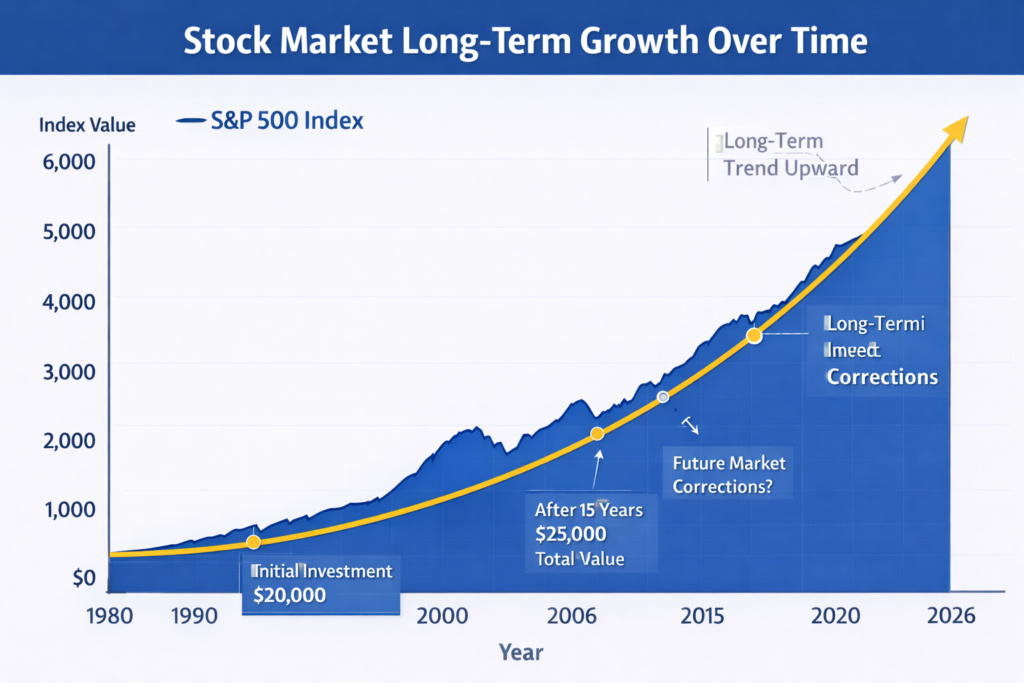

The Growth Engine: The Equity Markets

While cash loses value, productive assets—specifically stocks—have historically outpaced inflation by a wide margin. Investing is the process of putting your capital to work in the global economy. When you invest in a broad market index, you are betting on human ingenuity, technological advancement, and corporate efficiency.

Historical Annualized Returns (Long-Term):

The Core Principle: Volatility is the price you pay for returns. Every major market crash—the 2000 Dot-com bubble, the 2008 Financial Crisis, the 2020 Pandemic—was followed by a recovery that eventually surpassed previous highs.

| Index | Primary Region | Historical Annualized Return |

| S&P 500 | USA | 8% – 10% |

| FTSE 100 | United Kingdom | 4% – 7% |

| S&P/TSX Composite | Canada | 6% – 8% |

| S&P/ASX 200 | Australia | 7% – 9% |

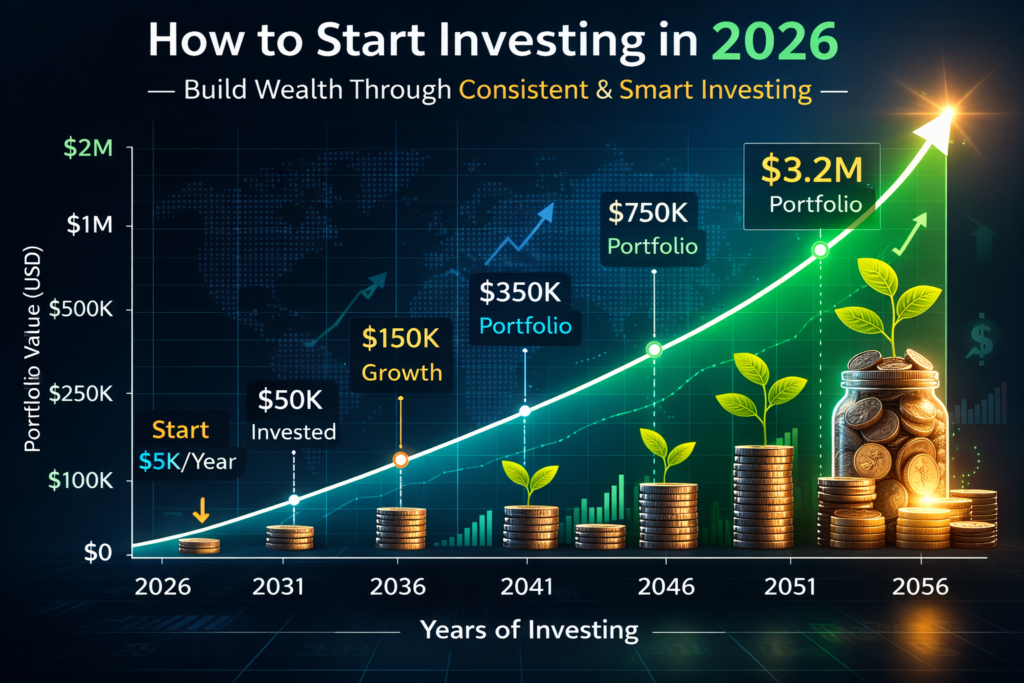

2. Step 1 in How to Start Investing in 2026: Define Your Financial Goal

Investing without a destination is merely speculation. Your strategy must be dictated by your “Time Horizon”—the duration you expect to hold the investment before needing the cash. Every successful investing strategy for 2026 begins with clarity around time horizon and risk tolerance.

A. Short-Term Goals (1–3 Years)

Examples: Saving for a wedding, a house deposit within 24 months, or an emergency fund.

- Strategy: Preservation of Capital.

- The Risk: The stock market can drop 20% in a single month. If you need that money for a down payment in 6 months, you cannot afford that volatility.

- Recommended Vehicles: * USA: High-Yield Savings Accounts (HYSA) or 4-week Treasury Bills ($T$-Bills).

- UK: Premium Bonds or Fixed-Term Savings Accounts.

- Canada: Guaranteed Investment Certificates (GICs).

- Australia: High-interest Term Deposits.

B. Medium-Term Goals (5–10 Years)

Examples: Funding a child’s secondary education or starting a business.

- Strategy: Balanced Growth.

- Typical Allocation: 60% Equities (Stocks) / 40% Fixed Income (Bonds). This provides growth potential while the bonds act as a “ballast” to reduce the depth of market dips.

C. Long-Term Goals (15–40 Years)

Examples: Retirement or building generational wealth.

- Strategy: Aggressive Compounding.

- The Math of Wealth:

- Investor A: Starts at age 25, invests $500/month at 8% return. At age 65, they have $1.6 million.

- Investor B: Starts at age 35, invests $1,000/month (double the amount) at 8% return. At age 65, they have $1.4 million.

- The Lesson: Time is more powerful than the amount invested. Starting ten years earlier is more effective than doubling your contribution later.

3. Step 2 in How to Start Investing in 2026: Understand How the Stock Market Works

To be a “Serious Investor,” you must move past the “gambling” mindset and understand the mechanics of the market. For beginner investing in 2026, ETFs provide instant diversification without requiring stock-picking expertise.

What is a Stock?

A stock is a legal claim on a portion of a company’s earnings and assets. When you buy a share of Microsoft (MSFT) or BHP Group (BHP), you are a part-owner. You benefit via:

- Capital Appreciation: The share price goes up as the company becomes more valuable.

- Dividends: A portion of the company’s profits paid out to you in cash.

What is an Index?

An index is a statistical measure of a section of the stock market.

- S&P 500: The 500 largest publicly traded companies in the US. It is the “gold standard” for measuring the US economy. Historical performance data can be reviewed through the U.S. Securities and Exchange Commission and major asset managers such as Vanguard Group.

- FTSE 100: The 100 largest companies listed on the London Stock Exchange. Highly weighted toward energy, banking, and mining.

- ASX 200: The 200 largest stocks in Australia, heavily influenced by the materials and financial sectors.

The Power of the ETF (Exchange-Traded Fund)

In the past, you had to pick individual stocks—a difficult and risky task. Today, you use ETFs. An ETF is a basket of hundreds or thousands of stocks.

- Diversification: If one company in the S&P 500 goes bankrupt, your portfolio barely feels it because you own 499 others.

- Liquidity: You can buy or sell them on the stock exchange just like a regular stock.

4. Step 3 in How to Start Investing in 2026: Choose the Right Investment Account (Tax Efficiency)

Your choice of “wrapper”—the account you hold your investments in—is often more important than the investments themselves. Governments in Tier-1 countries provide tax incentives to encourage investing. A critical part of how to start investing in 2026 is choosing the correct tax-advantaged account.

🇺🇸 United States: The “Three-Bucket” Strategy

- 401(k) / 403(b): Employer-sponsored. The “Free Money” bucket. If your employer offers a “match” (e.g., they contribute $1 for every $1 you do), this is an immediate 100% return.

- Roth IRA: You pay tax on the money now, but all future growth and withdrawals are 100% tax-free. This is the holy grail for young investors.

- Taxable Brokerage: No tax benefits, but you can withdraw the money whenever you want without penalties.

🇬🇧 United Kingdom: The ISA Advantage

- Stocks & Shares ISA: You can contribute up to £20,000 per year (as of current limits). Official guidance is available via HM Revenue & Customs. Any profit you make is entirely exempt from Capital Gains Tax (CGT) and Dividend Tax.

- SIPP (Self-Invested Personal Pension): The government gives you “Tax Relief.” If you are a basic-rate taxpayer, contributing £800 results in the government adding £200 to make it £1,000.

🇨🇦 Canada: The TFSA vs. RRSP

- TFSA (Tax-Free Savings Account): Despite the name, it’s for investing. Any growth inside is tax-free. It is highly flexible for both medium and long-term goals. Detailed rules are published by the Canada Revenue Agency.

- RRSP (Registered Retirement Savings Plan): Contributions reduce your taxable income now. You pay tax when you withdraw in retirement, presumably when you are in a lower tax bracket.

🇦🇺 Australia: The Superannuation System

- Superannuation (Super): A mandatory system where employers contribute a percentage of your salary. It is taxed at a concessional rate of 15%, far lower than most income tax brackets. Contribution rules are maintained by the Australian Taxation Office.

- SMSF (Self-Managed Super Funds): For advanced investors wanting total control over their retirement assets.

5. Step 4 in How to Start Investing in 2026: Asset Allocation and Risk Management

No guide on how to start investing in 2026 would be complete without understanding asset allocation. Asset allocation is the process of deciding how much of your money goes into different “Asset Classes.”

The Primary Asset Classes

- Equities (Stocks): High risk, high reward. The “Growth” engine.

- Fixed Income (Bonds): You are lending money to a government or corporation. They pay you interest. Lower risk, lower reward.

- Cash/Cash Equivalents: No risk of nominal loss, but high risk of losing value to inflation.

The Modern Allocation Strategy

The old rule was “100 minus your age equals your stock percentage.” In 2026, with longer life expectancies, many professionals use “120 minus your age.”

- Age 25: 95% Stocks / 5% Bonds. (You have 40 years to recover from crashes).

- Age 50: 70% Stocks / 30% Bonds. (You need to start protecting your “nest egg”).

Diversification: The “Only Free Lunch”

Never bet on just one country. A proper diversification strategy spreads risk across sectors and countries. A global asset allocation reduces concentration risk. A Global Portfolio typically includes:

- 50% Domestic Stocks (e.g., US stocks for US residents).

- 40% International Developed Markets (Europe, Japan, Australia).

- 10% Emerging Markets (India, Brazil, SE Asia).

6. Step 5 in How to Start Investing in 2026: Picking Your First Investments

The smartest approach to starting to invest in 2026 is keeping costs low and exposure broad. For a beginner, the goal is to be “Low Cost” and “Broad Market.” High fees are the “cancer” of an investment portfolio.

The “Three-Fund Portfolio” Model

This is a world-renowned strategy championed by the “Bogleheads” (followers of Vanguard founder Jack Bogle). You only need three ETFs:

- Total Stock Market Index: Covers every public company in your home country (e.g., VTI in the US, VCN in Canada).

- Total International Stock Index: Covers the rest of the world (e.g., VXUS).

- Total Bond Market Index: (e.g., BND or AGG).

Expense Ratios: Why 1% is Too Much

Every ETF charges an “Expense Ratio.”

- Cheap Fund: 0.03% ($3 per year for every $10,000 invested).

- Expensive Fund: 1.00% ($100 per year for every $10,000).Over 30 years, that 1% fee can eat up to 30% of your total ending wealth. In 2026, there is no reason to pay more than 0.20% for a core portfolio.

Understanding Real Returns, Risk, and Investor Behavior

| Concept | Simple Definition | Why It Matters in 2026 | Example | Action Step for Beginners |

|---|---|---|---|---|

| Nominal Return | The raw percentage return before inflation | Headlines often quote this number, but it overstates real wealth growth | Portfolio earns 8% in a year | Don’t evaluate performance using nominal return alone |

| Real Return | Return after adjusting for inflation | Protects your purchasing power over decades | 8% return – 3% inflation = 5% real return | Focus on long-term inflation-adjusted returns |

| Inflation-Adjusted Returns | Growth measured in today’s dollars | Critical for retirement planning and long-term investing | $1M in 2056 ≠ $1M today | Use conservative inflation estimates (2–3%) in projections |

| Sequence of Returns Risk | Risk of poor market performance early in retirement | Early losses + withdrawals can permanently damage portfolios | Market drops 25% in first retirement year | Reduce equity exposure gradually near retirement |

| Market Correction | A temporary decline of 10%+ from recent highs | Normal part of investing cycle | S&P 500 drops 12% in 6 months | Continue investing; avoid panic selling |

| Bear Market | A prolonged decline of 20%+ | Tests emotional discipline | 2008 financial crisis | Stick to your asset allocation plan |

| Behavioral Finance Biases | Psychological tendencies that affect decisions | Often cause investors to buy high and sell low | Selling during panic | Automate investments to remove emotion |

| Loss Aversion | Fear of losses outweighs joy of gains | Leads to premature selling | Selling after 15% drop | Zoom out to 20–30 year perspective |

| Passive Investing | Matching market performance via low-cost ETFs | Historically outperforms most active managers after fees | S&P 500 ETF | Use diversified index funds |

| Active Investing | Trying to outperform the market via stock selection | Higher fees + inconsistent results | Stock picking or managed funds | Only allocate small % if experienced |

One overlooked part of how to start investing in 2026 is understanding the difference between nominal returns and real returns.

A nominal return is the raw percentage gain your investment produces. For example, if your portfolio grows 8% in a year, that is your nominal return. However, if inflation during that year is 3%, your real (inflation-adjusted) return is only 5%. Over decades, inflation-adjusted returns matter far more than headline numbers.

Another critical concept is sequence of returns risk. This refers to the danger of experiencing major market declines early in retirement while withdrawing funds. Even if long-term average returns remain strong, poor early returns can significantly reduce portfolio longevity. This is why asset allocation becomes increasingly important as you age.

Behavioral finance also plays a major role in investing outcomes. Investors frequently fall victim to cognitive biases such as loss aversion (fear of losses), recency bias (believing recent trends will continue), and overconfidence. These biases often cause investors to buy during market peaks and sell during downturns.

Finally, the debate between passive vs active investing remains relevant in 2026. Over long periods, low-cost index funds often outperform most actively managed funds. According to historical data published by Vanguard, the majority of active managers underperform low-cost index funds over 15-year periods. Active managers attempt to outperform the market through stock selection and market timing. Passive investing, typically through low-cost ETFs, seeks to match market performance while minimizing fees. Over long periods, data consistently shows that low-cost passive strategies outperform the majority of actively managed funds after fees.

Understanding these principles strengthens your investing strategy for 2026 and reinforces why simplicity, discipline, and cost control are powerful advantages.

7. Step 6 in How to Start Investing in 2026: The Mechanics of Investing (Automation)

One overlooked step in how to begin investing in 2026 is automation. The greatest enemy of the investor is not the market; it is the human brain. We are hard-wired to buy when things are expensive (excitement) and sell when things are cheap (fear).

Dollar-Cost Averaging (DCA)

DCA is the practice of investing a fixed amount of money at regular intervals, regardless of the price.

- When the market is Up, your $500 buys fewer shares.

- When the market is Down, your $500 buys more shares.This mathematically lowers your average cost per share over time and removes the need to “time the market.”

Step-by-Step Automation:

- Link your bank account to your brokerage.

- Set a “Recurring Deposit“ for the day after your paycheck arrives.

- Set an “Automatic Buy” order for your chosen ETFs.

8. Step 7 in How to Start Investing in 2026: Risk Management and Market Psychology

Understanding the “Correction”

Anyone serious about beginner investing in 2026 must understand volatility. In the stock market, a 10% drop is called a “Correction.” This happens almost every single year. It is a normal part of the market breathing.

A 20% drop is a “Bear Market.” This happens roughly every 4–7 years.

The Investor’s Creed: “Time in the Market beats Timing the Market”

If you invested $10,000 in the S&P 500 from 2003 to 2023 but missed the 10 best days of the market (which often happen right after the worst days), your ending balance would be cut in half.

Successful investing is 1% action and 99% patience.

9. Step 8 in How to Start Investing in 2026: Common Beginner Pitfalls to Avoid

- Chasing the “Hot Tip”: If you heard about a “sure thing” stock on social media or from a friend, you are already too late. The “smart money” has already moved in.

- Checking Your Account Daily: This triggers emotional responses. Check your portfolio once a quarter or once a year.

- Ignoring the Emergency Fund: Never invest your last dollar. You should have 3–6 months of living expenses in a high-interest savings account before buying stocks.

- Complexity Bias: Many believe a “better” portfolio must be more complex. In reality, a simple two-ETF portfolio usually outperforms professional hedge funds over 20 years.

10. Step 9 in How to Start Investing in 2026: Your 2026 Five-Step Action Plan

- The Safety Net: Build a $2,000 “Starter Emergency Fund.”

- The Match: Contribute to your employer-sponsored retirement plan (401k/Super/Pension) to get the full match.

- The Tax-Free Bucket: Open a Roth IRA (USA), ISA (UK), or TFSA (Canada) and set up a $100/month (minimum) auto-contribution.

- The Selection: Buy a Total World Stock ETF (e.g., VT or VWRD).

- The Increase: Every time you get a pay raise, “split” it—put 50% toward your lifestyle and 50% toward increasing your monthly investment.

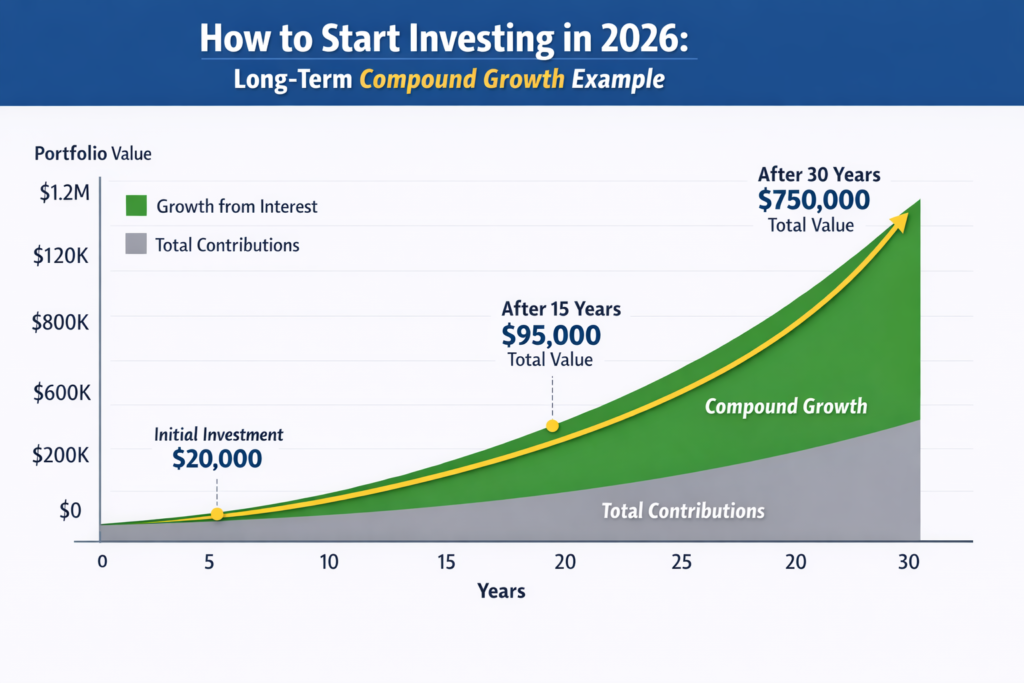

11. Case Study: The Power of Compounding

This example illustrates why how to start investing in 2026 is less about timing and more about time in the market. This demonstrates the exponential power of compound interest.

Case 1: The Early Starter (The Power of Time)

- Investor: Sarah, age 22.

- Contribution: $400/month.

- Duration: 43 years (retire at 65).

- Return: 8% (Historical Average).

- Final Result: ~$1,750,000. Total invested: $206,400.

Case 2: The Late Bloomer (The Cost of Waiting)

- Investor: Mark, age 42.

- Contribution: $1,500/month (Nearly 4x Sarah’s amount).

- Duration: 23 years (retire at 65).

- Return: 8%.

- Final Result: ~$1,250,000. Total invested: $414,000.

Conclusion: Mark invested twice as much money as Sarah, yet ended up with $500,000 less. Time is your greatest asset.

12. Final Reflection: The Wealthy Mindset

Wealth is not what you spend; it is the assets you own that produce value while you sleep. In 2026, the barriers to entry have never been lower. You can start with $10 in many countries.

The difference between those who struggle financially and those who thrive is not “luck” or “insider information.” It is the willingness to delay gratification today for freedom tomorrow. If you follow this investing strategy for 2026 consistently, wealth becomes a mathematical outcome—not luck.

Investing is a marathon, not a sprint. Start your first mile today.