The 50/30/20 Rule Explained is one of the simplest and most powerful budgeting strategies you can use in 2026 to manage your money effectively.

In the financial landscape of 2026, the traditional concepts of “saving for a rainy day” have been upended by a whirlwind of economic shifts. We are navigating a “New Normal” characterized by high-interest rates, the dominance of the subscription economy, and a housing market that often feels impenetrable.

Whether you are a Gen Z professional entering a volatile job market or a seasoned earner trying to protect your wealth against inflation, the fundamental question remains: How do I manage my money without feeling like I’m suffocating?

The answer lies in a framework that is over two decades old but more relevant than ever: The 50/30/20 Rule

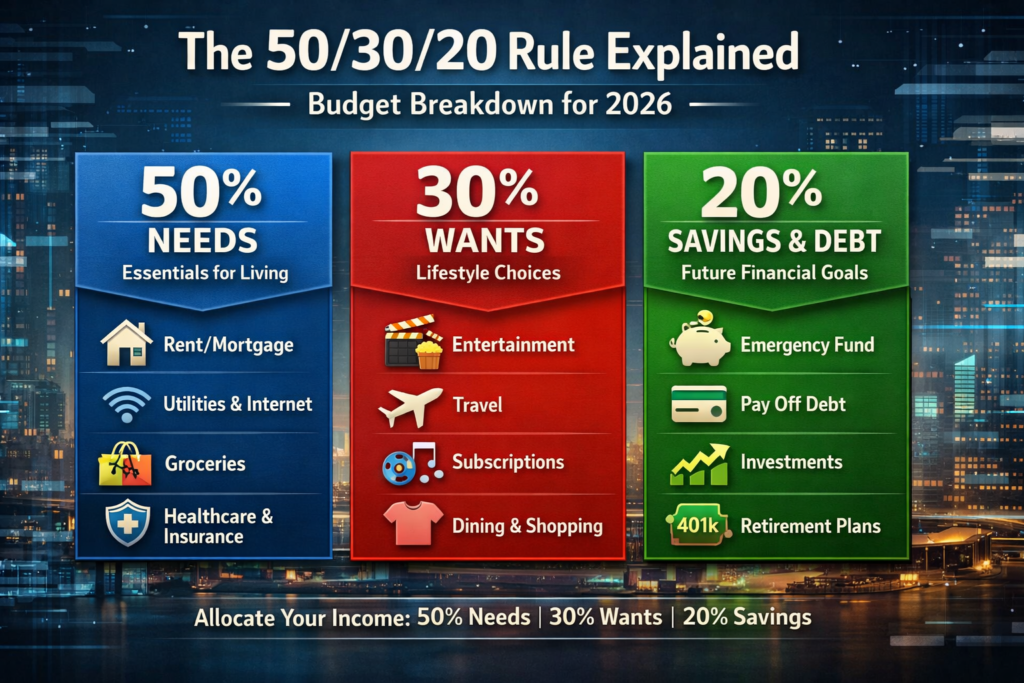

The 50/30/20 Rule Explained helps you divide your income into three simple categories: needs, wants, and savings. This method simplifies budgeting and makes financial planning easier for beginners and professionals alike.

Pro Tip: Bookmark this page and follow the steps after watching.

50% Needs → Essentials like rent, food, bills

30% Wants → Lifestyle spending like travel, dining

20% Savings → Investments, emergency fund, debt payoff

This chart helps you quickly understand how to allocate your income without overcomplicating your budget. It’s one of the easiest ways to stay financially disciplined in 2026.

Chapter 1: The Intellectual Foundation of the 50/30/20 Rule

To use a tool effectively, you must understand its design. The 50/30/20 rule was popularized by Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, in their seminal work, All Your Worth: The Ultimate Lifetime Money Plan.

1.1 Beyond the Spreadsheet: A Macro Approach

Most budgets fail because they are too granular. They ask you to track every cup of coffee or every pack of gum. This leads to “budgeting burnout”—a state where the mental energy required to track the money exceeds the benefit of saving it.

The 50/30/20 rule is a macro-budgeting tool. It focuses on the big picture, dividing your financial life into three distinct buckets. In 2026, where digital transactions happen in milliseconds, having three broad categories is the only way to maintain sanity.

1.2 The Psychological Edge: Permission to Spend

The rule works because it eliminates decision fatigue. When you know exactly how much “permission” you have to spend on fun (Wants) and how much is non-negotiable (Needs), the guilt associated with spending evaporates. It transforms money from a source of constant anxiety into a tool for empowerment.

Chapter 2: The Foundation – Calculating “After-Tax Income”

The biggest mistake beginners make is applying these percentages to their gross salary. In 2026, with complex tax brackets and various payroll deductions, your “Gross Pay” is a phantom number.

2.1 Defining Net Income (Take-Home Pay)

After-tax income is the actual amount that hits your bank account. To calculate this accurately, you must look at your pay stub and identify what stays and what goes.

To calculate your base number, subtract:

- Federal, State, and Local Income Taxes: The mandatory cut the government takes.

- Social Security/National Insurance: Mandatory contributions to state pensions or safety nets.

- Medicare/Healthcare Levies: Mandatory health-related taxes.

2.2 The “Deduction” Trap: Automated Savings

In 2026, many employers automatically deduct 401(k) or pension contributions.

- The Rule: If you are contributing to a retirement plan before the money hits your bank account, you should add that amount back to your net income to see your true “Savings” percentage. If you don’t, you might think you aren’t saving enough when, in reality, you are already hitting your 20% goal via payroll.

Detailed Example:

John’s Monthly Pay Stub:

- Gross Salary: $6,000

- Income Tax: -$1,100

- Social Security: -$350

- Health Insurance Premium: -$250

- 401(k) Contribution: -$500

- Actual Bank Deposit: $3,800

To apply the 50/30/20 rule correctly, John should add back his $500 401(k) contribution. His “Budgeting Net Income” is $4,300.

Chapter 3: The 50% Category – The “Needs” (The Non-Negotiables)

The “Needs” category is the bedrock of your financial stability. These are expenses that, if left unpaid, would severely impact your life, health, or ability to earn income.

3.1 What Qualifies as a Need in 2026?

The definition of a “Need” has evolved. In 2026, we categorize these as:

- Shelter: This includes rent or mortgage payments, property taxes, and home insurance.

- Utilities: Electricity, water, and heating.

- Connectivity: In 2026, high-speed internet and a mobile data plan are no longer luxuries; they are utilities required for banking, remote work, and basic communication.

- Food: Basic groceries. This covers the sustenance required for a healthy diet. (Note: This does not include luxury food items or dining out).

- Transportation: Public transit passes, or fuel and insurance for a modest, reliable vehicle.

- Healthcare: Insurance premiums, co-pays, and essential medications.

- Minimum Debt Payments: You must pay the minimum on your credit cards, student loans, and car notes to protect your credit score.

3.2 The “Gray Area”: Needs vs. Wants

This is where most budgeting efforts fail. People “self-justify” wants into needs.

- The Car: A vehicle that safely gets you to work is a Need. A luxury sedan with heated leather seats and a $800 monthly payment is a Want disguised as a need.

- The Apartment: A safe, clean place to sleep is a Need. A penthouse with a gym and concierge is a Want.

3.3 Managing the 50% in High-Cost-of-Living (HCOL) Areas

In Tier-1 cities like New York, London, or Sydney, housing alone can swallow 50% of your income.

- The Strategy: If your Needs exceed 50%, you are “financially fragile.” You must either reduce your “Wants” (the 30% bucket) to compensate or work toward increasing your income. You cannot ignore the 20% savings goal; otherwise, you are simply working to pay rent.

Chapter 4: The 30% Category – The “Wants” (Lifestyle Choices)

This is the “Lifestyle” bucket. It is the most flexible part of your budget and the first place to cut when the economy takes a downturn.

4.1 The Importance of Enjoyment

Budgeting is not about suffering; it’s about intentionality. The 50/30/20 rule is unique because it encourages you to spend 30% on yourself. This prevents the “rebound effect” where you live too frugally for three months and then go on a massive, unplanned shopping spree.

4.2 Common 2026 “Wants”:

- Dining and Socializing: Every coffee shop visit, brunch, or dinner out.

- Entertainment: Cinema tickets, concerts, and sporting events.

- The Subscription Economy: Netflix, Disney+, Spotify, specialized SaaS tools for hobbies, and gym memberships.

- Travel: Your annual holiday or weekend getaways.

- Aesthetics: Designer clothing beyond basic needs, high-end grooming, and home decor.

4.3 The “Subscription Creep” Audit

In 2026, “Subscription Creep” is the silent killer of wealth. Small $10-$20 charges feel insignificant individually, but they often aggregate to $300-$500 monthly.

- The 48-Hour Rule: For any “Want” over $100, wait 48 hours before clicking “buy.” If the desire is still there and it fits in your 30% bucket, proceed.

Chapter 5: The 20% Category – The “Future” (Savings & Debt)

This is the most critical bucket for your long-term freedom. In 2026, this 20% isn’t just “money under the mattress”; it is your Exit Strategy from the 9-to-5 grind.

5.1 The Savings Hierarchy

You should allocate this 20% in the following order of operations:

- The Starter Emergency Fund: Save $2,000 immediately. This is your “peace of mind” fund for a flat tire or a broken tooth.

- High-Interest Debt: In 2026, credit card interest rates can exceed 25%. This is a financial emergency. Use your 20% bucket to crush any debt with an interest rate above 7%.

- The Full Emergency Fund: Once high-interest debt is gone, build 3 to 6 months of Needs (your 50% bucket) in a High-Yield Savings Account (HYSA).

- Investing for Wealth: Once you have a safety net, the 20% goes into the market—Index Funds, ETFs, and retirement accounts.

Read our guide on emergency funds to build a strong financial safety net.

5.2 The Compounding Power of 20%

If you consistently save 20% of your income starting at age 25, the math of compounding interest suggests you can retire comfortably with your current lifestyle by age 55-60.

Example: Saving $1,000/month (20% of a $5,000 income) at a 7% annual return results in $1.2 million over 30 years.

For long-term wealth creation, learn how to invest in index funds.

📚 Trusted Financial Resources

- Budgeting strategies recommended by the Federal Reserve highlight the importance of consistent saving habits.

- Tax planning insights from the Internal Revenue Service can help reduce liabilities and improve net income.

- Long-term investing through firms like Vanguard Group supports sustainable wealth creation.

Chapter 6: Real-World Scenarios (Tier-1 Market Examples)

Scenario A: The Entry-Level Professional (Toronto, Canada)

- Net Income: $4,000 CAD

- Needs (50%): $2,000 (Shared apartment, transit pass, basic groceries)

- Wants (30%): $1,200 (Dining out, streaming, weekend trips)

- Savings (20%): $800 (TFSA contributions and student loan extra payments)

Scenario B: The High-Earner (San Francisco, USA)

- Net Income: $12,000 USD

- Needs (50%): $6,000 (High rent, car insurance, premium groceries)

- Wants (30%): $3,600 (Luxury travel, high-end gym, hobbies)

- Savings (20%): $2,400 (Maxing out 401k and brokerage accounts)

Chapter 7: Adapting the Rule for 2026 Challenges

Critics often say the 50/30/20 rule is “too simple” for a “complex” world. Here is how to adapt it:

7.1 The “High-Rent” Pivot (60/20/20)

If you live in a city where rent takes up 40% of your income, your “Needs” will likely hit 60%. To maintain your future, you must not cut your 20% savings. Instead, you must cut your “Wants” to 20%.

7.2 The “Debt-Crusher” Pivot (50/10/40)

If you are drowning in debt, you should temporarily lower your “Wants” to the bare minimum (10%) and throw 40% of your income at your debt. This is a short-term sacrifice for a long-term gain.

Chapter 8: Tools for Implementation

In 2026, manual tracking is obsolete.

- AI-Budgeting Apps: Use tools that automatically categorize your transactions into Needs, Wants, and Savings.

- The “Two-Bank” System: Have one bank account for Needs/Bills and a separate account for Wants. When the “Wants” account hits zero, the fun stops until next month.

- Automated Transfers: Set your 20% savings to transfer to your investment account the minute your paycheck hits. If you don’t see it, you won’t spend it.

Chapter 9: Detailed Terminology and Examples

To reach a comprehensive understanding, let’s break down the technical terms used in the Tier-1 financial markets.

9.1 Amortization and Housing

In the “Needs” category, your mortgage isn’t just a payment; it’s an amortization schedule.

- Example: Early in a 30-year mortgage, most of your 50% bucket is going toward interest. By year 20, a larger portion goes toward equity. This equity eventually moves from a “Need” (payment) to an “Asset” (wealth).

9.2 Opportunity Cost in “Wants”

Every dollar in your 30% bucket has an opportunity cost.

- Example: A $1,500 vacation today is a “Want.” That same $1,500 invested in your 20% bucket could be worth $11,000 in 30 years. You don’t have to skip the vacation, but you should be aware of the trade-off.

Chapter 10: 2026 SEO Strategy

| Category | Typical 2026 Expenses | Tier-1 Market Nuance |

| Needs (50%) | Rent/Mortgage, Internet, Utilities, Basic Food, Insurance | High housing costs in London/NYC may require a 60% shift. |

| Wants (30%) | Streaming, Dining, Travel, Hobbies, Fashion | Subscription creep is the #1 danger here. |

| Savings (20%) | 401k, ISA, TFSA, High-Yield Savings, Extra Debt Pay | Interest rates in 2026 favor savers over borrowers. |

❓ The 50/30/20 Rule Explained – FAQs

What is the 50/30/20 rule?

The 50/30/20 rule explained simply divides your income into needs, wants, and savings.

Is the 50/30/20 rule still relevant in 2026?

Yes, the 50/30/20 rule explained remains relevant but requires adjustments based on lifestyle and inflation.

Can beginners use the 50/30/20 rule?

Yes, the 50/30/20 rule explained is perfect for beginners due to its simplicity.

Conclusion: Financial Freedom is a Choice

The 50/30/20 rule isn’t about math; it’s about values. It asks you to value your survival (Needs), your present happiness (Wants), and your future freedom (Savings) in a balanced way.

In the complex economic world of 2026, simplicity is your greatest competitive advantage. By adopting this three-bucket system, you stop being a victim of your bank statement and start being the architect of your life.