401(k) vs IRA is one of the most important retirement investing decisions you’ll ever make. Choosing the right account—and knowing which one to max first—can significantly impact your long-term wealth, taxes, and retirement lifestyle.

One of the most common and important questions investors ask is:

“Should I max my 401(k) first or my IRA?”

At first glance, both seem similar. Both offer tax advantages. Both are designed for retirement. Both can grow your wealth significantly over time.

But the order in which you invest in them can easily mean a difference of hundreds of thousands—or even millions—of dollars over your lifetime.

This guide breaks everything down in simple but powerful detail:

- What a 401(k) is (with full explanation)

- What an IRA is (Traditional vs Roth)

- Key differences

- Strategic priority order (what to max first)

- Real-world case studies1q

- Mistakes to avoid

- A step-by-step decision framework

🧠 PART 1: What is a 401(k)?

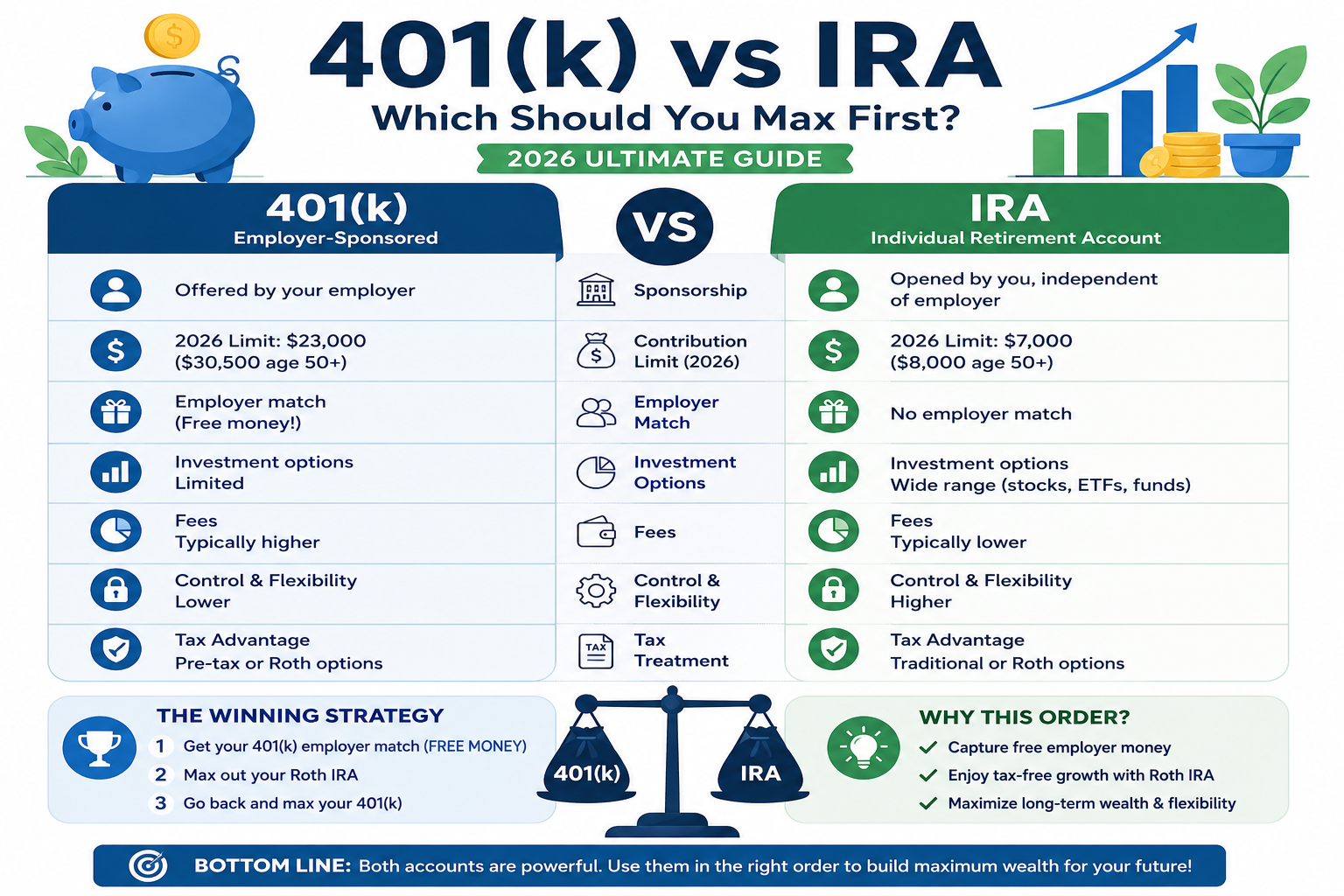

A 401(k) is an employer-sponsored retirement account in the United States.

🔹 Key Idea:

It allows you to invest a portion of your salary before or after taxes, depending on the type.

Types of 401(k)

1. Traditional 401(k)

- Contributions: Pre-tax

- Tax benefit: Reduces your taxable income today

- Withdrawals: Taxed in retirement

👉 Example:

If you earn $100,000 and contribute $10,000:

- You are taxed as if you earned $90,000

2. Roth 401(k)

- Contributions: After-tax

- Tax benefit: No immediate tax break

- Withdrawals: Tax-free in retirement

Contribution Limits (2026 Approx)

- $23,000 per year (under age 50)

- $30,500 (with catch-up contribution)

Employer Match (MOST IMPORTANT)

This is where the 401(k) becomes extremely powerful.

👉 Example:

- Employer matches 100% up to 5%

- You earn $100,000

- You contribute $5,000

- Employer adds $5,000

💡 That’s an instant 100% return on your money

Pros of 401(k)

✔ Employer match (free money)

✔ High contribution limit

✔ Automatic payroll deduction

✔ Tax advantages

Cons of 401(k)

❌ Limited investment options

❌ Fees can be high

❌ Less control compared to IRA

🧠 PART 2: What is an IRA? (Individual Retirement Account)

An IRA is a retirement account you open yourself—completely independent of your employer.

Types of IRA

1. Traditional IRA

- Contributions may be tax-deductible

- Taxes paid during withdrawal

2. Roth IRA (Most powerful for long-term wealth)

- Contributions are after-tax

- Withdrawals are 100% tax-free

Contribution Limits (2026 Approx)

- $7,000 per year

- $8,000 if age 50+

Income Limits (Important)

Roth IRA has income limits.

👉 Example:

- If you earn too much (~$150K+ single), you may not be able to contribute directly

(But there is a workaround: Backdoor Roth IRA)

Pros of IRA

✔ Full control over investments

✔ Lower fees

✔ Access to stocks, ETFs, index funds

✔ Roth IRA offers tax-free growth

Cons of IRA

❌ Lower contribution limit

❌ No employer match

❌ Income restrictions

⚔️ PART 3: 401(k) vs IRA — Core Differences

| Feature | 401(k) | IRA |

|---|---|---|

| Employer Sponsored | Yes | No |

| Contribution Limit | High | Lower |

| Employer Match | Yes | No |

| Investment Options | Limited | Wide |

| Fees | Higher | Lower |

| Control | Low | High |

| Roth Option | Yes | Yes |

🧠 PART 4: The Correct Strategy (What to Max First)

Now we answer the main question:

✅ Step-by-Step Priority Order

🥇 Step 1: Contribute to 401(k) up to Employer Match

This is non-negotiable.

👉 Why?

Because you are literally getting free money

💡 Not doing this = losing guaranteed returns

🥈 Step 2: Max Your Roth IRA

After capturing employer match:

👉 Move to IRA (preferably Roth)

Why?

✔ Tax-free growth

✔ Better investment options

✔ More flexibility

🥉 Step 3: Go Back and Max Your 401(k)

Once IRA is maxed:

👉 Return to 401(k) and contribute more

🏆 Final Order Summary:

- 401(k) → Employer Match

- Roth IRA → Max it

- 401(k) → Max remaining

📊 PART 5: Case Study (Real Wealth Impact)

Let’s compare two investors:

👤 Investor A (Wrong Strategy)

- Maxes 401(k) first

- Ignores Roth IRA

Result after 30 years:

- Total savings: $1.2M

- Tax paid in retirement: HIGH

👤 Investor B (Optimal Strategy)

- Takes employer match

- Maxes Roth IRA

- Then maxes 401(k)

Result after 30 years:

- Total savings: $1.4M

- Tax paid: LOW

💡 Difference:

👉 $200,000+ extra wealth

📈 PART 6: Compounding Example

Let’s assume:

- Investment: $7,000/year

- Return: 8%

- Time: 30 years

Final Value:

👉 ~$850,000

Now imagine:

- Roth IRA → Tax-free

- Traditional 401(k) → taxed at 25%

👉 You lose ~$200K+ in taxes

🧠 PART 7: When Should You Prioritize 401(k) First?

There are some exceptions.

Scenario 1: High Income + Tax Savings Needed

If you’re in a high tax bracket:

👉 Traditional 401(k) reduces taxes today

Scenario 2: No Access to Roth IRA

High earners may not qualify directly

Scenario 3: Employer Offers Excellent Plan

- Low fees

- Strong investment options

🧠 PART 8: When Should You Prioritize IRA First?

Scenario 1: Young Investor

- Lower tax bracket

- Roth IRA becomes extremely powerful

Scenario 2: You Want Flexibility

IRA allows:

✔ More investment choices

✔ Lower fees

✔ Easier withdrawals (contributions in Roth)

Scenario 3: Poor 401(k) Plan

If your employer offers:

❌ High fees

❌ Limited funds

👉 IRA is better

⚠️ PART 9: Biggest Mistakes to Avoid

❌ Mistake 1: Skipping Employer Match

This is the biggest mistake.

👉 It’s literally free money.

❌ Mistake 2: Ignoring Roth IRA

Many investors focus only on tax deduction today.

👉 But tax-free growth is far more powerful long-term.

❌ Mistake 3: Over-investing in 401(k) Early

Without IRA:

👉 You lose flexibility + control

❌ Mistake 4: Not Investing at All

Even the best strategy fails if:

👉 You don’t start

📊 PART 10: Advanced Strategy (For High Earners)

🔥 Backdoor Roth IRA

Used by high-income individuals.

Steps:

- Contribute to Traditional IRA

- Convert to Roth IRA

🔥 Mega Backdoor Roth (Advanced)

- Uses 401(k)

- Allows very large Roth contributions

🧠 PART 11: Real-Life Example (Detailed)

👨 Case: John (Age 30)

- Salary: $100,000

- Employer match: 5%

Strategy:

- Contribute $5,000 → get $5,000 match

- Max Roth IRA ($7,000)

- Add remaining to 401(k)

After 30 Years:

- 401(k): ~$1.2M

- Roth IRA: ~$900K

👉 Total: $2.1M+

Tax Impact:

- Roth portion: TAX-FREE

- 401(k): partially taxable

🧠 PART 12: Decision Framework (Simple Rule)

Ask yourself:

✅ Do I have employer match?

👉 YES → Start with 401(k)

✅ Do I qualify for Roth IRA?

👉 YES → Max it next

✅ Do I want tax-free income later?

👉 YES → Prioritize Roth

✅ Am I in high tax bracket now?

👉 YES → Use 401(k) more

Frequently Asked Questions About 401(k) vs IRA

🏁 FINAL CONCLUSION

If you remember only ONE thing from this entire guide, remember this:

👉 The correct order is:

✔ 401(k) → Employer Match

✔ Roth IRA → Max

✔ 401(k) → Max

💡 Why This Works:

- You capture free money

- You secure tax-free growth

- You maximize long-term compounding

🚀 Final Thought

Building wealth isn’t about choosing one account over another.

It’s about using the right accounts in the right order.

Most people get this wrong—and that’s why they retire with less money than they should.

But if you follow this strategy consistently:

👉 You put yourself in the top 5% of disciplined investors.