Introduction: The Most Important Investing Decision You’ll Ever Make

Asset allocation is the most important concept in investing because it determines how your money grows, how much risk you take, and how stable your portfolio remains over time.

If you remember only one concept in investing, remember this:

Asset allocation matters more than stock picking, market timing, or chasing trends.

Most beginners think investing success comes from finding the next big company like Tesla Inc. or perfectly timing the market. However, this belief is misleading because even professional investors fail to consistently predict markets.

In reality, what determines long-term success is how you divide your money, not what individual stock you pick. Your portfolio structure controls both returns and risk, which are the two most important factors in investing.

For investors in Tier-1 countries like the United States, United Kingdom, Canada, and Australia, asset allocation becomes even more critical due to access to global markets, tax systems, and retirement plans.

If you’re new to investing, this quick video explains asset allocation in a simple and visual way. It will help you understand how different assets like stocks and bonds work together in a portfolio before diving deeper into the detailed explanation below.

As explained in the video, asset allocation is not about picking the best individual investment but about balancing different asset classes to manage risk and maximize returns. This concept is widely used by investors in developed markets to build long-term wealth while avoiding major losses during market downturns.

What Is Asset Allocation? (Simple Definition Explained)

What Is an Asset?

An asset is anything that has value and can either grow in value or generate income over time. In finance, assets are the building blocks of wealth.

Examples include:

- Stocks (ownership in companies)

- Bonds (loans to governments/companies)

- Real estate (property investments)

- Gold (store of value)

- Cash (liquid money)

Each asset behaves differently under economic conditions. For example, stocks grow during economic expansion, while bonds provide stability during downturns.

What Does Allocation Mean?

Allocation means how you distribute something across different options. In investing, it refers to dividing your money across various asset classes.

For example:

- 60% stocks

- 30% bonds

- 10% cash

This distribution determines your overall risk exposure and return potential.

Full Definition of Asset Allocation

Asset Allocation = The strategic distribution of your investment capital across different asset classes to balance risk and return.

This means:

- You don’t put all money in one place

- You spread investments intelligently

- You adjust based on goals, age, and risk tolerance

What Are Asset Classes in Asset Allocation?

Asset classes are categories of investments that behave similarly.

📈 1. Stocks (Equities)

Stocks represent ownership in companies like Apple Inc. or Microsoft Corporation.

Stocks can deliver around 8–10% average annual returns in developed markets like the United States, but they can also decline by 30–50% during major market crashes. This volatility is why proper asset allocation is essential to balance risk and return in a long-term investment strategy.

How You Make Money:

- Capital appreciation (price increases over time)

- Dividends (regular income payouts)

Characteristics:

- High return potential (8–10% long-term average in the U.S.)

- High volatility (prices fluctuate frequently)

- Best for long-term wealth creation

Stocks are essential for growth but require patience during market crashes.

🏦 2. Bonds (Fixed Income)

Bonds are loans you give to governments or corporations, such as those issued by the United States Department of the Treasury.

Bonds typically generate 3–5% annual returns and provide stable income through interest payments. In economies like the United Kingdom, bonds are widely used to reduce portfolio volatility and protect capital during stock market downturns.

How You Make Money:

- Interest payments (fixed income)

- Return of principal at maturity

Characteristics:

- Lower risk than stocks

- Lower returns (3–5%)

- Provide stability in downturns

Bonds act as a cushion during stock market crashes.

🏠 3. Real Estate Investments

Real estate includes physical property or REITs (Real Estate Investment Trusts).

Income Sources:

- Rental income

- Property appreciation

- Tax benefits (especially in Tier-1 countries)

Real estate is a strong inflation hedge and adds diversification.

🪙 4. Commodities (Gold, Oil)

Commodities include natural resources like gold and oil.

Role in Portfolio:

- Protect against inflation

- Perform well during crises

- Reduce overall portfolio risk

Gold is especially used during economic uncertainty.

💵 5. Cash & Cash Equivalents

Includes:

- Savings accounts

- Treasury bills

- Money market funds

Purpose:

- Liquidity (easy access to money)

- Emergency funds

- Stability

However, cash loses value due to inflation over time.

A well-structured asset allocation strategy depends on how these asset classes work together. To understand this concept in more detail, read our complete guide on building a diversified portfolio and how combining stocks, bonds, and real estate can reduce overall risk while improving long-term returns.

Asset Classes Comparison Table

| Asset Class | What It Means | Risk Level | Return Potential | Income Type | Volatility | Best For | Example |

|---|---|---|---|---|---|---|---|

| 📈 Stocks (Equities) | Ownership in a company that grows over time | High | High (8–10% long-term) | Dividends + Capital Gain | High | Long-term wealth growth | Apple Inc. |

| 🏦 Bonds (Fixed Income) | Loan given to government or company | Medium | Moderate (3–5%) | Fixed Interest | Low–Medium | Stability & income | United States Department of the Treasury |

| 🏠 Real Estate | Property or REIT investment | Medium | Moderate–High | Rental Income | Medium | Passive income & inflation hedge | Residential/Commercial property |

| 🪙 Commodities | Physical assets like gold, oil | Medium | Variable | Price appreciation | Medium–High | Inflation protection | Gold, Oil |

| 💵 Cash & Equivalents | Liquid money or short-term instruments | Low | Low (1–3%) | Interest | Very Low | Safety & liquidity | Savings account |

This comparison table helps investors clearly understand how different asset classes function within an asset allocation strategy.

Stocks offer the highest growth potential but come with significant volatility, making them suitable for long-term investors in markets like the United States or United Kingdom.

Bonds, on the other hand, provide stability and predictable income, which helps reduce overall portfolio risk.

Real estate and commodities act as diversification tools, especially during inflationary periods, while cash ensures liquidity and financial safety. A well-balanced asset allocation combines these asset classes strategically to optimize returns while minimizing risk.

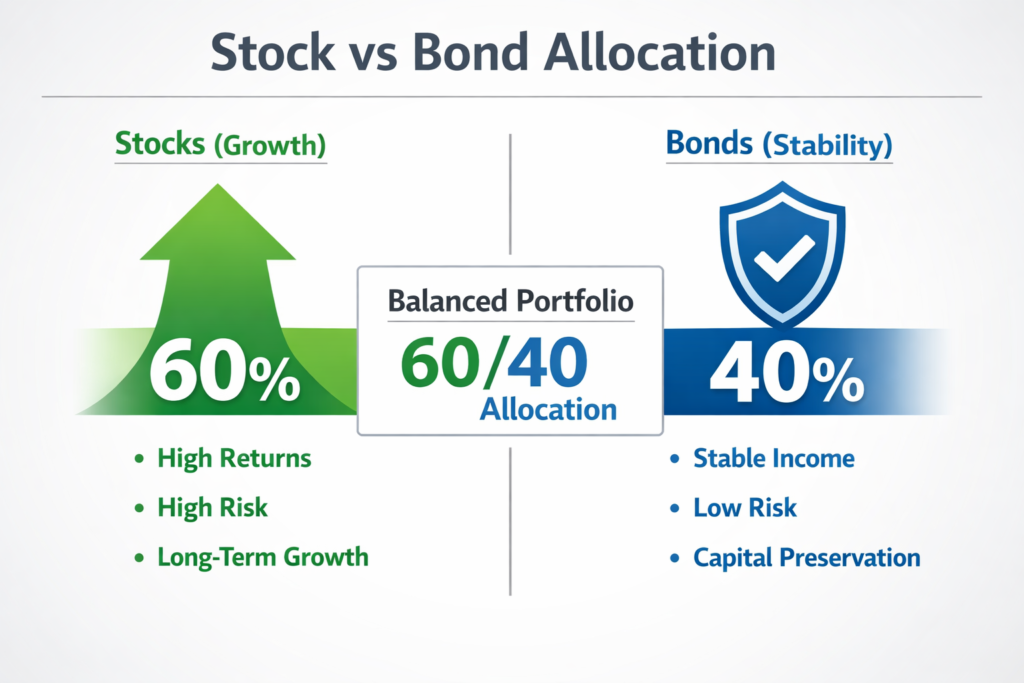

Stock vs bond allocation is one of the most critical components of asset allocation because it directly determines a portfolio’s risk and return profile.

Stocks provide higher long-term growth potential but come with greater volatility, while bonds offer stability and predictable income with lower risk.

In Tier-1 countries like the United States and United Kingdom, a balanced allocation such as 60% stocks and 40% bonds is widely used to achieve steady growth while protecting against market downturns.

This balance helps investors stay invested during volatility and achieve consistent long-term returns.

Why Asset Allocation Determines 90% of Investment Returns

According to Investopedia, asset allocation is one of the most important factors in determining portfolio performance. Regulatory bodies like the U.S. Securities and Exchange Commission also emphasize diversification to reduce risk.

This concept comes from research by:

- Gary P. Brinson

- Randolph Hood

- Gilbert Beebower

They found that:

Over 90% of portfolio performance variation is due to asset allocation.

This does NOT mean stock selection is useless. It means:

- Allocation determines overall direction

- Stock picking only fine-tunes results

Asset Allocation Examples (Real Case Studies)

Case Study 1: Two Investors

Investor A

- 90% stocks

- 10% bonds

Investor B

- 50% stocks

- 50% bonds

ssume:

- Stocks return 10%

- Bonds return 4%

Yearly Returns:

Investor A:

(0.9 × 10%) + (0.1 × 4%) = 9.4%

Investor B:

(0.5 × 10%) + (0.5 × 4%) = 7%

Returns Calculation

| Investor | Annual Return |

|---|---|

| A | 9.4% |

| B | 7% |

30-Year Growth (Starting $100,000)

| Investor | Final Value |

|---|---|

| A | $1.5 Million |

| B | $761,000 |

👉 Same assets, different allocation → huge difference.

Asset Allocation Growth Comparison

| Allocation | Risk | Return | Stability |

|---|---|---|---|

| 90% Stocks | High | High | Low |

| 60/40 | Medium | Medium | High |

| 30% Stocks | Low | Low | Very High |

This table highlights how asset allocation directly impacts risk, return, and stability.

A portfolio heavily weighted toward stocks offers higher growth potential but comes with increased volatility, while a more balanced allocation like 60/40 provides a better mix of growth and protection.

Conservative portfolios reduce risk significantly but may limit long-term returns, which is why choosing the right asset allocation strategy is essential for achieving financial goals.

The chart illustrates how asset allocation directly impacts investment behavior.

A stock-heavy portfolio (90%) offers higher potential returns but comes with increased risk and lower stability.

A balanced 60/40 portfolio provides moderate risk and return with improved stability, making it a popular long-term strategy.

Meanwhile, a conservative 30% stock allocation prioritizes capital preservation and stability, but with lower growth potential.

Case Study 2: Market Crash (2008 Example)

During the 2008 crisis:

- Stock market dropped ~37%

- Bonds remained stable

Imagine:

Investor A: 100% stocks

Investor B: 60% stocks / 40% bonds

Investor A loses 37%

Investor B loses ~20%

Who recovers faster?

Investor B.

Because smaller losses require smaller gains to recover.

Math:

- 50% loss needs 100% gain

- 20% loss needs 25% gain

Risk control matters more than maximizing returns.

| Portfolio | Loss |

|---|---|

| 100% Stocks | -37% |

| 60/40 Portfolio | -20% |

👉 Smaller losses = faster recovery.

The Mathematics of Asset Allocation

Portfolio Return Formula

Formula:

Portfolio Return = (Weight × Return) of each asset

Rp = (W1 × R1) + (W2 × R2) + (W3 × R3)…

Where:

- Rp = Portfolio return

- W = Weight (allocation %)

- R = Asset return

But volatility is more complex.

Example:

- 60% stocks (10%)

- 40% bonds (4%)

Return = 7.6%

Risk Concept

Risk depends on:

- Standard deviation (Volatility)

- Correlation between assets

Low correlation assets reduce total risk.

This is Modern Portfolio Theory developed by: Harry Markowitz

He won a Nobel Prize for proving diversification mathematically reduces risk. i.e. Developed by Harry Markowitz under Modern Portfolio Theory.

Types of Asset Allocation

Strategic Asset Allocation

Fixed long-term allocation. Stable and disciplined.

Tactical Asset Allocation

Short-term adjustments based on market conditions.

Dynamic Allocation

Continuously changing allocation. Used by professionals.

Age-Based Allocation

“100 – age” rule. Simple but not always accurate.

As shown in the asset allocation strategy diversification chart above, each strategy—strategic, tactical, dynamic, and age-based—plays a unique role in balancing risk and maximizing long-term returns.

Asset allocation strategy diversification chart visually explains how different approaches like strategic, tactical, dynamic, and age-based allocation help investors balance risk and return. Each strategy represents a different way of adjusting your portfolio based on time horizon, market conditions, and personal goals. Strategic allocation, as seen in the diversification chart above, focuses on long-term stability.

For example, strategic allocation focuses on long-term stability, while tactical allocation allows short-term adjustments based on market opportunities. This diversification across strategies ensures that investors are not dependent on a single approach, making their portfolio more resilient during market volatility.

9️⃣ Target-Date Funds

Managed by firms like:

- Vanguard Group

- Fidelity Investments

They automatically adjust allocation over time:

- Young → More stocks

- Old → More bonds

Model Portfolios Based on Risk Level

🟢 Aggressive Portfolio (High Risk)

- 90% stocks

- 10% bonds

🟡 Balanced Portfolio

- 60% stocks

- 40% bonds

🔵 Conservative Portfolio

- 30% stocks

- 60% bonds

- 10% cash

If you want to explore how different investment options fit into these portfolios, you can also read our detailed comparison of stocks, ETFs, and mutual funds to understand which assets are best for your financial goals.

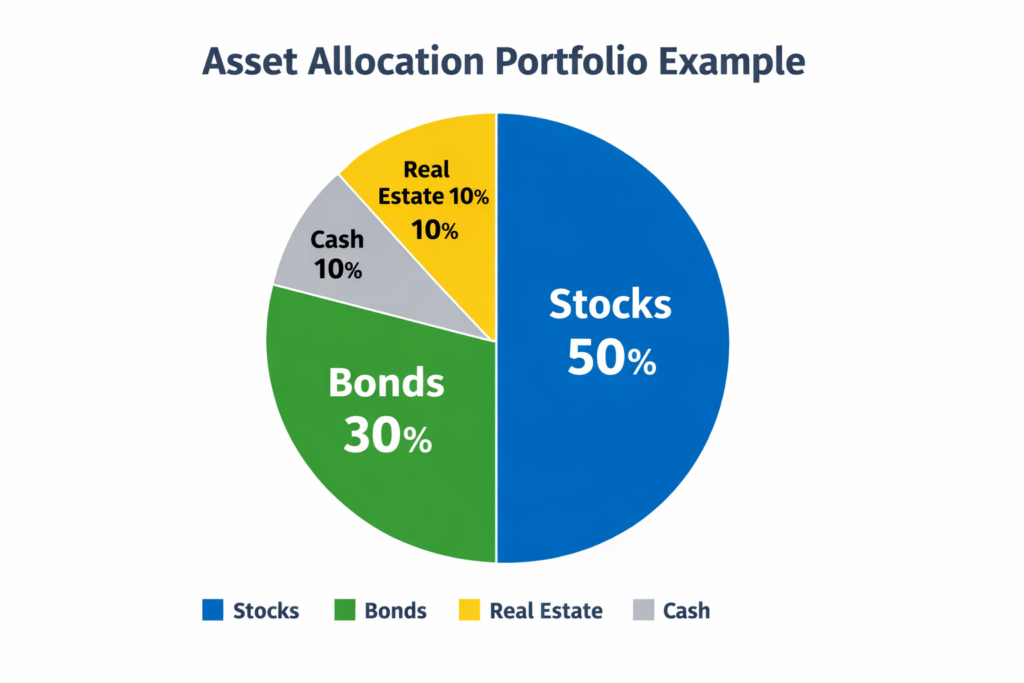

Pie Chart Representation (Example Balanced Portfolio)

Below is a real-world asset allocation portfolio example used by long-term investors.

The above asset allocation pie chart example visually represents how a diversified portfolio is structured to balance risk and return.

In this example, a significant portion of the portfolio is allocated to stocks, which provide long-term growth potential, while bonds offer stability and reduce volatility. Real estate adds an additional layer of diversification and income generation, and cash ensures liquidity for short-term needs and emergencies.

This type of asset allocation strategy is commonly used by investors in the United States, United Kingdom, and Canada to achieve a balanced investment approach that can perform well across different market conditions.

Why Investors Fail at Asset Allocation

Common mistakes:

- Emotional decisions

- Buying high, selling low

- No rebalancing

- Overconfidence

Behavior is the biggest risk.

Rebalancing: The Key to Maintaining Portfolio Performance

What Is Rebalancing?

Rebalancing means restoring original allocation.

Example:

- Stocks grow to 75%

- Sell stocks, buy bonds

Benefits of Rebalancing:

- Maintains risk

- Locks profits

- Encourages discipline

Psychological Power

Good allocation:

- Reduces stress

- Prevents panic selling

- Improves consistency

The best portfolio is one you can hold during crashes.

Correlation

Correlation = how assets move together.

| Value | Meaning |

|---|---|

| +1 | Same direction |

| 0 | No relation |

| -1 | Opposite |

Low correlation reduces risk.

Inflation

Inflation reduces purchasing power.

| Asset | Inflation Protection |

|---|---|

| Stocks | Strong |

| Bonds | Moderate |

| Real Estate | Strong |

| Gold | Strong |

| Cash | Weak |

Global Diversification

Invest across:

- U.S.

- Europe

- Emerging markets

Reduces country-specific risk.

Case Study 3: Long-Term Investor

Monthly investment: $500

Duration: 40 years

| Allocation | Final Value |

|---|---|

| 80% Stocks | $1.5M |

| 40% Stocks | $900K |

👉 Allocation determines retirement lifestyle.

Risk Tolerance vs Capacity

- Tolerance = Emotional ability

- Capacity = Financial ability

Both must match your allocation.

The 2026 Reality

Markets are influenced by:

- AI

- Inflation

- Global conflicts

But core principle remains:

Diversification + discipline = success

Final Takeaways: Build a Winning Asset Allocation Strategy

✔ Asset allocation drives returns

✔ Reduces risk

✔ Improves consistency

✔ Prevents emotional mistakes

✔ Builds long-term wealth

FAQs on Asset Allocation

Q1: What is the best asset allocation?

The best asset allocation depends on your age, financial goals, and risk tolerance. Younger investors often prefer higher stock exposure, while older investors focus more on bonds for stability.

Q2: Why is asset allocation important?

Asset allocation determines how your portfolio performs under different market conditions by balancing risk and return.

Q3: How often should you rebalance your portfolio?

Most experts recommend rebalancing once a year or whenever your allocation significantly changes.

Ultimate Conclusion

You don’t need:

- Perfect timing

- Expert stock picking

- Market predictions

You need:

A disciplined asset allocation strategy

Because ultimately:

Your portfolio mix determines your financial future.