Introduction: The Invisible Enemy of Your Financial Future

Top Investing Myths That Are Keeping You Poor continue to silently sabotage millions of people across the United States, United Kingdom, Canada, Australia, and Western Europe. Even in economies filled with opportunity.

Most people assume financial struggle is caused by low income or bad luck. In reality, the biggest barrier to wealth is belief.

While income and opportunity matter, they are not the primary reason most people fail to build wealth.

Belief determines:

- Whether you invest or avoid investing.

- Whether you take responsibility or blame the system.

- Whether you start early or procrastinate.

- Whether you stay disciplined or act emotionally.

A belief is not just a thought—it is a mental rule that silently governs your decisions.

For example:

- “Investing is risky” → You avoid investing → Your money never grows → You stay financially stagnant.

- “I’m bad with money” → You don’t learn → You don’t improve → The belief reinforces itself.

In Tier-1 countries (USA, UK, Canada, Australia, Western Europe), this is especially tragic. These economies provide:

- Access to global stock markets

- Tax-advantaged retirement accounts

- Online brokerage platforms

- Low-cost index funds and ETFs

- Financial education resources

Yet millions of people still:

- Live paycheck to paycheck

- Keep money in low-interest savings accounts

- Avoid investing entirely

- Start investing decades too late

- Panic during market downturns

The issue is not access.

The issue is belief.

This guide will dismantle the most dangerous investing myths—explaining why they exist, how they damage your future, and what to replace them with so you can finally build lasting wealth.

The Top Investing Myths That Are Keeping You Poor in 2026. The Top Investing Myths That Are Keeping You Poor are not obvious.

They are disguised as logic, caution, and common sense.

But over time, they create massive financial damage.

Myth #1: “Investing Is Only for Rich People”

Definition of the Myth

This myth claims that investing is an activity reserved for people who are already wealthy—those with large incomes, inherited wealth, or elite financial connections.

Why This Myth Exists

Historically, investing was limited to the wealthy. For much of the 20th century:

- Stock trading required large minimum investments.

- Brokerage accounts had high fees.

- Investment opportunities were restricted to institutions.

- Financial information was not easily accessible.

Media reinforced this by portraying investors as:

- Wall Street bankers

- Hedge fund managers

- Tech billionaires

- Real estate moguls

This created a mental image:

Investor = Rich person in a suit, not someone like me.

Why This Myth Is Financially Deadly

If you believe investing is “not for people like me,” you delay starting—or never start at all.

That delay costs you time, and time is the most powerful variable in wealth creation due to compound interest.

What Is Compound Interest?

If you’re new to compounding, read our full breakdown on how compound interest works to see real examples and growth charts.

Compound interest is the process by which your investment earnings themselves earn returns.

Formula (simplified):

Future Value = Principal × (1 + rate)ⁿ

Where:

- Principal = initial investment

- Rate = annual return

- n = number of years

But the real power comes when you add regular contributions.

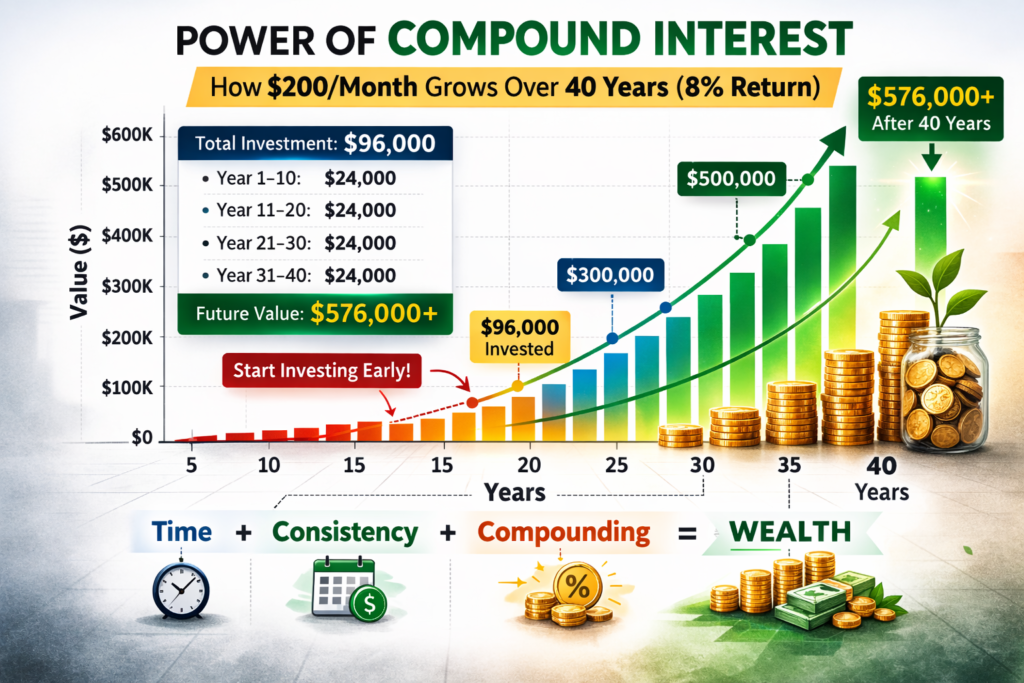

Example

Investor A:

- Starts at age 25

- Invests $200/month

- Earns an average of 8% annually

- Invests for 40 years

Investor B:

- Starts at age 40

- Invests $400/month (double the amount)

- Earns the same 8%

- Invests for 25 years

Despite investing twice as much per month, Investor B ends with less money than Investor A.

Why?

Because time multiplies money more powerfully than higher contributions alone.

The Truth

Investing is not for rich people.

Investing is how people become rich.

Today, you can:

- Open a brokerage account with $0 minimum

- Buy fractional shares (e.g., $5 worth of Apple stock)

- Invest automatically with as little as $1

- Use tax-advantaged retirement accounts like:

- 401(k) (USA)

- IRA / Roth IRA (USA)

- ISA (UK)

- TFSA / RRSP (Canada)

- Superannuation (Australia)

Wealth is not built by status, intelligence, or luck.

Wealth is built by consistent behavior over time.

Myth #2: “You Need a Lot of Money to Start Investing”

Definition of the Myth

This myth claims that you must accumulate a large amount of savings before investing—often thousands or tens of thousands of dollars.

Why This Myth Exists

This belief comes from:

- Old brokerage minimums

- Images of investors managing large portfolios

- The misconception that small investments “don’t matter”

- Confusion between saving and investing

Why This Myth Keeps You Poor

Waiting until you “have enough money” delays your investing journey. And every year of delay costs you exponential growth.

The Mathematics of Delay

Let’s compare two investors:

Investor C:

- Starts investing at 22

- Invests $100/month

- Stops at 32

- Never invests again

- Total invested: $12,000

Investor D:

- Starts at 32

- Invests $100/month

- Continues until 65

- Total invested: $39,600

Despite investing over three times as much, Investor D often ends with less money than Investor C.

Why?

Because Investor C’s money had more time to compound.

The Truth

You can start investing with:

- $10

- $50

- $100

What matters is not the amount—it’s the habit.

Think of investing like physical fitness:

- One workout doesn’t make you fit.

- One healthy meal doesn’t transform your body.

- But consistent behavior over time creates massive results.

Small investments today build:

- Financial confidence

- Habit formation

- Long-term momentum

And those habits compound into wealth.

Myth #3: “Investing Is Too Risky—It’s Basically Gambling”

Definition of the Myth

This myth equates investing with gambling—suggesting that both involve random outcomes, unpredictable losses, and luck-based results. This is one of the most dangerous patterns behind the Top Investing Myths That Are Keeping You Poor because it encourages inaction.

Why This Myth Exists

People associate investing with:

- Market crashes

- Financial crises

- Stock market volatility

- Media headlines about losses

Events like:

- The 2000 dot-com crash

- The 2008 global financial crisis

- The COVID-19 market crash

- Crypto collapses

create emotional memories that overshadow long-term growth.

Understanding Risk vs. Volatility

These two concepts are often confused:

Volatility

- Short-term price fluctuations.

- Example: A stock drops 10% this month and rises 15% next month.

Risk

- The probability of permanent loss of capital.

- Example: A business goes bankrupt and never recovers.

Long-term, diversified investing has volatility but relatively low risk of permanent loss—especially across broad markets.

Why This Myth Is Misleading

Investing in diversified, long-term assets (such as total market index funds) is not gambling—it is ownership in productive businesses.

You are not betting on numbers.

You are investing in:

- Companies

- Innovation

- Economic growth

- Human productivity

The Truth

Not investing is actually riskier.

Why?

Because inflation erodes the value of money.

Example: Inflation Erosion

If:

- Inflation averages 3% per year

- Your savings account earns 1%

According to official U.S. inflation data from the Bureau of Labor Statistics (BLS CPI data), inflation has averaged around 2–3% over long periods, steadily reducing purchasing power over time.

Your real return = -2% per year.

Over 30 years, your money loses nearly 45% of its purchasing power.

That means:

- $100,000 today will only buy what ~$55,000 buys in the future.

True risk = doing nothing.

Myth #4: “I’ll Start Investing When the Market Is Safer”

Definition of the Myth

This myth suggests that investing should wait until markets are stable, predictable, or “safe.”

Why This Myth Exists

Humans crave certainty.

Our brains evolved to:

- Avoid danger

- Seek predictability

- Fear loss more than we value gain

This leads to:

- Waiting for the “perfect time”

- Avoiding uncertainty

- Overanalyzing entry points

Why This Myth Is Dangerous

There is no such thing as a perfect time to invest.

Markets are:

- Always uncertain

- Always influenced by politics, economics, and human behavior

- Always fluctuating

People who wait for certainty often:

- Buy after prices rise

- Sell after prices fall

- Miss long-term growth

This is called emotional investing, and it consistently produces poor results.

The Truth: Dollar-Cost Averaging

Instead of trying to time the market, use dollar-cost averaging (DCA).

What Is Dollar-Cost Averaging?

It means:

- Investing a fixed amount of money at regular intervals (monthly, biweekly, etc.)

- Regardless of market conditions

For a step-by-step tutorial, see our beginner’s guide to dollar-cost averaging.

How It Works

When prices are high:

- Your fixed amount buys fewer shares.

When prices are low:

- Your fixed amount buys more shares.

Over time, this lowers your average cost per share and removes emotional decision-making.

Real-World Example

You invest $500 every month into an index fund:

- In a bull market, your account grows.

- In a bear market, your contributions buy more shares.

- Over decades, this creates massive compounding.

The Truth

The best time to invest was 20 years ago.

The second-best time is today.

Myth #5: “Investing Is Only for Financial Geniuses”

Definition of the Myth

This myth claims that successful investing requires:

- Advanced mathematics

- Deep economic knowledge

- Constant market analysis

- Exceptional intelligence

Why This Myth Exists

Finance is often presented using:

- Complex terminology

- Technical charts

- Academic language

- Financial jargon

This creates the illusion that investing is only for:

- Economists

- Analysts

- Fund managers

- Mathematicians

Why This Myth Is False

Research consistently shows that:

- Most professional fund managers fail to beat the market over long periods.

- The majority of investors underperform due to behavioral mistakes—not lack of intelligence.

The Real Drivers of Investment Success

Investment success depends on:

- Consistency – Investing regularly.

- Patience – Staying invested long-term.

- Discipline – Avoiding emotional decisions.

- Low costs – Minimizing fees and taxes.

- Diversification – Spreading risk.

None of these require genius-level intelligence.

The Truth

You don’t need to be smart.

You need to be disciplined.

Simple strategies—like investing in diversified index funds and holding long-term—have historically outperformed most complex strategies.

Why the Top Investing Myths That Are Keeping You Poor Still Persist in 2026

The Top Investing Myths That Are Keeping You Poor persist because they feel emotionally safe. Believing that investing is risky, complicated, or reserved for the wealthy protects people from discomfort.

But these myths don’t protect your future.

They quietly destroy it.

If you truly want financial freedom, you must identify and eliminate the Top Investing Myths That Are Keeping You Poor before they compound into decades of missed opportunity.

Myth #6: “Real Estate Is the Only Way to Get Rich”

Definition of the Myth

This myth claims that real estate is the superior—or only—path to wealth.

Why This Myth Exists

Real estate is:

- Tangible

- Visible

- Discussed widely in media

- Associated with millionaires and passive income

TV shows, podcasts, and social media glorify:

- Rental properties

- House flipping

- Real estate portfolios

This creates the perception that:

If you’re not investing in property, you’re missing out.

Why This Myth Is Limiting

Real estate is just one asset class.

It comes with:

- Large upfront capital requirements

- Mortgage debt

- Maintenance costs

- Property taxes

- Insurance

- Tenant management

- Illiquidity (hard to sell quickly)

- Geographic concentration risk

For many people, these barriers make real estate:

- Inaccessible

- Stressful

- Unattractive

The Truth

You can build wealth through:

- Stocks

- Bonds

- Index funds

- ETFs

- Retirement accounts

- Businesses

- Royalties

- Intellectual property

- Online ventures

Real estate can be part of a diversified portfolio—but it is not mandatory.

Myth #7: “You Have to Be Lucky to Get Rich Investing”

Definition of the Myth

This myth suggests that wealth is primarily the result of luck—being in the right place at the right time.

Why This Myth Exists

People focus on:

- Early investors in Apple, Amazon, Tesla, Bitcoin

- Stories of overnight millionaires

- Viral success stories

These narratives ignore:

- Decades of consistent investing

- Thousands of unnoticed failures

- Survivorship bias

What Is Survivorship Bias?

Survivorship bias occurs when:

- We only see the success stories.

- We ignore the countless failures.

Example:

- You hear about one crypto millionaire.

- You don’t hear about the millions who lost money.

Why This Myth Is Harmful

If wealth is perceived as luck-based:

- People feel powerless.

- They take extreme risks.

- Or they avoid investing entirely.

The Truth

Wealth is built through process, not prediction.

You don’t need to pick the next Apple.

You need to:

- Invest regularly

- Stay invested

- Reinvest dividends

- Avoid emotional decisions

- Let time do the work

This is not luck.

This is math + discipline + time.

Myth #8: “Debt Must Be Eliminated Before You Can Invest”

Definition of the Myth

This myth claims that all debt must be paid off before any investing can begin. This is one of the most dangerous patterns behind the Top Investing Myths That Are Keeping You Poor because it encourages inaction.

Why This Myth Exists

Debt is often framed as evil—and for good reason. High-interest consumer debt (credit cards, payday loans) can destroy financial stability.

This leads people to believe:

“I must be 100% debt-free before I invest.”

Why This Myth Can Delay Wealth Building

While eliminating high-interest debt is essential, waiting to be completely debt-free before investing can:

- Delay compounding

- Miss employer retirement matches

- Reduce long-term wealth

Understanding Good Debt vs. Bad Debt

Bad Debt:

- High-interest

- Non-productive

- Used for consumption

Examples: - Credit cards

- Payday loans

- High-interest personal loans

Good (or Neutral) Debt:

- Low-interest

- Used to acquire assets or increase earning potential

Examples: - Student loans

- Mortgages

- Business loans

The Truth

You can often:

- Pay down high-interest debt and

- Invest simultaneously

Example

If your employer offers:

- A 401(k) match of 100% up to 5% of your salary

Not contributing means you’re:

- Giving up a guaranteed 100% return on your money.

Even while paying off debt, it often makes sense to:

- Contribute enough to capture the match.

The goal is balance, not perfection.

Myth #9: “You Need to Actively Trade to Make Real Money”

Definition of the Myth

This myth claims that real wealth comes from:

- Day trading

- Options trading

- Crypto speculation

- High-frequency trading

- Constant buying and selling

Why This Myth Exists

Media glamorizes:

- Traders making fast money

- Screens filled with charts

- Dramatic wins and losses

- “Get rich quick” narratives

Social media amplifies:

- Success stories

- Flashy lifestyles

- Overnight profits

Why This Myth Is Dangerous

Active trading:

- Increases transaction costs (commissions, spreads)

- Increases taxes (short-term capital gains)

- Increases emotional stress

- Increases the probability of mistakes

- Encourages impulsive behavior

Most active traders lose money over time.

The Truth

Long-term, low-cost, passive investing has historically outperformed most active strategies. Research from Vanguard consistently shows that disciplined, long-term investors in diversified index funds outperform the majority of active traders over time.

Wealth is built:

- Slowly

- Quietly

- Boringly

And boring is beautiful.

Myth #10: “The Stock Market Is Rigged Against Regular People”

Definition of the Myth

This myth claims that:

- Markets are unfair.

- Institutions always win.

- Individual investors are doomed.

Why This Myth Exists

Scandals, financial crises, and institutional advantages fuel distrust.

People see:

- Insider trading cases

- Market manipulation

- High-frequency trading

- Corporate bailouts

This creates a sense of injustice and helplessness.

Why This Myth Is Paralyzing

It leads to:

- Cynicism

- Avoidance

- Financial stagnation

- Missed opportunities

The Truth

While markets are not perfect, they are one of the greatest wealth-building tools ever created.

Over long periods, global markets have consistently grown as:

- Businesses innovate

- Technology advances

- Productivity increases

- Populations grow

You don’t need to beat professionals.

You just need to participate.

Myth #11: “I’m Too Old to Start Investing”

Definition of the Myth

This myth suggests that if you didn’t start investing young, it’s now pointless to begin.

Why This Myth Exists

People compare themselves to:

- Those who started in their 20s

- Early retirees

- Financial influencers

This creates:

- Regret

- Shame

- Paralysis

Why This Myth Is False

While starting earlier is better, starting later is still powerful.

Even in your:

- 40s

- 50s

- 60s

You still have:

- Years of compounding

- Time to improve your financial security

- Opportunities to reduce financial stress

The Truth

The best time to start was earlier.

The second-best time is now.

Myth #12: “Saving Money Is the Same as Investing”

Definition of the Myth

This myth assumes that saving and investing are interchangeable.

Why This Myth Exists

Both involve:

- Setting money aside

- Delaying consumption

- Financial discipline

This leads people to believe:

“If I’m saving, I’m building wealth.”

Why This Myth Is Dangerous

Saving protects money.

Investing grows money.

If you only save and never invest:

- Inflation erodes your purchasing power.

- Your money stagnates.

- You remain dependent on labor income.

The Truth

You need both:

Savings:

- Emergency fund

- Short-term goals

- Financial security

- Liquidity

Before investing heavily, make sure you’ve built financial stability (see our complete guide on how to build a 6-month emergency fund).

Investments:

- Long-term wealth

- Retirement

- Financial independence

- Passive income

They serve different purposes—and both are essential.

Myth #13: “Financial Advisors Will Make Me Rich”

Definition of the Myth

This myth assumes that hiring a financial advisor guarantees better financial outcomes.

Why This Myth Exists

People trust:

- Experts

- Professionals

- Authority figures

They assume:

“If someone is a financial advisor, they must know how to make me rich.”

Why This Myth Is Misleading

No advisor can:

- Control markets

- Predict the future

- Eliminate risk

Some advisors:

- Charge high fees

- Sell commission-based products

- Underperform simple strategies

The Truth

A good advisor can provide:

- Structure

- Education

- Accountability

- Behavioral coaching

But you are responsible for your financial outcomes.

Wealth is built by consistent behavior, not outsourcing decisions.

Myth #14: “If the Economy Is Bad, Investing Is Pointless”

Definition of the Myth

This myth suggests that investing only works during economic growth and stability. This is one of the most dangerous patterns behind the Top Investing Myths That Are Keeping You Poor because it encourages inaction.

Why This Myth Exists

Recessions, inflation, political instability, and global crises create fear and uncertainty.

People associate:

- Bad economy = bad investments

Why This Myth Is Wrong

Some of the best investing opportunities occur during:

- Recessions

- Market downturns

- Periods of pessimism

Historically:

- Markets fall.

- Then they recover.

- Then they reach new highs.

According to historical S&P 500 return data, the market has delivered positive long-term returns despite recessions, wars, and financial crises.

The Truth

Economic uncertainty is not a signal to stop investing.

It’s often a signal to stay disciplined.

Myth #15: “I’ll Figure Out Investing Later”

Definition of the Myth

This myth postpones investing indefinitely.

Why This Myth Exists

People prioritize:

- Bills

- Family

- Career

- Health

- Immediate needs

Investing feels:

- Abstract

- Distant

- Non-urgent

Why This Myth Is Costly

“Later” often becomes:

- Next year

- Next decade

- Never

And every year of delay reduces the power of compounding.

The Truth

You don’t need to master investing today.

You need to start today.

Progress beats perfection.

The Psychology Behind Investing Myths

These myths persist because they protect us from discomfort:

- Fear of loss

- Fear of failure

- Fear of looking ignorant

- Fear of responsibility

- Fear of uncertainty

Avoiding investing feels safer than confronting uncertainty.

But emotional comfort today often leads to financial discomfort tomorrow.

Wealth requires:

- Delayed gratification

- Emotional regulation

- Long-term thinking

- Personal responsibility

These skills must be trained.

How the Top Investing Myths That Are Keeping You Poor Destroy Long-Term Wealth

The Cost of Believing These Myths

Let’s quantify the cost.

The Real Cost of the Top Investing Myths That Are Keeping You Poor

Person A: Believes the Myths

- Waits until 40 to invest

- Saves in cash

- Avoids markets

- Invests irregularly

- Panics during downturns

Person B: Rejects the Myths

- Starts investing at 25

- Invests monthly

- Uses diversified funds

- Reinvests dividends

- Stays invested through volatility

After 40 years, Person B is likely to have hundreds of thousands—or millions—more than Person A.

Not because they were smarter.

Not because they were luckier.

Because they believed better stories.

What to Believe Instead: The Wealth-Building Truths

Replace myths with these truths:

- Investing is for everyone.

- You don’t need much money to start.

- Time matters more than timing.

- Consistency beats intelligence.

- Diversification reduces risk.

- Behavior determines results.

- Wealth is built slowly and steadily.

- Markets reward patience.

- Your future is shaped by today’s decisions.

- You are capable of building wealth.

Breaking Free from the Top Investing Myths That Are Keeping You Poor

Step-by-Step Action Plan

Here’s how to move from belief to action:

Step 1: Start Small

Open an investment account and start with an amount that feels easy—even $10.

Step 2: Automate

Set up automatic monthly contributions so investing becomes a habit, not a decision.

Step 3: Diversify

Use broad-market index funds or ETFs to spread risk across:

- Industries

- Countries

- Asset classes

If you’re unsure where to start, explore our guide on the best index funds for beginners.

Step 4: Stay Consistent

Invest every month, regardless of:

- Market conditions

- News headlines

- Economic cycles

Step 5: Ignore Noise

Stop reacting to:

- Daily market news

- Social media hype

- Fear-based headlines

Focus on your long-term plan.

Step 6: Increase Over Time

As your income grows:

- Increase your contributions.

- Raise your savings rate.

- Accelerate compounding.

Step 7: Reinvest Returns

Reinvest:

- Dividends

- Capital gains

- Interest

Let compounding work for you.

Final Thoughts: The Real Reason Most People Stay Poor

The Top Investing Myths That Are Keeping You Poor are not just financial misunderstandings — they are mental barriers that quietly block long-term wealth creation.

If you eliminate the Top Investing Myths That Are Keeping You Poor, you immediately increase your financial trajectory for decades to come.

It’s often a lack of belief in one’s ability to build wealth.

The biggest barrier to financial success is not:

- Income

- Education

- Economy

- Government

- Technology

It’s mindset.

Every wealthy person started where you are now:

- With uncertainty

- With fear

- With imperfect knowledge

- With doubt

The difference?

They acted anyway.

You don’t need to know everything.

You don’t need to be perfect.

You just need to begin.