1. Introduction: Why Your Credit Score Matters More Than Ever

Improve credit score fast using legal and safe methods is one of the most important financial goals in 2026. Your credit score is not just a number — it’s your financial identity that affects loans, interest rates, and long-term wealth.

In today’s world, your credit score is not just a number — it’s your financial identity.

It determines:

- Whether you can get a loan

- What interest rate you’ll pay

- Whether you qualify for rent, insurance, or even jobs (in some countries)

A good credit score can save you lakhs or crores over your lifetime, while a poor one can trap you in high-interest debt.

The good news?

You can improve your credit score fast, legally, and safely — without scams, hacks, or shortcuts.

This guide explains every term, every rule, and every step — with real-life examples — so anyone, even a beginner, can follow.

2. What Is a Credit Score?

A credit score is a three-digit number that represents how likely you are to repay borrowed money.

Think of it like:

- A report card for your financial behavior

- A trust score for lenders

Example:

If two people apply for a loan:

- Person A has a credit score of 780

- Person B has a credit score of 520

The lender will:

- Trust Person A more

- Offer Person A a lower interest rate

- Possibly reject Person B or charge a very high rate

3. Types of Credit Scores (FICO vs VantageScore)

There isn’t just one credit score. The two main scoring models are:

✅ FICO Score

- Most widely used by banks

- Range: 300–850

- Created by Fair Isaac Corporation

✅ VantageScore

- Created by Experian, Equifax, and TransUnion

- Also ranges 300–850

- Used by some lenders and apps

💡 Most lenders rely on FICO, so that’s what we focus on.

4. Credit Score Ranges Explained

| Score Range | Category | Meaning |

|---|---|---|

| 800–850 | Excellent | Best rates, easy approvals |

| 740–799 | Very Good | Very strong profile |

| 670–739 | Good | Average borrower |

| 580–669 | Fair | Risky but acceptable |

| 300–579 | Poor | High risk, limited access |

Example:

If your score is 620, you might:

- Get approved for a loan

- But pay 2–5% higher interest

If your score is 760, you:

- Get approved easily

- Save thousands in interest

5. What Is a Credit Report?

A credit report is a detailed record of your financial behavior.

It contains:

- Personal information

- Account history

- Payment records

- Outstanding balances

- Credit limits

- Public records (bankruptcy, collections, etc.)

- Inquiries (who checked your credit)

Your credit score is calculated from your credit report.

Think of it this way:

- Credit report = full medical record

- Credit score = overall health score

6. The 5 Key Factors That Determine Your Credit Score

Your credit score is not random. It is calculated using five main factors, each with a specific weight.

Let’s explain each in detail.

🔸 1. Payment History (35%) — The Most Important Factor

Payment history shows whether you:

- Paid bills on time

- Missed payments

- Defaulted

- Had accounts sent to collections

This accounts for 35% of your score — the largest portion.

What counts as a late payment?

- 30 days late

- 60 days late

- 90+ days late

The later and more recent, the worse the impact.

Example:

You have:

- Credit card bill due on 5th

- You pay on 7th

If your lender reports after 30 days, it becomes a 30-day late payment and can drop your score 50–100 points.

💡 Even one late payment can stay on your report for 7 years.

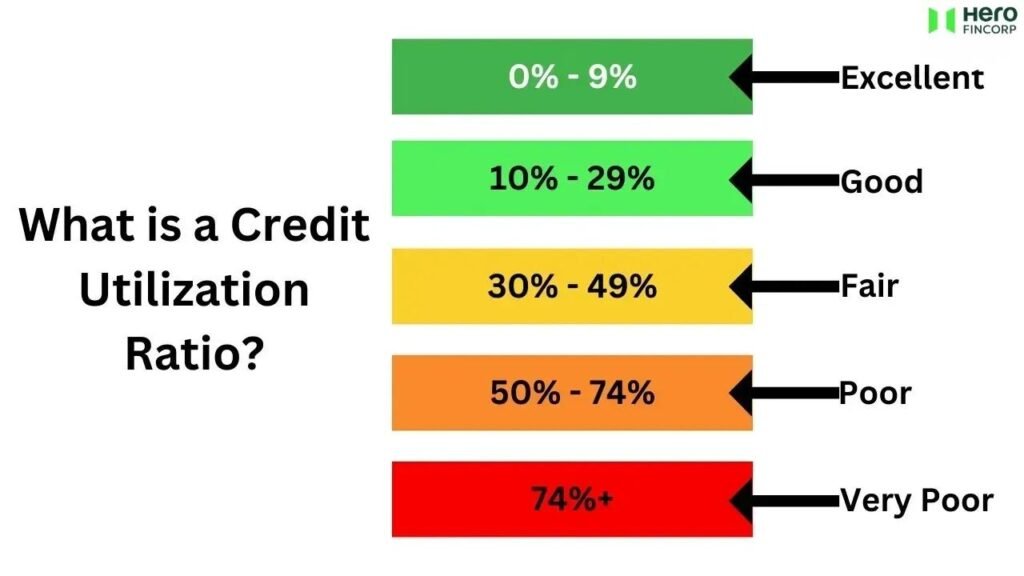

🔸 2. Credit Utilization (30%) — How Much Credit You Use

Credit utilization =

Credit used ÷ Total credit limit

It measures how much of your available credit you are using.

Example:

You have:

- Credit limit: ₹1,00,000

- Current balance: ₹60,000

Utilization = 60%

This is high and hurts your score.

💡 Ideal utilization = Below 30%, best = Below 10%

Below 10% = Excellent | 30% = Good | 50%+ = Risky | 80%+ = Poor

🔸 3. Length of Credit History (15%)

This measures:

- How long your accounts have been open

- Average age of all accounts

- Age of your oldest account

Older history = more trust.

Example:

- Person A: Credit history of 10 years

- Person B: Credit history of 1 year

Even if both behave well, Person A will usually have a higher score.

🔸 4. Credit Mix (10%)

Credit mix refers to having different types of credit, such as:

- Credit cards (revolving credit)

- Personal loans (installment loans)

- Auto loans

- Home loans

A healthy mix shows you can manage different forms of debt responsibly.

🔸 5. New Credit & Hard Inquiries (10%)

Whenever you apply for credit, the lender performs a hard inquiry, which:

- Slightly lowers your score

- Stays on your report for 2 years

Too many inquiries in a short time makes you look desperate for credit.

Example:

Applying for 5 credit cards in one month can drop your score significantly.

🔹 7. How Credit Scores Affect Your Life

Your credit score impacts:

🏦 Loans & Mortgages

- Approval or rejection

- Interest rate

- Loan amount

🏠 Renting a Home

- Landlords check your credit

- Poor score may mean rejection or higher deposit

🚗 Auto Insurance

- Some insurers use credit-based scores

- Lower score = higher premiums

💼 Jobs

- Some employers check credit for finance roles

📱 Mobile Plans

- Postpaid plans may require credit checks

8. How Fast Can You Improve Your Credit Score?

30 Days (20–100 pts), 90 Days (50–150 pts), 1 Year (100–250 pts)

Credit improvement depends on:

- Your current score

- Your credit profile

- Your actions

Typical improvement timelines:

- 30–45 days: Small improvements (10–50 points)

- 3–6 months: Noticeable improvement (50–100 points)

- 6–12 months: Major improvement (100–200+ points)

There is no legal overnight fix, but there are fast and safe methods.

9. Step-by-Step Plan to Improve Your Credit Score Fast

Now let’s move into action mode.

✅ Step 1: Get Your Credit Report (Free)

You must know where you stand.

Get your report from:

- Official credit bureaus

- Government-approved websites

- Banks or apps offering free scores

Review:

- Accounts

- Balances

- Payment history

- Errors

✅ Step 2: Check for Errors and Dispute Them

Errors are common and can destroy your score unfairly.

Common errors:

- Accounts that are not yours

- Incorrect balances

- Late payments that you paid on time

- Duplicate accounts

- Closed accounts showing as open

Example:

Your report shows a ₹50,000 loan you never took.

That error alone can drop your score 80–150 points.

You must:

- File a dispute with the bureau

- Attach proof

- Follow up

Once corrected, your score can rise quickly.

✅ Step 3: Pay All Bills On Time (100% of the Time)

This is non-negotiable.

Set:

- Auto-pay

- Reminders

- Calendar alerts

Even one missed payment can undo months of progress.

✅ Step 4: Reduce Credit Card Balances (Utilization Hack)

This is one of the fastest ways to improve your score.

Strategy:

- Pay down cards to below 30%

- Best: below 10%

Example:

Card limit: ₹1,00,000

Balance: ₹80,000 (80% utilization)

Pay down to ₹10,000 → utilization = 10%

Your score can increase 30–100 points.

✅ Step 5: Don’t Close Old Credit Cards

Closing old accounts:

- Reduces your available credit

- Shortens your credit history

- Increases utilization

Unless there’s a fee, keep them open.

✅ Step 6: Avoid New Credit Applications Temporarily

Stop applying for:

- New credit cards

- Personal loans

- BNPL (Buy Now Pay Later)

Give your score time to recover.

✅ Step 7: Use the Debt Snowball or Avalanche Method

Let’s explain both.

🔹 Debt Snowball Method

Pay off:

- Smallest balance first

- Then move to next

Best for motivation.

🔹 Debt Avalanche Method

Pay off:

- Highest interest rate first

Best for saving money.

Both help your score by:

- Reducing balances

- Improving payment history

10. How to Fix Errors on Your Credit Report (Detailed Guide)

Step-by-Step Dispute Process:

- Identify the error.

- Collect proof (bank statements, receipts, contracts).

- Submit dispute online or by mail.

- Credit bureau investigates (usually 30 days).

- If verified wrong, it is corrected or removed.

Example:

Your report shows:

- A late payment in May

But you have bank proof showing you paid on time.

Once corrected, your score increases automatically.

11. How to Pay Down Debt Strategically

Debt is the biggest enemy of your credit score.

Let’s explain the best strategies.

🔸 Balance Transfer (If Available)

Move high-interest debt to:

- A card with 0% interest for 6–18 months

This:

- Reduces interest

- Helps you pay faster

- Improves utilization

🔸 Consolidation Loan

Combine:

- Multiple debts into one loan

This:

- Simplifies payments

- Can reduce interest

- Improves credit mix

🔸 Negotiation & Settlement

If you’re in default:

- Negotiate with lenders

- Ask for:

- Reduced balance

- Payment plans

- Removal of negative marks

⚠️ Be careful: Some settlements hurt your score temporarily but may be necessary.

12. How to Lower Credit Utilization Quickly

Fastest legal methods:

1. Pay before the statement date

Not just the due date.

2. Make multiple payments per month

This keeps balances low.

3. Request a credit limit increase

If your income improved and history is clean.

Example:

Limit = ₹1,00,000

Balance = ₹40,000 → 40% utilization

Limit increased to ₹2,00,000

Same balance = 20% utilization → score improves

13. How to Build Credit from Scratch

If you have no credit history, lenders don’t know if they can trust you.

Here’s how to build credit safely:

🔸 Secured Credit Card

You deposit money → that becomes your limit.

Example:

Deposit ₹10,000 → limit ₹10,000

Use it responsibly → your credit history starts.

🔸 Credit Builder Loan

You borrow a small amount that is locked.

You repay monthly.

After completion, you get the money back.

This builds:

- Payment history

- Credit mix

🔸 Become an Authorized User

Get added to someone’s:

- Old, well-managed credit card

You inherit:

- Their history

- Their good behavior

⚠️ Only if the primary user is responsible.

14. How to Rebuild Credit After Bad Credit

Bad credit can result from:

- Missed payments

- Defaults

- Collections

- Bankruptcy

Rebuilding is possible — and legal.

Step 1: Stop the bleeding

No more late payments.

Step 2: Clear or settle bad debts

Options:

- Pay in full

- Settle for less

- Negotiate “pay for delete” (not guaranteed)

Step 3: Start positive credit

Use:

- Secured cards

- Credit builder loans

Step 4: Be consistent for 6–12 months

Credit improves gradually.

15. The Truth About Credit Repair Companies

Credit repair companies:

- Cannot remove accurate negative information

- Cannot legally “fix” your credit overnight

- Often charge high fees for tasks you can do yourself

⚠️ If someone promises:

- “Guaranteed 800 score”

- “Remove all negatives instantly”

→ It’s a scam.

16. Myths About Credit Scores

Let’s destroy common myths.

❌ Myth 1: Checking your score hurts it

✅ Truth: Checking your own score = soft inquiry = no impact

❌ Myth 2: Carrying a balance improves your score

✅ Truth: Paying in full is better

❌ Myth 3: Closing cards improves your score

✅ Truth: It often lowers your score

❌ Myth 4: Income affects your score

✅ Truth: Income is not part of the score formula

17. Legal Rights Under Credit Laws

You are protected by law.

Your Rights:

- Right to access your credit report

- Right to dispute errors

- Right to correction within a reasonable time

- Right to fair reporting

- Right to privacy

Credit bureaus must:

- Investigate disputes

- Correct errors

- Remove unverifiable information

18. Real-Life Examples and Case Studies

🧑 Case Study 1: Rahul (Score 520 → 720 in 9 Months)

Problem:

- Missed payments

- High balances

- Errors on report

Actions:

- Disputed 3 errors

- Paid cards down to 10% utilization

- Set up auto-pay

- Stopped applying for credit

Result:

- +200 points in 9 months

👩 Case Study 2: Priya (No Credit → 700 in 6 Months)

Problem:

- No credit history

Actions:

- Opened secured card

- Used 5–10% utilization

- Paid in full every month

Result:

- Built strong score in 6 months

👨 Case Study 3: Amit (Default → Recovery)

Problem:

- Loan default

- Collections

- Very poor score

Actions:

- Settled old debts

- Opened credit builder loan

- Maintained perfect payment history

Result:

- Rebuilt score within 12 months

19. Tools, Apps, and Resources

You can use:

- Credit monitoring apps

- Bank dashboards

- Budgeting apps

- Debt calculators

- Payment reminders

These tools help:

- Track score

- Monitor changes

- Prevent mistakes

20. Frequently Asked Questions (FAQ)

Q1. How long do late payments stay on my report?

Late payments remain for 7 years, but their impact reduces over time.

Q2. Can I remove accurate negative information?

No. Only incorrect or unverifiable information can be removed legally.

Q3. Is paying off collections good for my score?

Yes, especially if it updates to “paid collection” or is removed.

Q4. Does paying off a loan early hurt my score?

No. It’s usually positive long-term.

Q5. How many credit cards should I have?

There is no perfect number. 2–4 well-managed cards are often ideal.

21. Trusted Financial Resources

- Budgeting strategies recommended by the Federal Reserve highlight the importance of savings habits.

- Tax planning insights from the Internal Revenue Service can help reduce liabilities.

- Long-term investing through firms like Vanguard Group supports wealth creation.

According to the Federal Reserve, most households struggle with emergency savings.

22. Final Action Plan & Summary

Let’s summarize your legal and safe path to a higher credit score:

✔ Do This:

- Check your credit report

- Dispute errors

- Pay all bills on time

- Reduce balances below 30% (best below 10%)

- Keep old accounts open

- Avoid unnecessary new credit

- Build positive history consistently

❌ Avoid This:

- Late payments

- High utilization

- Credit repair scams

- Closing old accounts

- Frequent applications

🎯 Final Thought

Improving your credit score is not about tricks — it’s about:

- Discipline

- Consistency

- Understanding the system

The system rewards:

- Responsible behavior

- Long-term reliability

- Smart financial habits

If you follow the steps in this guide, you will see improvement — safely, legally, and permanently.