Real estate has created more millionaires than almost any other asset class in modern financial history—especially in Tier-1 countries such as the United States, Canada, the United Kingdom, Australia, and Western Europe. From industrial magnates of the 19th century to modern entrepreneurs and professionals, property ownership has been one of the most consistent paths to financial independence.

For those exploring real estate investing for beginners, the opportunity today is not just about buying property — it’s about building a structured, repeatable system for wealth creation. Real estate investing for beginners works best when approached with data, discipline, and long-term thinking rather than speculation.

Real estate investing for beginners may seem complex at first, but with the right strategy, it becomes one of the most predictable wealth-building systems available.

Unlike stocks, bonds, or cryptocurrencies—which exist only as digital or paper claims—real estate is a tangible, income-producing, utility-based asset. It combines four powerful wealth-building forces:

- Cash flow – monthly income from rent.

- Appreciation – long-term increase in value.

- Leverage – control of large assets with small capital.

- Tax efficiency – legal strategies to reduce or defer taxes.

Even during periods of high interest rates, rising inflation, or economic uncertainty, property remains resilient because it satisfies a basic human need: shelter. People may stop buying luxury goods during recessions, but they rarely stop paying rent.

Yet for beginners, real estate often feels overwhelming. High down payments, complex legal terminology, fear of buying at the “top,” horror stories about bad tenants, and uncertainty about market cycles discourage many people from ever making their first move. As a result, they remain renters or passive investors while others quietly build portfolios that generate income, equity, and freedom.

This comprehensive 2026 guide is designed to strip away complexity and give you a technical, psychological, and strategic roadmap for buying your first property smartly. Whether you live in the US, UK, Canada, Australia, or Western Europe, this guide will teach you how to:

- Evaluate deals with confidence.

- Use financing intelligently.

- Manage risk conservatively.

- Build wealth sustainably.

This is not speculation. This is systematic wealth construction.

Why Real Estate Investing for Beginners Is Still Powerful in 2026

Real estate investing for beginners remains one of the most accessible and reliable ways to build long-term wealth in 2026. Unlike stocks or crypto, property allows new investors to use leverage — meaning you control a large asset with a relatively small down payment.

Accessibility is another major advantage. In many Tier-1 countries, first-time buyer programs allow entry with as little as 3–5% down. This lowers the barrier to entry compared to most business ventures.

Real estate also acts as an inflation hedge. As inflation rises, rents and property values typically increase over time, protecting purchasing power. Meanwhile, fixed-rate mortgages stay constant, effectively becoming cheaper in real terms.

Tax advantages further strengthen the appeal. Investors may deduct mortgage interest, property expenses, depreciation, and maintenance costs (depending on local regulations), increasing net returns.

For these reasons, real estate investing for beginners continues to be a powerful, proven wealth-building strategy when approached conservatively.

1. Understanding Real Estate Investing (Beginner Level)

At its core, real estate investing is the acquisition, ownership, management, rental, and/or sale of property for profit. The profit comes from two sources:

- Income – money generated while you own the property.

- Growth – increase in the property’s value over time.

This differs fundamentally from buying a home to live in, which is usually driven by emotional and lifestyle considerations rather than financial return.

1.1 The Psychological Shift: Consumer vs Investor

Most people are trained to think like consumers:

- “Can I afford the monthly payment?”

- “Do I like the kitchen?”

- “Is the neighborhood nice?”

Investors think differently:

- “Does this asset produce income?”

- “What is the return on invested capital?”

- “How resilient is demand in this area?”

- “What is my downside risk?”

This mental shift is the foundation of every successful real estate career. This mindset shift is especially important in real estate investing for beginners, where emotional decision-making often leads to poor first purchases.

1.2 Home vs Investment Property

Let’s define the difference clearly:

A Primary Residence (Home)

- You live in it.

- You pay the mortgage.

- You pay for repairs.

- You pay taxes and insurance.

- It does not produce income.

While it may appreciate over time, it usually costs you money every month. From a cash-flow perspective, it is a liability.

An Investment Property

- Tenants live in it.

- Tenants pay rent.

- Rent covers expenses and debt.

- You keep the surplus.

- You benefit from appreciation and tax advantages.

From a financial perspective, it is an asset—something that puts money in your pocket.

This distinction alone separates people who build wealth from people who merely consume.

The Two Main Ways You Make Money

Every profitable real estate deal is driven by two wealth engines:

- Cash Flow – short-term income.

- Appreciation – long-term growth.

Both are important. A deal with strong appreciation but no cash flow is speculative. A deal with strong cash flow but no appreciation is stable but may not scale wealth as quickly. The most powerful deals combine both.

1.3 Cash Flow (The Income Engine)

Cash flow is the net income you receive after all expenses and debt payments have been deducted from rental income. It is the actual money you keep each month. In real estate investing for beginners, prioritizing positive cash flow dramatically reduces financial stress and increases long-term survival rates.

1.3.1 The Cash Flow Formula

Gross Rental Income

– Operating Expenses

– Debt Service

= Net Cash Flow

Let’s break each component down.

Gross Rental Income

This is the total rent collected from all tenants before any deductions.

Example:

- Single-family home: £1,800/month rent.

- Duplex: £1,200 + £1,300 = £2,500/month rent.

This is your top-line revenue.

Operating Expenses

These are the ongoing costs required to operate and maintain the property. They include:

- Property taxes – Paid annually or monthly to local government.

- Insurance – Covers fire, liability, and other risks.

- Maintenance and repairs – Plumbing, roofing, appliances, landscaping.

- Property management fees – Typically 8%–12% of rent.

- Utilities – If landlord-paid (water, trash, electricity).

- HOA fees – If applicable.

- Vacancy allowance – Money set aside for periods when the property is unoccupied.

A conservative investor typically budgets 30%–40% of gross rent for operating expenses (excluding mortgage).

Debt Service

This is your mortgage payment, which includes:

- Principal – The portion that reduces your loan balance.

- Interest – The cost of borrowing money.

1.3.2 Real-World Cash Flow Example (UK)

You own a rental house in a suburb of Manchester.

- Rent: £2,000/month

- Mortgage: £1,200/month

- Property Taxes & Insurance: £300/month

- Maintenance Reserve (10%): £200/month

Net Cash Flow = £2,000 – (£1,200 + £300 + £200) = £300/month

This £300 is positive cash flow.

1.3.3 Why Cash Flow Is Critical

Cash flow is not just income—it is risk management. Risk control is the foundation of successful real estate investing for beginners, particularly in the first five years of portfolio building.

It:

- Creates a buffer during recessions.

- Covers unexpected repairs.

- Allows you to hold property long-term.

- Reduces dependence on your job.

- Funds future investments.

In contrast, negative cash flow means you must subsidize the property from your own income. This increases financial stress and risk. While some experienced investors accept negative cash flow in high-growth markets, beginners should avoid it because it relies on appreciation speculation rather than financial stability.

1.4 Appreciation (The Growth Engine)

Appreciation is the increase in a property’s market value over time. It is the primary driver of long-term wealth accumulation in real estate. While appreciation is powerful, real estate investing for beginners should never rely solely on future price growth to justify a purchase.

1.4.1 Market Appreciation (Passive)

Market appreciation occurs due to external forces such as:

- Population growth – More people competing for limited housing.

- Job creation – Higher incomes increase housing demand.

- Inflation – Currency loses value, assets rise in nominal terms.

- Supply constraints – Zoning laws, land scarcity, construction delays.

Example:

If you buy a home for $400,000 and the market grows at 4% per year, the value becomes approximately $592,000 after 10 years.

1.4.2 Forced Appreciation (Active)

Forced appreciation is value you create through strategic improvements.

Examples:

- Renovating a kitchen increases perceived value.

- Adding a bathroom improves rentability.

- Converting a basement into a legal rental unit increases income.

- Improving energy efficiency lowers operating costs and increases desirability.

Example:

You buy a dated home for $300,000, spend $40,000 on renovations, and the new market value becomes $400,000. You have created $60,000 in equity—not by waiting, but by acting.

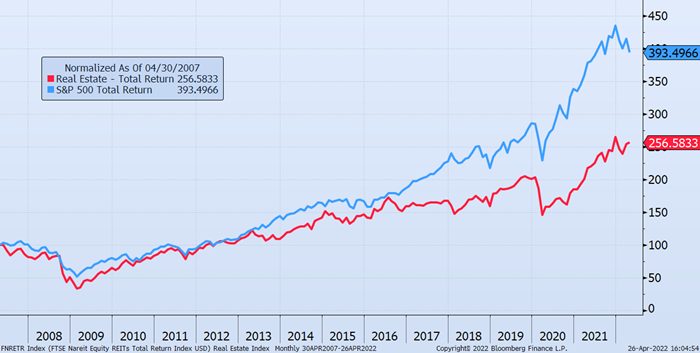

This is how investors manufacture wealth. To understand why real estate remains powerful for beginners, compare its historical return profile against other major asset classes:

2. Why Tier-1 Countries Are Ideal for Beginners

While emerging markets may offer higher nominal returns, Tier-1 countries provide something more valuable to beginners: predictability and safety.

2.1 Strong Legal Protections

In Tier-1 countries:

- Property rights are constitutionally protected.

- Titles are enforceable.

- Courts uphold contracts.

- Land registries are reliable.

- Government seizure without compensation is rare.

This legal infrastructure dramatically reduces political and ownership risk.

2.2 Access to Long-Term Financing

Tier-1 countries offer:

- 30-year fixed-rate mortgages (USA).

- Long amortization periods (Canada, Australia).

- Competitive lending markets.

This allows investors to:

- Lock in borrowing costs.

- Predict cash flow.

- Scale portfolios safely.

2.3 Stable Rental Demand

Urbanization, immigration, and housing shortages create chronic rental demand in cities such as:

- London

- Toronto

- Sydney

- New York

- Austin

- Berlin

As long as people need shelter, your asset remains economically relevant.

3. Setting Clear Investment Goals for Real Estate Investing for Beginners

A beginner without a goal is like a pilot without a destination. Successful real estate investing for beginners starts with clarity of purpose.

Your investment goal determines:

- Property type.

- Location.

- Financing strategy.

- Risk tolerance.

- Time horizon.

3.1 Income-Focused Investors

You want monthly income to supplement or replace your job.

Characteristics:

- Focus on cash flow.

- Prefer multi-unit properties.

- Target B-class neighborhoods.

- Emphasize rent-to-price ratios.

Example:

A duplex that nets $500/month in cash flow can replace a car payment, fund travel, or accelerate retirement savings.

3.2 Growth-Focused Investors

You want long-term wealth accumulation.

Characteristics:

- Focus on appreciation.

- Target A-class neighborhoods.

- Invest near job centers and infrastructure.

- Accept lower cash flow or breakeven.

Example:

A condo in central London may break even monthly but double in value over 15 years, creating substantial equity.

4. How Much Money Do You Really Need?

The myth that you need 20% down prevents many people from starting. In 2026, there are multiple low-entry strategies.

4.1 Down Payment Options

1. Low Down Payment (3.5%–5%)

Available through:

- USA: FHA loans (owner-occupied).

- UK: First-time buyer schemes.

- Canada: Insured mortgages.

- Australia: First Home Buyer programs.

These usually require you to live in the property for at least one year. For official mortgage qualification requirements and government-backed loan programs in the United States, review the U.S. Department of Housing and Urban Development (HUD) guidelines here: https://www.hud.gov

2. Standard Investment Down Payment (20%–25%)

Required for:

- Non-owner-occupied properties.

- Lower interest rates.

- Higher approval chances.

- Stronger cash flow.

4.2 Hidden Costs

Always budget an extra 3%–5% of the purchase price for:

- Stamp duty / land transfer tax.

- Legal and conveyancing fees.

- Inspection and appraisal.

- Loan origination fees.

- Title insurance (where applicable).

Failing to budget for these can derail your deal at the closing table. Stamp duty / land transfer tax (UK investors can review current Stamp Duty Land Tax rates and thresholds on the official UK government website here: https://www.gov.uk/stamp-duty-land-tax).

5. Best Real Estate Strategies for Beginners

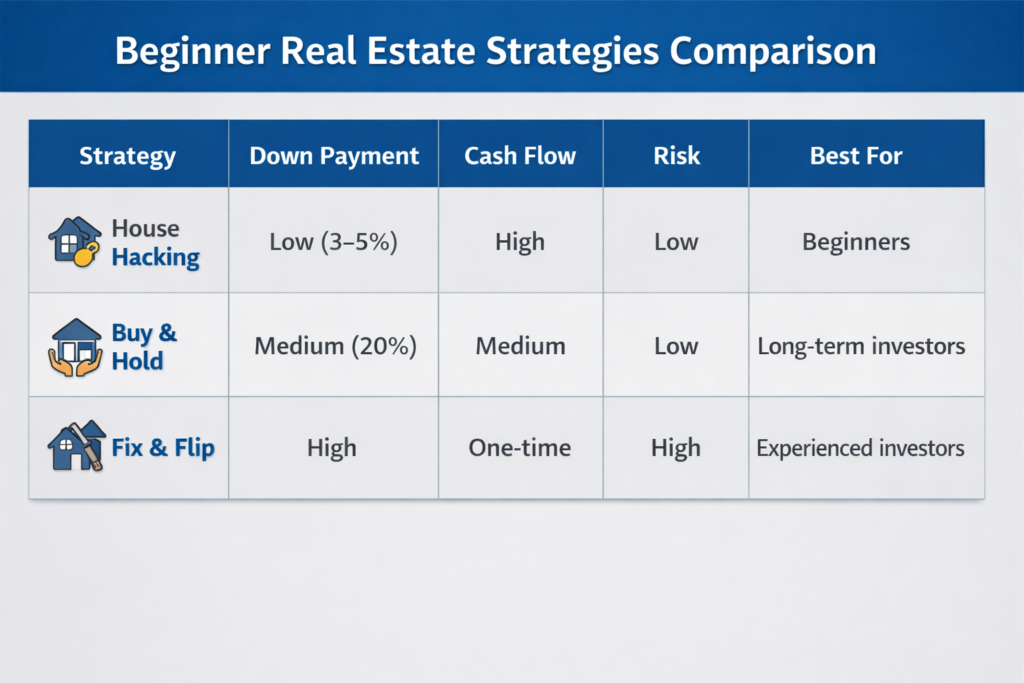

5.1 House Hacking (The Beginner’s Cheat Code)

House hacking is the most powerful beginner strategy because it eliminates your housing expense while building wealth.

How House Hacking Works

- Buy a 2–4 unit property.

- Live in one unit.

- Rent out the others.

- Use low down payment financing.

- Let tenants pay the mortgage.

Real-World Example (USA)

You buy a triplex in Chicago for $450,000 with 3.5% down.

- Unit A (you live): $0 rent.

- Unit B: $1,500/month.

- Unit C: $1,500/month.

- Total rent: $3,000/month.

Your mortgage, taxes, and insurance total $2,800/month.

Result: You live for free and pocket $200/month.

Why House Hacking Is Powerful

- Eliminates housing costs.

- Builds equity.

- Reduces risk.

- Provides landlord experience.

- Enables rapid scaling.

5.2 Buy and Hold

The classic long-term strategy.

Process:

- Buy a property.

- Rent it long-term.

- Hold for decades.

- Let tenants pay off the loan.

- Benefit from appreciation and tax advantages.

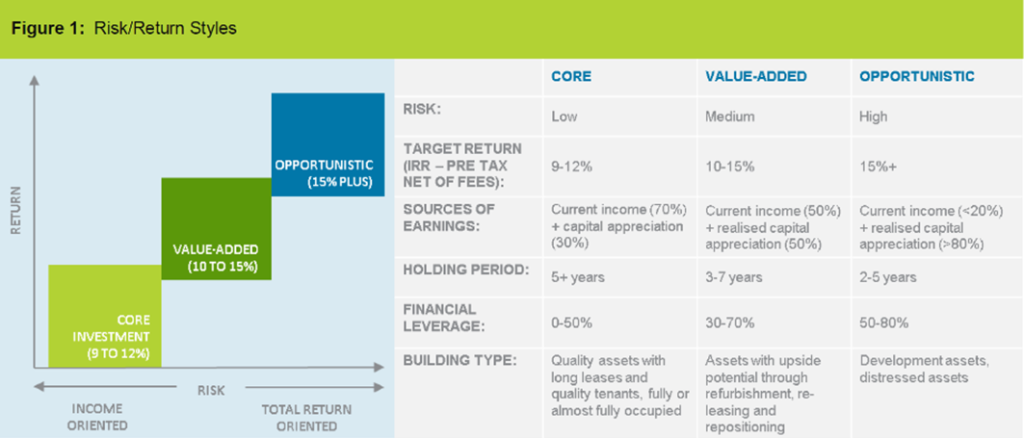

This strategy prioritizes stability, predictability, and compounding. Below is a simplified comparison of the most beginner-friendly real estate strategies:

6. Choosing the Right Location

You can renovate a house, but you cannot move it. Location determines:

- Rent levels.

- Vacancy rates.

- Appreciation.

- Tenant quality.

- Exit strategy.

6.1 Macro Market (City-Level)

Look for cities with The Three Pillars:

- Job Growth – New employers, expanding industries.

- Population Growth – Net migration inflows.

- Infrastructure Investment – Transit, highways, airports, universities.

Cities meeting all three tend to outperform over time.

6.2 Micro Market (Neighborhood-Level)

Within a city, look for:

- Proximity to universities, hospitals, and grocery stores.

- Walkability and public transit.

- School quality.

- Low crime rates.

- Strong rental demand.

Properties within a 10-minute walk of major anchors tend to remain occupied even during recessions.

7. Understanding Financing and Mortgages

Financing is the engine of your investment. Understanding loan mechanics gives you a strategic advantage.

7.1 Key Mortgage Terms

1. LTV (Loan-to-Value)

LTV measures the size of your loan relative to the property’s value.

Example:

- Purchase price: $100,000

- Loan amount: $80,000

- LTV = 80%

Lower LTV = lower risk to lender = better rates.

2. DTI (Debt-to-Income)

DTI measures how much of your income goes toward debt payments.

Formula:

Total Monthly Debt ÷ Gross Monthly Income = DTI

Most lenders require DTI below 43%. Canadian investors can review official mortgage rules, lender regulations, and borrower protections through the Financial Consumer Agency of Canada here: https://www.canada.ca/en/financial-consumer-agency.html.

3. Amortization

Amortization is the schedule by which your loan is repaid.

Early years:

- Mostly interest.

- Little principal reduction.

Later years:

- Mostly principal.

- Rapid equity growth.

7.2 Fixed vs Variable Rates

Fixed-Rate Mortgages

- Same payment every month.

- Protection against rate hikes.

- Easier budgeting.

Variable-Rate Mortgages

- Payments fluctuate.

- Lower initial rates.

- Higher risk.

For beginners, fixed-rate mortgages are strongly recommended.

8. How to Analyze a Deal Like a Pro

Every deal must be evaluated with numbers—not emotions.

8.1 The 1% Rule (Quick Screening Tool)

A property should ideally rent for 1% of its purchase price per month.

Example:

- $250,000 property → $2,500/month rent.

In high-cost cities, 0.7%–0.8% may be acceptable if appreciation potential is strong.

8.2 Capitalization Rate (Cap Rate)

Cap Rate measures the return on a property if purchased with cash.

Formula:

Net Operating Income (NOI) ÷ Purchase Price = Cap Rate

In Tier-1 markets:

- 4%–6% = Solid.

- 6%–8% = Strong.

- Below 4% = Premium appreciation markets.

8.3 Cash-on-Cash Return

Cash-on-cash return measures the return on your actual cash invested.

Formula:

Annual Cash Flow ÷ Total Cash Invested = Cash-on-Cash Return

Example:

- Annual cash flow: $6,000

- Total cash invested: $60,000

- Return = 10%

9. The Power of Real Estate Leverage

Leverage is what makes real estate uniquely powerful.

You control a large asset using a relatively small amount of your own money.

Real-World Leverage Example

- Purchase price: $500,000

- Down payment: $100,000

- Loan: $400,000

If the property increases in value by 5%, that’s $25,000.

Your return:

$25,000 ÷ $100,000 = 25%

This compounding effect is how investors scale wealth faster than traditional savers.

10. Managing Risk Smartly

Risk cannot be eliminated, but it can be managed.

10.1 Fixed-Rate Debt

Fixed-rate loans protect you from interest rate volatility.

10.2 Cash Reserves

Maintain 3–6 months of expenses in a dedicated reserve account to cover:

- Vacancies.

- Repairs.

- Economic downturns.

10.3 Tenant Screening

Bad tenants cost far more than vacancies.

Always:

- Verify income.

- Check credit history.

- Call previous landlords.

- Confirm employment.

- Conduct background checks (where legal).

11. Legal and Tax Basics

Real estate is one of the most tax-advantaged asset classes in Tier-1 countries.

11.1 Depreciation

Depreciation allows you to deduct the “wear and tear” of the building from your taxable income—even if the property is increasing in value.

This often results in paper losses that reduce your tax bill while you remain cash-flow positive.

11.2 Country-Specific Advantages

- USA: 1031 Exchanges allow you to defer capital gains tax when upgrading properties.

- Australia: Negative gearing allows rental losses to offset personal income.

- UK: UK investors should consult official HMRC guidance for the latest rental tax rules and relief eligibility.

- Canada: Capital cost allowance and tax-deferred growth inside registered accounts.

12. Building Your Real Estate Team

You are the CEO of your portfolio. Surround yourself with professionals:

- Real Estate Agent – Finds deals, negotiates price.

- Mortgage Broker / Lender – Secures financing.

- Inspector – Identifies structural issues.

- Property Manager – Handles tenants and maintenance.

- Real Estate Attorney / Solicitor – Reviews contracts and protects your interests.

This team minimizes risk and maximizes efficiency.

13. Step-by-Step: Buying Your First Property

The first deal in real estate investing for beginners should be treated as a training ground rather than a speculative bet. Here is your exact beginner roadmap:

- Fix Your Credit

Aim for a credit score above 740 to secure the best interest rates. - Get Pre-Approved

Know your budget before shopping. - Define Your Buy Box

Example: “3-bedroom house under $500k within 20 minutes of downtown.” - Analyze 100 Deals

- Evaluate 100 properties.

- Make offers on 5.

- Buy 1.

- Conduct Due Diligence

- Inspection.

- Appraisal.

- Title search.

- Close and Rent

- Hire a manager if desired.

- List the property.

- Screen tenants carefully.

14. Long-Term Wealth Strategy: The Snowball Effect

Your first property is the hardest.

After 5–7 years:

- The mortgage balance decreases.

- The property value increases.

- Your equity grows.

You can then perform a cash-out refinance, extracting equity to fund the down payment for your second property—without selling the first.

Repeat this process, and one property becomes two, two become four, and four become eight. This is how ordinary professionals build extraordinary portfolios over time.

Conclusion: Your First Property Is a Foundation, Not a Gamble

Real estate investing for beginners in 2026 requires less speculation and more precision than ever before. But when done correctly—using data, discipline, and conservative assumptions—it remains one of the safest and most powerful wealth-building tools available. For real estate investing for beginners, patience and discipline matter more than timing the market. Ultimately, real estate investing for beginners is not about timing the market — it is about time in the market, supported by smart leverage and conservative decision-making.

By focusing on:

- Tier-1 markets.

- Positive cash flow.

- Responsible leverage.

- Long-term ownership.

- Risk management.

You are not gambling—you are constructing a financial future.

The smartest investors don’t wait to buy real estate; they buy real estate and wait.