1. Introduction: Why Every Adult Must Understand These Three Assets

In today’s financial world, saving money is no longer enough. While saving protects you from emergencies, it does not build wealth. In most Tier-1 countries, inflation steadily reduces the purchasing power of cash. This means that even if your bank balance grows, what that money can buy may shrink over time.

What is Inflation?

Inflation is the general increase in prices over time. If inflation is 3% annually, something that costs $100 today will cost about $103 next year. Over 10–20 years, this effect compounds dramatically. A dollar saved today may only buy half as much in the future. Investing is not just about money — it’s about security, freedom, and independence. It’s about creating a future where you’re not dependent on a paycheck. According to official U.S. inflation data from the Bureau of Labor Statistics. The U.S. Securities and Exchange Commission provides a helpful beginner investing guide.

Why Investing Matters

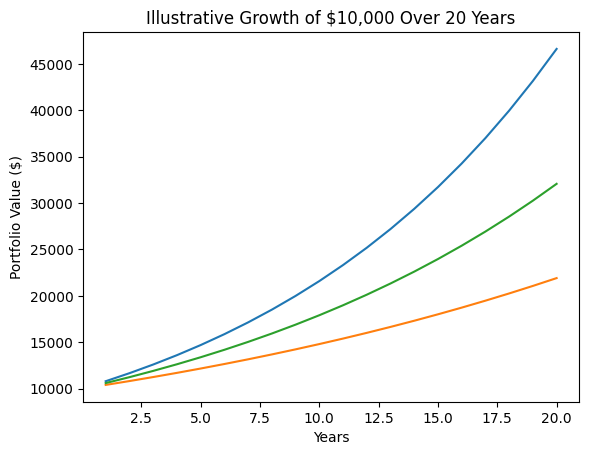

📈 Here’s how $10,000 could grow over 20 years across different asset classes (illustrative example):

Investing allows your money to grow faster than inflation, helping you:

- Build a secure retirement

- Create passive income streams

- Afford major goals like homes, education, and travel

- Achieve financial independence, meaning you no longer rely solely on a paycheck

Most people feel intimidated by investing because it seems complex or risky. In reality, successful investing is not about trading daily or predicting markets. It’s about understanding three core building blocks:

- Stocks – Ownership in businesses

- Bonds – Loans you give in exchange for interest

- Mutual Funds – Bundles of stocks and/or bonds managed professionally

Once you understand these, you understand the foundation of modern investing.

2. What Are Stocks?

How Stocks Work

A stock (also called a share or equity) represents ownership in a company. When a company needs capital to grow, it can sell shares to the public through a stock exchange. By buying shares, you become a partial owner of that business. Historically, the S&P 500 has averaged around 10% annual returns over long periods.

Example:

If a company has 1 million shares and you own 1,000 shares, you own 0.1% of the company.

Ownership gives you:

- A claim on a portion of the company’s profits

- The right to vote on major company decisions (in many cases)

- The potential to benefit if the company grows in value

Companies use stock money to:

- Expand operations

- Develop new products

- Enter new markets

- Pay off debt

Types of Stocks

Stocks are not all the same. They differ based on company size, growth stage, income generation, and valuation.

1. Growth Stocks

Definition:

Growth stocks belong to companies expected to grow faster than the overall market.

These companies usually reinvest their profits into:

- Research and development

- Marketing

- Infrastructure

- Innovation

Because they reinvest instead of paying dividends, investors profit mainly through price appreciation.

Examples:

- Technology companies

- E-commerce platforms

- Biotech startups

Real-World Example:

Amazon reinvested profits for years instead of paying dividends, focusing on growth. Early investors benefited massively from stock price appreciation.

Pros:

- High potential returns

- Strong long-term growth opportunities

Cons:

- High volatility (prices fluctuate sharply)

- Higher risk if growth expectations are not met

2. Dividend Stocks

Definition:

Dividend stocks are issued by companies that distribute a portion of profits to shareholders regularly, usually quarterly.

Examples:

- Utility companies

- Consumer staples (food, household goods)

- Large, established corporations (blue-chip stocks)

Real-World Example:

If a company pays $2 per share annually and you own 100 shares, you receive $200 each year as income.

Pros:

- Regular income

- Lower volatility than growth stocks

- Often stable businesses

Cons:

- Slower growth compared to growth stocks

- Dividends can be reduced or stopped in tough times

3. Value Stocks

Definition:

Value stocks appear undervalued compared to their fundamentals (earnings, assets, revenue). Investors believe the market has mispriced them.

Examples:

- Established companies temporarily facing challenges

- Businesses in out-of-favor industries

Real-World Example:

If a strong company’s stock drops due to short-term bad news but its core business remains strong, value investors may buy, expecting recovery.

Pros:

- Potential for price recovery

- Often pay dividends

Cons:

- The stock may remain undervalued for long periods

- Some companies are cheap for valid reasons

How You Make Money from Stocks

There are two main ways to earn from stocks:

1. Capital Appreciation

Definition:

Capital appreciation is the increase in the stock’s price over time.

Example:

- Buy stock at $50

- Sell later at $80

- Profit = $30 per share (before taxes and fees)

This profit is called a capital gain. If you bought shares at $50 and they grew to $120 over 10 years, your return would be 140% — before dividends.

2. Dividends

Definition:

Dividends are payments made by companies to shareholders from profits.

Example:

- Company pays $2 per share annually

- You own 200 shares

- Annual income = $400

Dividends provide passive income, which can be reinvested to buy more shares, compounding growth over time.

Risks of Stock Investing

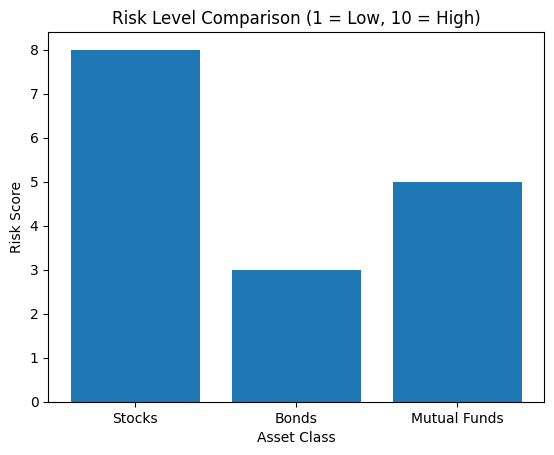

📊 Risk levels vary significantly between asset classes. Here’s a simplified comparison:

Stocks offer high return potential but come with risk.

1. Market Risk

Stock prices fall during:

- Economic recessions

- Financial crises

- Global events (wars, pandemics)

Even strong companies can see their stock prices drop temporarily.

2. Company Risk

A specific company may:

- Lose customers

- Face lawsuits

- Fail due to competition or poor management

In extreme cases, the company may go bankrupt, and shareholders may lose most or all of their investment.

3. Volatility

Stock prices fluctuate daily, sometimes sharply. Emotional reactions to price swings can lead to poor decisions, such as panic selling.

Key Insight:

Over long periods, diversified stock portfolios have historically delivered the highest returns among major asset classes — but only for investors who remain patient and disciplined.

3. What Are Bonds?

How Bonds Work

A bond is a loan you give to a government, corporation, or organization. In return, the borrower promises to:

- Pay you interest (called coupon payments) at regular intervals

- Repay the principal (original amount) at a specific maturity date

When you buy a bond, you are not an owner — you are a lender.

Key Bond Terms Explained

- Principal (Face Value): The amount you lend, usually $1,000 per bond.

- Coupon Rate: The annual interest rate paid on the bond.

- Maturity Date: The date when the principal is repaid.

- Issuer: The entity borrowing the money.

Example:

You buy a $1,000 bond with:

- Coupon rate: 5%

- Term: 10 years

Each year, you receive:

$1,000 × 5% = $50 in interest.

After 10 years, you receive:

Your original $1,000 back.

Types of Bonds

1. Government Bonds

Definition:

Issued by national governments.

Examples:

- U.S. Treasury Bonds

- UK Gilts

- Canadian Government Bonds

- Australian Commonwealth Bonds

Pros:

- Very low default risk

- Backed by government taxing power

Cons:

- Lower interest rates

- Lower long-term returns compared to stocks

2. Corporate Bonds

Definition:

Issued by companies to finance operations or expansion.

Pros:

- Higher interest rates than government bonds

Cons:

- Higher default risk

- Credit quality varies by company

3. Municipal Bonds (U.S.)

Definition:

Issued by states, cities, or local governments.

Pros:

- Often tax-free interest income at federal and sometimes state level

Cons:

- Lower yields

- Credit risk varies by municipality

4. High-Yield (Junk) Bonds

Definition:

Issued by companies with lower credit ratings.

Pros:

- Very high interest rates

Cons:

- High default risk

- More volatile

How You Make Money from Bonds

1. Interest Payments (Coupon Income)

Bonds provide predictable income, making them attractive for retirees and conservative investors.

2. Price Appreciation

Bond prices change based on interest rates:

- When interest rates fall, existing bonds with higher coupon rates become more valuable.

- When interest rates rise, existing bonds lose value.

Investors can profit by selling bonds at a higher price than they paid.

Risks of Bond Investing

1. Interest Rate Risk

When interest rates rise, bond prices fall. Long-term bonds are more sensitive to rate changes than short-term bonds.

2. Credit Risk

The issuer may fail to make interest payments or repay principal. This is called default risk.

3. Inflation Risk

Inflation reduces the purchasing power of fixed interest payments. A bond paying 3% when inflation is 5% results in a negative real return.

Despite these risks, bonds provide stability, income, and diversification, making them essential for balanced portfolios.

4. What Are Mutual Funds?

How Mutual Funds Work

A mutual fund pools money from thousands (or millions) of investors and invests it in a diversified portfolio of assets such as:

- Stocks

- Bonds

- Or a combination of both

Instead of selecting individual securities yourself, a professional fund manager makes investment decisions on your behalf.

When you buy shares of a mutual fund, you own a portion of the entire portfolio.

Example:

You invest $1,000 in a mutual fund that owns:

- 500 different stocks

- 100 bonds

Your investment is automatically diversified across all those assets — even though you only bought one fund.

Types of Mutual Funds

1. Equity (Stock) Funds

These invest primarily in stocks.

Subtypes include:

- Growth funds – Focus on fast-growing companies

- Value funds – Focus on undervalued stocks

- Index funds – Track a market index (e.g., S&P 500)

- Sector funds – Focus on specific industries (technology, healthcare, energy)

2. Bond Funds

These invest primarily in bonds.

Subtypes include:

- Government bond funds

- Corporate bond funds

- High-yield bond funds

- Short-term and long-term bond funds

3. Balanced Funds

These invest in both stocks and bonds, aiming to provide:

- Moderate growth

- Reduced volatility

- Income stability

4. Index Funds

Definition:

Index funds replicate the performance of a specific market index rather than trying to beat it.

Examples:

- S&P 500 Index Fund

- FTSE 100 Index Fund

- MSCI World Index Fund

Pros:

- Very low fees

- Broad diversification

- Historically strong long-term performance

Cons:

- Cannot outperform the market (but rarely underperform it)

How You Make Money from Mutual Funds

1. Net Asset Value (NAV) Growth

NAV is the value of one share of the mutual fund. As the fund’s investments increase in value, the NAV rises.

Example:

- Buy fund at NAV = $20

- Later NAV = $30

- Profit = $10 per share

2. Income Distributions

The fund distributes dividends and interest earned from its investments to shareholders.

3. Capital Gains Distributions

When the fund sells securities at a profit, it may distribute capital gains to investors.

Risks of Mutual Fund Investing

1. Market Risk

If the market declines, the fund’s value declines as well. If you’re worried about volatility, read our guide on How to Invest During a Market Crash (2026 Guide).

2. Management Risk

Active fund managers may make poor investment decisions, leading to underperformance.

3. Fee Risk

Mutual funds charge expense ratios — annual fees deducted from your investment. High fees significantly reduce long-term returns.

Despite these risks, mutual funds are one of the most beginner-friendly investment vehicles, offering instant diversification and professional management.

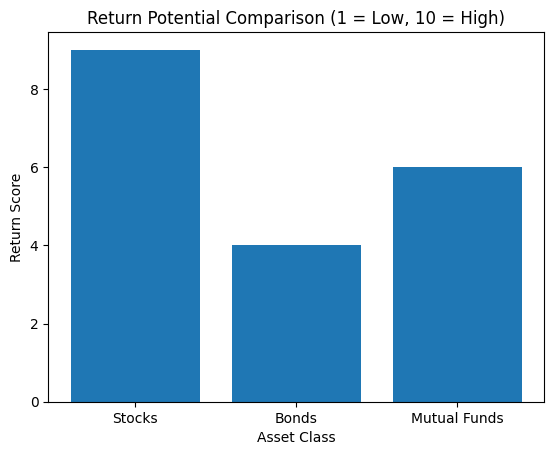

5. Stocks vs Bonds vs Mutual Funds: A Complete Comparison

| Feature | Stocks | Bonds | Mutual Funds |

|---|---|---|---|

| Ownership | Direct ownership | Lender (no ownership) | Indirect ownership |

| Risk Level | High | Low–Moderate | Varies by fund |

| Return Potential | High | Low–Moderate | Moderate–High |

| Income | Dividends (some) | Interest payments | Dividends + interest |

| Volatility | High | Low | Moderate |

| Diversification | Low (unless many) | Moderate | High |

| Best For | Long-term growth | Stability & income | Beginner-friendly investing |

🧮 Quick Compound Growth Example

Formula:

Future Value = P × (1 + r)^t

Where:

- P = Initial investment

- r = Annual return

- t = Years invested

Example:

$10,000 invested at 8% for 25 years:

= 10,000 × (1.08)^25

= $68,484

That’s the power of compounding.

🧮 Interactive Compound Interest Calculator

Try different monthly amounts and see how long-term investing builds real wealth.

📊 Case Study: Sarah’s 20-Year Investing Plan

Sarah is 30 years old and lives in the United States.

She invests:

- $500 per month

- 80% index fund (stocks)

- 20% bond fund

- Average return: 8%

After 20 years:

Using compound growth:

$500/month × 12 × 20 = $120,000 invested

Portfolio value ≈ $295,000

Nearly $175,000 came from growth — not savings.

This demonstrates why long-term investing beats saving alone.

6. How to Build a Beginner Portfolio

You can also explore real estate diversification in Real Estate Investing for Beginners. Your portfolio is the collection of all your investments. A good portfolio balances risk and return based on:

- Age

- Income

- Risk tolerance

- Time horizon

- Financial goals

General Rule of Thumb

Younger investors have more time to recover from market downturns, so they can hold more stocks. Older investors need stability and income, so they hold more bonds.

Sample Beginner Portfolios

Conservative Portfolio (Low Risk)

- 30% Stocks

- 60% Bonds

- 10% Cash

Best for:

- Retirees

- Near-term financial goals

- Risk-averse investors

Moderate Portfolio (Balanced)

- 60% Stocks

- 35% Bonds

- 5% Cash

Best for:

- Most working adults

- Medium-to-long-term goals

🥧 Here’s what a typical balanced portfolio allocation looks like:

Aggressive Portfolio (Growth-Oriented)

- 80–90% Stocks

- 10–20% Bonds

Best for:

- Young investors

- Long-term wealth builders

- High risk tolerance

Best Beginner Strategy

Most beginners in Tier-1 countries benefit from:

- Low-cost index mutual funds

- Automatic monthly investing

- Long-term holding (10+ years)

This strategy:

- Reduces emotional decision-making

- Minimizes fees

- Maximizes compound growth

7. Tax Considerations in Tier-1 Countries

Taxes significantly affect your investment returns. Understanding tax rules helps you keep more of your profits.

United States

- Capital gains tax: Paid when you sell investments at a profit

- Short-term (held < 1 year): taxed as ordinary income

- Long-term (held ≥ 1 year): taxed at lower rates

- Dividends: Qualified dividends taxed at lower rates

- Tax-advantaged accounts: 401(k), Traditional IRA, Roth IRA

United Kingdom

- Capital Gains Tax (CGT): On profits above annual allowance

- Dividend tax: Above annual dividend allowance

- Tax-efficient accounts: ISA (Individual Savings Account), SIPP (Self-Invested Personal Pension)

Canada

- Capital gains tax: Only 50% of gains are taxable

- Dividend tax credit: Reduces tax on eligible dividends

- Tax-advantaged accounts: TFSA, RRSP

Australia

- Capital gains tax: 50% discount for assets held over 12 months

- Franking credits: Refund or offset corporate tax paid on dividends

- Retirement accounts: Superannuation

Europe

Tax rules vary by country:

- Germany, France, Netherlands, Spain, and others each have unique tax systems

- Many offer tax-advantaged investment or retirement accounts

Key Tax Strategy:

Always invest through tax-advantaged accounts when available to maximize long-term growth.

8. Common Beginner Mistakes (and How to Avoid Them)

Many investors fall for common myths — see Top Investing Myths That Are Keeping You Poor.

1. Trying to Time the Market

Mistake: Waiting for the perfect moment to invest.

Reality: No one can consistently predict market movements.

Solution: Invest regularly regardless of market conditions (dollar-cost averaging).

2. Chasing Hot Stocks

Mistake: Buying stocks based on social media hype or headlines.

Reality: Most hype-driven stocks crash after initial excitement fades.

Solution: Stick to diversified funds and long-term strategies.

3. Ignoring Diversification

Mistake: Putting all money into one stock or one sector.

Reality: One bad event can destroy your portfolio.

Solution: Diversify across asset classes, industries, and regions.

4. Panic Selling During Crashes

Mistake: Selling when markets fall due to fear.

Reality: Market crashes are temporary; long-term trends are upward.

Solution: Stay invested, rebalance if needed, and continue investing.

5. Paying High Fees

Mistake: Investing in funds with high expense ratios.

Reality: Fees compound against you over decades, costing thousands or even millions.

Solution: Choose low-cost index funds whenever possible.

9. Step-by-Step: How to Start Investing Today

Step 1: Set Clear Financial Goals

Ask yourself:

- Is this money for retirement?

- Buying a home?

- Children’s education?

- Building passive income?

Your goals determine your time horizon and risk tolerance.

Step 2: Build an Emergency Fund

Before investing, save:

- 3–6 months of living expenses in cash

- Keep it in a high-interest savings account

This protects you from selling investments during emergencies.

Step 3: Open an Investment Account

Choose the right account:

- Brokerage account for general investing

- Retirement accounts (401k, IRA, ISA, TFSA, RRSP, Superannuation) for tax advantages

Step 4: Choose Your Investments

Begin with:

- Broad market index funds (e.g., S&P 500, Total Market Funds)

- Bond funds for stability

- Balanced funds for simplicity

Avoid individual stock picking as a beginner.

Step 5: Automate Your Investing

Set up:

- Automatic monthly contributions

- Automatic fund purchases

Automation removes emotion and builds discipline. This strategy is similar to Dollar-Cost Averaging, which helps reduce timing risk.

Step 6: Review Annually — Not Daily

Check your portfolio:

- Once or twice a year

- Rebalance if allocations drift

- Ignore daily market noise

10. Conclusion: Building Wealth the Smart Way

When you build a diversified portfolio and follow a long-term investing plan, you create financial independence — the ability to choose how you live and work. Stocks, bonds, and mutual funds are not just financial instruments — they are wealth-building engines.

When used correctly, they help you:

- Outpace inflation

- Build retirement security

- Generate passive income

- Achieve long-term financial freedom

You do not need to be rich to invest. You do not need insider knowledge. You do not need to predict the market.

You only need:

- A clear plan

- Consistent investing

- Patience

- Discipline

Start small. Stay consistent. Let time and compound growth do the heavy lifting.

Your future self will thank you.

Frequently Asked Questions

If you’d like, I can also:

✅ Add SEO keywords and meta description

✅ Convert this into WordPress/blog-ready format

✅ Rewrite for a specific country (US, UK, Canada, Australia, Europe)

✅ Add FAQs, calculators, or case studies