Roth IRA vs Traditional IRA: Which Retirement Account Is Better in 2026?

Retirement planning is not only about investing money. It is also about understanding taxes, compounding, future income, and long-term financial freedom. One of the biggest decisions investors face is choosing between a Roth IRA and a Traditional IRA.

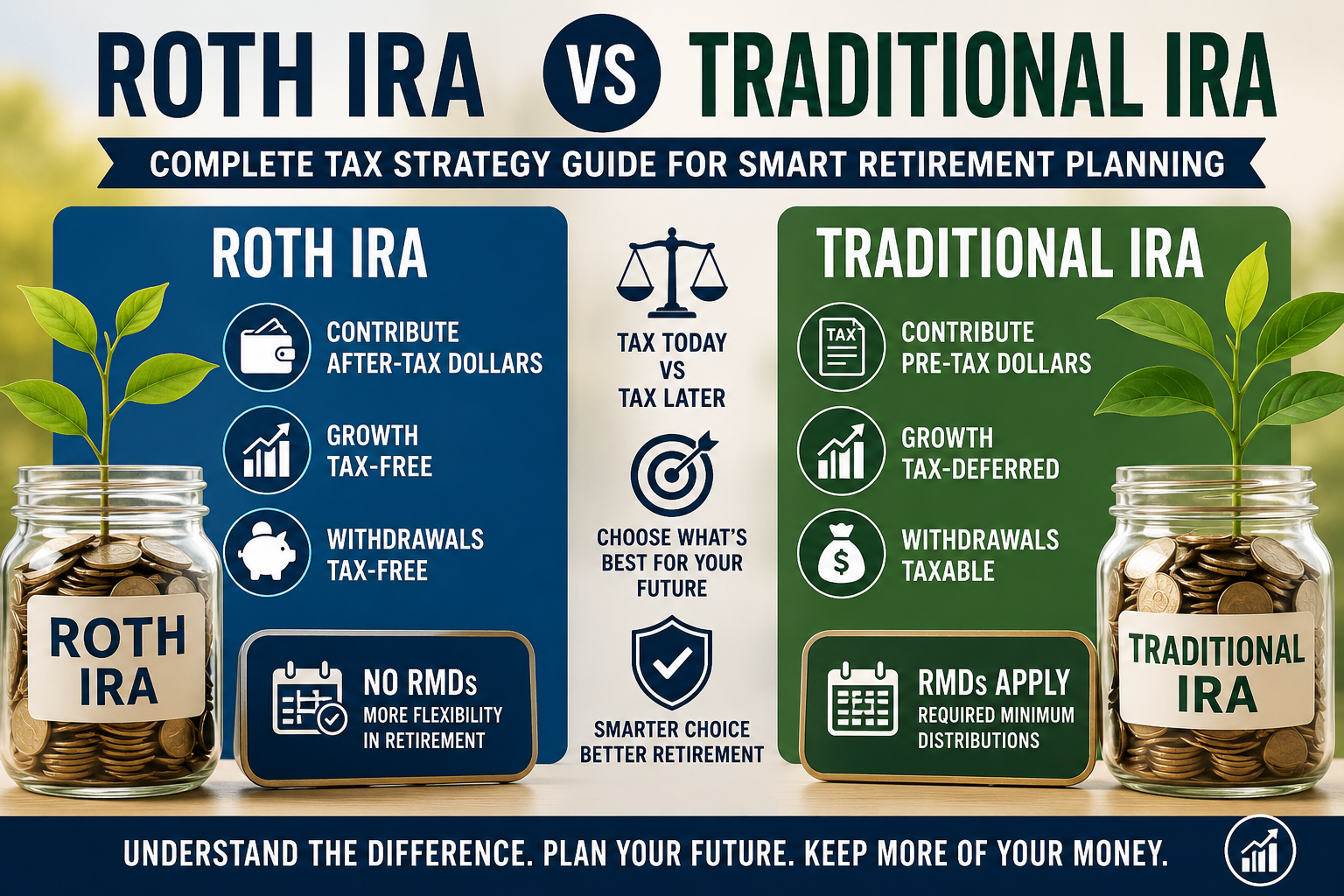

Both accounts are designed to help people save for retirement while receiving tax advantages from the government. However, the timing of taxes is completely different.

A Traditional IRA gives tax benefits today but taxes you later.

A Roth IRA taxes you today but gives tax-free income in retirement.

This single difference can potentially impact your wealth by hundreds of thousands of dollars over your lifetime.

In this complete tax strategy guide, you will learn:

- What a Roth IRA is

- What a Traditional IRA is

- Major differences between both accounts

- Tax strategies used by wealthy investors

- Which IRA is better for your income level

- Real-life case studies and examples

- Common mistakes to avoid

- Best retirement planning strategies for 2026

What Is an IRA and How Does It Work?

IRA stands for Individual Retirement Account.

It is a special investment account created to help individuals save for retirement with tax advantages. When comparing Roth IRA vs Traditional IRA, investors must understand how taxes impact long-term wealth accumulation.

Unlike a normal savings account, an IRA allows investments such as:

- Stocks

- ETFs

- Mutual funds

- Bonds

- Index funds

The two most popular types of IRAs are:

- Traditional IRA

- Roth IRA

Both help retirement savings grow over time through compounding, but the tax treatment is very different.

Understanding the Core Difference Between Roth IRA and Traditional IRA

The biggest difference comes down to one question:

When do you want to pay taxes?

Traditional IRA

- Tax benefit now

- Taxes later

Roth IRA

- Taxes now

- Tax-free later

This sounds simple, but it affects your:

- Retirement income

- Tax bracket

- Wealth growth

- Financial flexibility

What Is a Traditional IRA in Retirement Planning?

A Traditional IRA is a retirement account where contributions may be tax-deductible.

This means you may reduce your taxable income today while allowing investments to grow tax-deferred.

However, withdrawals during retirement are taxed as ordinary income.

How Traditional IRA Works

Let’s understand with an example.

Suppose:

- Your annual salary = $90,000

- IRA contribution = $7,000

If contributions are deductible, your taxable income becomes:

$90,000 − $7,000 = $83,000

This reduces your current tax bill.

Your investments then grow without yearly taxes until retirement.

But later, when you withdraw money, the government taxes those withdrawals.

Key Features of Traditional IRA

1. Tax Deduction

Contributions may reduce taxable income.

This is especially beneficial for high-income earners.

2. Tax-Deferred Growth

You do not pay yearly taxes on:

- Dividends

- Interest

- Capital gains

This allows faster compounding.

3. Taxable Withdrawals

Withdrawals after retirement are taxed as ordinary income.

4. Required Minimum Distributions (RMDs)

The government forces withdrawals starting around age 73.

Even if you do not need the money, you must withdraw and pay taxes.

Advantages of Traditional IRA

Immediate Tax Savings

High earners often prefer Traditional IRAs because they lower current taxes.

Useful During Peak Earning Years

If your tax bracket is high today, tax deductions become more valuable.

Potentially Lower Retirement Taxes

Many retirees have lower income after retirement.

This may reduce their tax rate later.

Disadvantages of Traditional IRA

Taxes in Retirement

Every withdrawal becomes taxable income.

Required Withdrawals

RMDs reduce flexibility.

Future Tax Uncertainty

Nobody knows future tax rates.

Higher future taxes can reduce retirement income significantly.

What Is a Roth IRA?

A Roth IRA is a retirement account funded with after-tax money.

You pay taxes now, but qualified withdrawals later are completely tax-free.

This is one of the biggest advantages in investing.

How Roth IRA Works

Suppose:

- Annual contribution = $7,000

- Investment period = 30 years

- Average return = 8%

Your investment could potentially grow to hundreds of thousands of dollars.

With a Roth IRA:

- No tax on growth

- No tax on withdrawals

- No tax on gains

Key Features of Roth IRA

1. After-Tax Contributions

You contribute money that has already been taxed.

2. Tax-Free Growth

All investment gains grow tax-free.

3. Tax-Free Retirement Withdrawals

If rules are followed:

- Age 59½ or older

- Account open for at least 5 years

Withdrawals become completely tax-free.

4. No Required Minimum Distributions

Unlike Traditional IRAs, Roth IRAs have no RMDs during the owner’s lifetime.

This gives greater retirement flexibility.

Advantages of Roth IRA

Tax-Free Retirement Income

This is the biggest benefit.

Ideal for Long-Term Compounding

Young investors benefit massively from decades of tax-free growth.

No RMDs

Money can continue growing tax-free for life.

Better Estate Planning

Roth IRAs are useful for passing wealth to heirs efficiently.

Disadvantages of Roth IRA

No Immediate Tax Deduction

You do not reduce taxes today.

Income Limits Apply

High-income earners may not qualify directly.

Roth IRA vs Traditional IRA: Side-by-Side Comparison

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Tax Benefit | Now | Later |

| Contributions | Often deductible | After-tax |

| Growth | Tax-deferred | Tax-free |

| Withdrawals | Taxable | Tax-free |

| RMDs | Yes | No |

| Best For | High earners | Young investors |

| Future Flexibility | Moderate | High |

The Roth IRA vs Traditional IRA decision depends largely on your current income, future tax expectations, and retirement timeline.

The Most Important Concept: Future Tax Rate

The best IRA depends largely on your future tax rate.

Choose Traditional IRA If:

You believe your retirement tax rate will be lower than your current tax rate.

Choose Roth IRA If:

You believe your future tax rate will be higher.

This is why younger investors often prefer Roth IRAs.

Why Young Investors Usually Prefer Roth IRA

Young workers often:

- Earn lower salaries

- Have lower tax brackets

- Have long investment horizons

This creates the perfect Roth IRA environment.

Example of Roth IRA Power

Suppose a 25-year-old invests:

- $7,000 yearly

- For 40 years

- At 8% annual return

Potential portfolio value:

Over $1.8 million.

If tax-free, retirement becomes significantly more powerful.

Why High-Income Earners Often Prefer Traditional IRA

A person earning:

- $250,000 annually

- In a high tax bracket

May value tax deductions more than future tax-free withdrawals.

Immediate tax reduction can save thousands every year.

Case Study 1: Young Professional

Profile

- Age: 24

- Income: $55,000

- Tax bracket: Low

- Retirement timeline: 35+ years

Best Option

Roth IRA.

Why?

- Low taxes today

- Long compounding period

- Future earnings likely higher

This investor locks in low tax rates permanently. These Roth IRA vs Traditional IRA examples show how different tax strategies work for different income levels.

Case Study 2: Mid-Career Executive

Profile

- Age: 45

- Income: $220,000

- High tax bracket

Best Option

Traditional IRA.

Why?

- Immediate tax deduction valuable

- Likely lower retirement income later

Case Study 3: FIRE Investor

FIRE means:

Financial Independence, Retire Early.

These investors often retire in their 40s or 50s.

Best Strategy

Combination approach:

- Roth IRA

- Traditional IRA

- Taxable brokerage account

This creates tax diversification.

What Is Tax Diversification?

Tax diversification means holding investments in different tax categories.

Examples:

- Tax-free accounts

- Tax-deferred accounts

- Taxable accounts

This provides flexibility during retirement withdrawals.

Understanding Roth Conversion

A Roth conversion moves money from:

Traditional IRA → Roth IRA.

You pay taxes now to gain tax-free future growth.

Why Investors Use Roth Conversions

1. Lower Future Taxes

Convert during low-income years.

2. Market Downturn Opportunities

If investments fall temporarily, conversion taxes become lower.

3. Long-Term Tax-Free Growth

Future gains become tax-free forever.

Roth Conversion Example

Suppose:

- Traditional IRA balance = $100,000

- Market crash reduces value to $70,000

Converting at $70,000 means lower taxes.

If the account later grows back to $150,000:

Future gains become tax-free.

What Is a Backdoor Roth IRA?

High earners sometimes exceed Roth IRA income limits.

The solution is called a Backdoor Roth IRA.

How Backdoor Roth Works

Step 1:

Contribute to Traditional IRA.

Step 2:

Convert to Roth IRA.

This strategy is widely used by high-income professionals.

Importance of Compound Interest

Compound interest is the engine behind retirement wealth.

It means earning returns on previous returns.

Albert Einstein reportedly called compounding the “eighth wonder of the world.”

Example of Compounding

Suppose:

- Initial investment = $10,000

- Return = 8%

- Time = 30 years

Future value becomes approximately:

$100,000+

Time matters more than contribution size.

Roth IRA and Long-Term Compounding

Tax-free compounding is extremely powerful.

Imagine:

- 40 years of growth

- No capital gains taxes

- No dividend taxes

- No withdrawal taxes

This creates enormous wealth-building potential.

Common Retirement Tax Mistakes

1. Ignoring Future Taxes

Many investors focus only on current tax savings.

This can backfire later.

2. Starting Too Late

Time is the biggest retirement advantage.

3. Depending Only on Traditional Accounts

This creates future tax concentration risk.

4. Not Using Employer Match

Employer 401(k) matching is essentially free money.

How Inflation Impacts Retirement Accounts

Inflation reduces purchasing power over time.

For example:

- $100 today

- May buy far less in 30 years

This is why investing matters.

Cash savings alone often fail to beat inflation.

Best Investments Inside an IRA

Popular investments include:

Index Funds

Low-cost diversified investments tracking market indexes.

ETFs

Exchange-traded funds offering flexibility and diversification.

Dividend Stocks

Provide passive income.

Growth Stocks

Higher risk but higher long-term growth potential.

Asset Allocation Strategy by Age

Age 20–35

Focus on growth:

- Stocks

- Index funds

- Roth IRA priority

Age 35–50

Balanced approach:

- Stocks

- Bonds

- Mixed IRA strategy

Age 50+

Focus on stability:

- Income generation

- Tax planning

- Withdrawal strategy

Withdrawal Strategies During Retirement

Smart withdrawals reduce taxes.

A common strategy:

- Taxable accounts first

- Traditional IRA second

- Roth IRA last

This allows Roth investments to continue compounding tax-free.

Why Roth IRA Is Powerful During Market Growth

Fast-growing investments benefit most inside Roth accounts.

Because future gains become tax-free.

Examples include:

- Growth ETFs

- Technology stocks

- Broad market index funds

Traditional IRA and Tax Arbitrage

Tax arbitrage means paying taxes at lower rates later.

This is the main Traditional IRA strategy.

Example:

- Current tax bracket = 35%

- Retirement tax bracket = 20%

You win through lower future taxation.

Retirement Planning in 2026

Modern retirement planning involves:

- Tax efficiency

- Inflation management

- Diversification

- Long-term compounding

Simply saving money is no longer enough.

Which IRA Is Better for Most People?

There is no universal answer.

But generally:

Roth IRA Often Wins For:

- Young investors

- Long-term investors

- People expecting higher future income

Traditional IRA Often Wins For:

- High-income earners

- People near retirement

- Investors expecting lower future taxes

Ideal Strategy for Many Investors

Many financial experts recommend using both.

This creates:

- Tax flexibility

- Better withdrawal planning

- Lower lifetime taxes

Beginner-Friendly Retirement Blueprint

Step 1

Build emergency savings.

Step 2

Capture employer 401(k) match.

Step 3

Maximize Roth IRA or Traditional IRA.

Step 4

Invest consistently every month.

Step 5

Increase contributions over time.

Final Thoughts on Roth IRA vs Traditional IRA

The Roth IRA vs Traditional IRA debate is ultimately about tax timing.

Traditional IRA:

Save taxes now, pay later.

Roth IRA:

Pay taxes now, avoid taxes later.

The best choice depends on:

- Your current income

- Future earning potential

- Retirement goals

- Tax expectations

- Investment timeline

For many young investors, Roth IRA offers extraordinary long-term benefits because of tax-free compounding.

For higher-income earners, Traditional IRA can provide powerful immediate tax savings.

The smartest investors often combine both strategies to maximize flexibility and minimize taxes throughout retirement.

Frequently Asked Questions (FAQs)

Is Roth IRA better than Traditional IRA?

Not always. Roth IRA is often better for younger investors with lower current tax rates. Traditional IRA may benefit high earners more.

Can I have both Roth and Traditional IRA?

Yes. Many investors use both for tax diversification.

Which is better: Roth IRA vs Traditional IRA?

The answer depends on your tax bracket, retirement goals, and future income expectations.

Which IRA grows faster?

Investment growth depends on the investments themselves. However, Roth IRA growth is tax-free.

Do I pay taxes on Roth IRA withdrawals?

Qualified withdrawals are tax-free.

What is the biggest advantage of a Roth IRA?

Tax-free retirement income.

What is the biggest advantage of a Traditional IRA?

Immediate tax deduction.

Why Roth IRA vs Traditional IRA Matters in 2026

As tax laws, inflation, and retirement costs continue changing, understanding Roth IRA vs Traditional IRA becomes increasingly important for long-term wealth preservation. Investors who create a tax-efficient retirement strategy today can potentially save thousands of dollars in future taxes while maximizing investment growth through compounding.

Conclusion

Retirement investing is not just about earning returns. It is about keeping more of your money after taxes.

Understanding Roth IRA vs Traditional IRA can dramatically impact your financial future.

The earlier you start investing and the smarter your tax strategy becomes, the greater your long-term wealth potential.

Whether you choose Roth IRA, Traditional IRA, or both, the most important step is starting early and investing consistently for the future.

Choosing between Roth IRA vs Traditional IRA can significantly impact your retirement income and long-term financial freedom.