Introduction: Why Credit Cards Matter

Credit cards explained simply: they are powerful financial tools that can either build your wealth or trap you in high-interest debt. In 2026, understanding how to use credit cards without going into debt is essential for financial success.

In Tier-1 countries like the USA, UK, Canada, and Australia, and rapidly developing economies like India, credit cards have become essential. They are the primary engine behind your Credit Score, which dictates your ability to buy a home or rent an apartment.

This guide on credit cards explained will help you understand how banks make money, how interest works, and how to use credit cards safely without ever falling into debt.

The Strategic Value

Credit cards provide a level of Consumer Protection that cash and debit cards simply cannot match. If a merchant goes bankrupt after you buy a flight, or if a fraudster steals your card details, the bank’s money is at stake, not yours. This “buffer” is the most underrated advantage of credit cards.

Credit Cards Explained: What Is a Credit Card?

A credit card is a physical or digital card representing a revolving line of credit. It is essentially a pre-approved, short-term loan that you can dip into at any time.

- Revolving means that as you pay back what you borrowed, that amount becomes available to spend again.

- Non-Revolving (like a car loan) means once you pay it back, the account is closed.

Example:

Imagine you have a ₹1,00,000 credit limit. You buy a new laptop for ₹40,000. Your available credit is now ₹60,000. Once you pay that ₹40,000 back to the bank, your available credit “revolves” back up to ₹1,00,000.

How Credit Cards Work (Credit Cards Explained Simply) : The Lifecycle of a Transaction

Understanding the mechanics helps you see where the bank makes its money—and how you can avoid giving them yours.

- The Swipe: You use your card at a store.

- Authorization: The merchant asks the bank, “Does this person have enough credit?”

- The Loan: The bank pays the merchant immediately. You now owe the bank.

- The Statement: Once a month, the bank sends a summary of all your “loans” from the last 30 days.

- The Settlement: You have a specific window (the Grace Period) to pay the bank back. If you pay 100%, you pay $0 in interest.

Key Credit Card Terms Explained in Detail

To master the game, you must speak the language. Misunderstanding these terms is the #1 cause of credit card debt.

🔹 Credit Limit (The Ceiling)

This is the maximum amount the bank is willing to risk on you. It is based on your income and your history of paying people back.

- Pro Tip: Having a high limit but using very little of it (low utilization) is the fastest way to boost your credit score.

🔹 Statement Balance vs. Current Balance

This is where most beginners get confused.

- Statement Balance: The total amount you owed on the day the “bill” was printed. This is the number you must pay to avoid interest.

- Current Balance: Everything you owe up to this very second, including purchases made after the statement was printed.

- Example: Your statement on Jan 1st is $500. On Jan 2nd, you buy groceries for $50. Your Statement Balance is still $500, but your Current Balance is $550. You only need to pay $500 to stay interest-free.

🔹 The Minimum Payment (The Trap)

The bank will tell you that you only “need” to pay a small amount (usually 2-5%) to avoid a late fee. This is a trick.

- If you owe $1,000 at 24% APR and only pay the $25 minimum, you will be paying off that debt for nearly 20 years and will pay thousands in interest.

🔹 APR (Annual Percentage Rate)

The cost of borrowing money over a year. However, interest is usually calculated daily.

$$\text{Daily Rate} = \frac{\text{APR}}{365}$$

If your APR is 36%, your daily rate is 0.098%. If you carry a $1,000 balance, you are being charged roughly $1 per day in interest.

Types of Credit Cards: Finding Your Fit

🟦 Secured Credit Cards (The Rebuilder)

You give the bank a deposit (e.g., $500), and they give you a card with a $500 limit. They hold your money as collateral. This is perfect for people with bad credit or no credit history.

🟩 Rewards & Cash Back Cards (The Optimizer)

These cards “pay” you to use them.

- Cash Back: You get a percentage (1% to 5%) of your spend back as a statement credit.

- Travel Miles: You earn points that can be transferred to airlines for “free” flights.

🟥 Student Cards

Lower barriers to entry, designed for those with little income. They often have lower limits to prevent students from getting into deep trouble.

The “Interest Math”: Why Carrying a Balance is Financial Suicide

The Federal Reserve reports that average credit card interest rates often exceed 20%, making unpaid balances extremely expensive. Most people don’t realize that credit card interest compounds daily. This means you pay interest on the interest you were charged yesterday.

The Math Example:

You have a $5,000 balance at 25% APR.

- Month 1 Interest: ~$104

- If you don’t pay it, Month 2 interest is calculated on $5,104.

- Within a few years, your debt can double even if you never buy another thing.

The Grace Period: The Secret to Free Borrowing

The Grace Period is the time between the end of your billing cycle and your due date (usually 21–25 days).

- If you pay your Statement Balance in full, the bank charges you 0% interest.

- This effectively means you are using the bank’s money for free for up to 50 days.

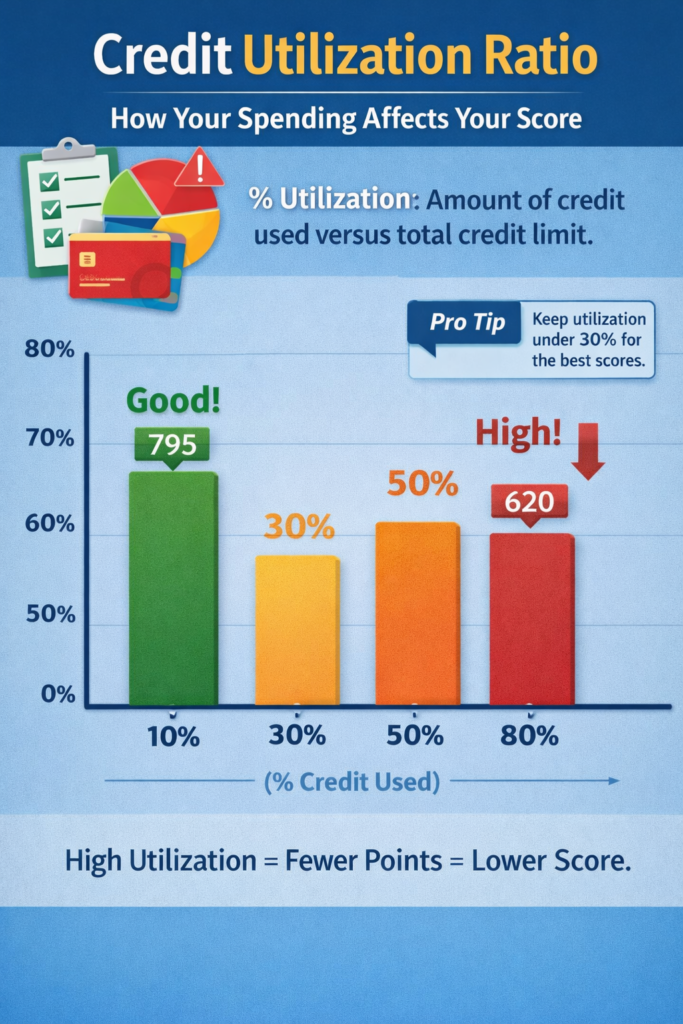

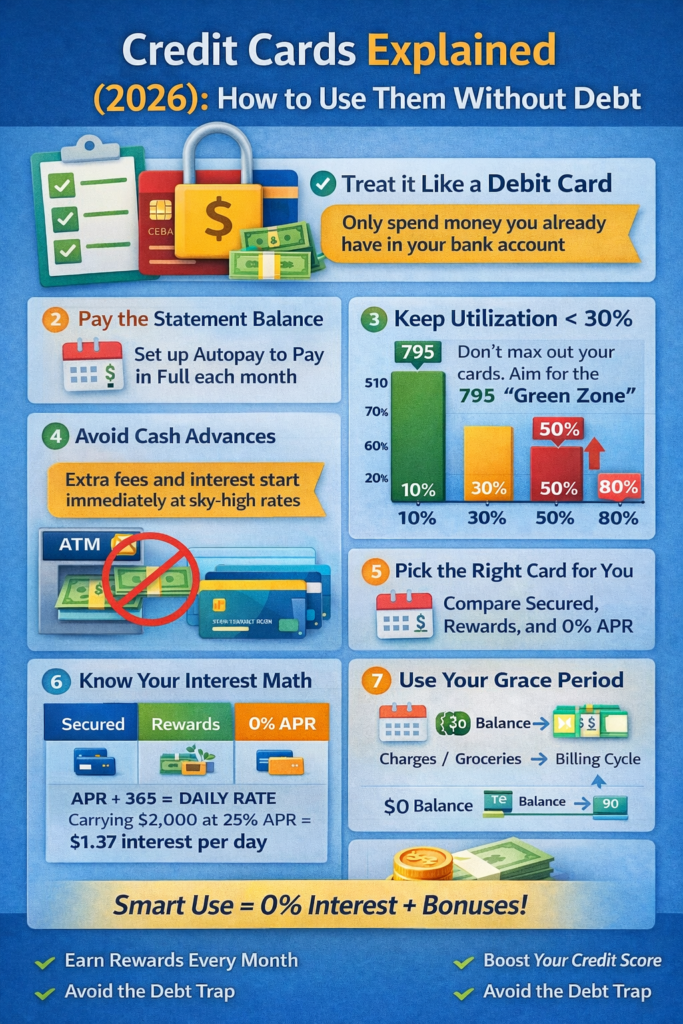

Credit Utilization Ratio (CUR): The 30% Rule

Credit bureaus like Experian recommend keeping your utilization below 30% for a healthy credit profile. Your CUR is 30% of your total credit score. It is the ratio of how much you owe vs. how much you could borrow.

$$\text{CUR} = \left( \frac{\text{Total Balances}}{\text{Total Limits}} \right) \times 100$$

- Example: You have a $10,000 limit. If you owe $3,000, your CUR is 30%.

- Rule of Thumb: Keep this under 10% for a “God-tier” credit score.

How Credit Cards Affect Your Credit Score

According to the Consumer Financial Protection Bureau, payment history and credit utilization are the most important factors affecting your credit score. Your score is calculated based on five factors:

- Payment History (35%): Did you pay on time?

- Utilization (30%): How much of your limit are you using?

- Length of History (15%): How old are your accounts?

- Credit Mix (10%): Do you have cards and loans?

- New Credit (10%): Have you applied for too many cards lately?

How to Use Credit Cards Without Going into Debt (Step-by-Step Guide)

The “Debit Card” Rule

Only buy something on a credit card if the money is already in your bank account. If you can’t pay for it with your debit card right now, you can’t afford it on your credit card.

Strategic Steps:

- Set Up Autopay: Set it to pay the “Full Statement Balance” every month.

- Check Daily: Use your bank’s app to monitor spending every morning. This prevents “Bill Shock” at the end of the month.

- Avoid Cash Advances: Using a credit card at an ATM is a disaster. Interest starts immediately (no grace period) and the rates are often 10% higher than regular purchases.

Step-by-Step Strategy for Beginners

- Month 1-3: Use the card for one small recurring bill (like Netflix). Pay it off in full. This builds a “Clean” payment history.

- Month 4-6: Start using it for Groceries and Fuel. These are “Need” spends, not “Want” spends.

- The “Freeze” Rule: If you ever fail to pay the full balance, stop using the card immediately until the balance is $0. You have lost your grace period and are now being charged interest on every new coffee you buy.

Common Credit Card Mistakes to Avoid

- ❌ Maxing out the card: Even if you pay it off, a 100% utilization rate on the day the bank “reports” will temporarily tank your credit score.

- ❌ Closing old cards: Closing your oldest card shortens your credit history and can drop your score. If there’s no annual fee, keep it open and buy a pack of gum once a year to keep it active.

- ❌ Ignoring the “Fine Print”: Many cards have foreign transaction fees (3%). If you travel, you need a card that waives these.

- This guide on credit cards explained helps you understand how banks calculate interest and how to avoid it completely.

- When credit cards are explained properly, it becomes clear that the biggest risk is not spending—but interest.

How to Pay Off Credit Card Debt

If you are already in the “Debt Trap,” use one of these two battle-tested methods:

🔹 The Avalanche Method (Mathematical)

List debts by Interest Rate. Pay the minimum on everything, but throw every spare penny at the card with the highest APR.

- Pros: Saves the most money.

- Cons: Takes time to feel like you’ve “won.”

🔹 The Snowball Method (Psychological)

List debts by Balance Size. Pay off the smallest balance first.

- Pros: The “Quick Win” keeps you motivated.

- Cons: You pay slightly more in interest over time.

Credit Card Rewards: The “Pro” Game

Rewards are the bank’s way of trying to get you to spend more. However, if you are a “Transactor” (someone who pays in full), rewards are pure profit.

Cash Back vs. Points vs. Miles

- Cash Back: Best for beginners. 2% back on everything is a 2% “discount” on your life.

- Travel Miles: Best for high spenders. Transferring 50,000 points to an airline for a $2,000 Business Class flight gives you 4 cents per point in value—far better than 1% cash back.

Balance Transfers and 0% APR Offers

A Balance Transfer is moving debt from a high-interest card to a new card with 0% interest for 12–21 months.

- Example: You have $5,000 debt at 25%. You move it to a 0% card. Even with a 3% transfer fee ($150), you save over $1,000 in interest over the next year.

- The Danger: If you haven’t fixed your spending habits, you will just end up with two maxed-out cards.

Credit Cards vs. Debit Cards: The Security Battle

In 2026, using a debit card for online shopping is risky.

- Debit: If someone steals your numbers, your actual rent money disappears. It can take weeks to get it back.

- Credit: If someone steals your numbers, the bank’s money is gone. You report it, the charge is frozen, and you are never out of pocket.

Myths About Credit Cards

- Myth: Carrying a balance helps your score. Fact: This is a lie designed by banks to make interest. Paying in full is always better.

- Myth: You have to be rich to have a “Black” or “Gold” card. Fact: Credit is about reliability, not just wealth. A teacher with a 800 score can get a better card than a millionaire with a 500 score.

Safety and Fraud Protection

- Virtual Cards: Many apps now let you create a “one-time use” card number for sketchy websites.

- Biometric Locks: Always enable “FaceID” or “Fingerprint” for your banking app.

- The “CVV” Rule: Never share your CVV or OTP (One-Time Password) with anyone, even if they claim to be from the bank. Banks will never ask for your OTP.

Frequently Asked Questions (FAQs)

Q: Does checking my own credit score hurt it?

A: No. That is a “Soft Inquiry.” Only when a lender checks it for a loan application is it a “Hard Inquiry” that affects your score.

Q: Can I negotiate my interest rate?

A: Yes. If you have been a customer for over a year and have a good payment history, call the bank and say, “I’m considering a balance transfer to another bank with a lower rate. Can you lower my APR?” Often, they will drop it by 3–5%.

Q: Does carrying a balance on a credit card improve your credit score?

A: No. Carrying a balance does not improve your credit score and only causes you to pay unnecessary interest. Paying your full statement balance every month is the best strategy.

Q: What is the safest way to use a credit card?

A: The safest way to use a credit card is to treat it like a debit card, only spend money you already have, and set autopay for the full statement balance every month.

Final Summary and Best Practices

A credit card is a tool, like a hammer. You can use it to build a house (wealth) or smash your thumb (debt).

The “Elite Investor” Checklist:

- Pay in Full: Every month, without fail.

- Stay Under 10%: Never “Max out” the card.

- Automate: Take the “Human Error” out of the equation.

- Audit: Spend 10 minutes every Sunday reviewing your transactions.

Now that you have credit cards explained in detail, you can use them as a tool instead of a trap. This complete guide on credit cards explained gives you everything you need to use credit cards without going into debt and build long-term financial success.

🎯 Final Thought

Control your money, or it will control you. If you treat a credit card like a financial weapon for building wealth, you will eventually reach a point where your rewards pay for your vacations and your credit score opens every door you knock on.How Inflation Destroys Savings (2026 Survival Guide to Beat Inflation)How to Save $10,000 a Year Without Sacrificing Your Lifestyle (2026 Guide)Improve Credit Score Fast (Legally & Safely) – 2026 Ultimate Guide