Strategic Asset Allocation Guide for Long-Term Wealth Building

The Strategic Asset Allocation Guide is one of the most powerful wealth-building frameworks used by high-net-worth individuals, pension funds, and institutional investors across Tier-1 economies such as the United States, United Kingdom, Canada, and Australia.

It is a long-term investment strategy that focuses on building a balanced portfolio of stocks, bonds, real estate, and cash to maximize returns while minimizing risk over decades.

Unlike short-term trading or speculation, Strategic Asset Allocation is designed for:

- Retirement wealth creation

- Passive income generation

- Capital preservation

- Inflation protection

- Long-term financial independence

Strategic Asset Allocation (SAA) is one of the most important concepts in long-term investing and wealth management. It is the foundation used by pension funds, retirement accounts, sovereign wealth funds, endowments, financial advisors, and individual investors across Tier-1 countries such as the United States, United Kingdom, Canada, and Australia.

At its core, Strategic Asset Allocation means deciding how much of your money should be invested in different asset classes—such as stocks, bonds, cash, real estate, commodities, and international investments—based on your long-term goals, risk tolerance, and time horizon.

Instead of constantly reacting to market news, Strategic Asset Allocation focuses on building a disciplined portfolio structure designed to perform over decades.

What Is Strategic Asset Allocation?

Strategic Asset Allocation is a long-term investment strategy where investors create a target allocation among different asset classes and periodically rebalance the portfolio back to those targets.

The idea is simple:

- Decide your ideal investment mix

- Keep the allocation stable over time

- Rebalance occasionally

- Ignore short-term market noiseStrategic Asset Allocation Explained

For example, an investor may decide on:

- 60% Stocks

- 30% Bonds

- 10% Cash

Even if markets rise or fall, the investor keeps returning to this original allocation.

This creates discipline and reduces emotional investing.

Understanding the Term Word-by-Word

Strategic

“Strategic” means long-term planning.

It refers to decisions based on:

- Future goals

- Expected returns

- Risk management

- Financial planning

- Economic assumptions

Strategic investing usually focuses on periods of:

- 10 years

- 20 years

- 30 years

- Retirement timelines

This differs from short-term speculation.

Asset

An asset is anything that has financial value.

Common investment assets include:

| Asset Type | Meaning |

|---|---|

| Stocks | Ownership in companies |

| Bonds | Loans to governments or corporations |

| Cash | Savings and money market instruments |

| Real Estate | Property investments |

| Commodities | Gold, oil, agriculture |

| Alternatives | Hedge funds, private equity |

Each asset behaves differently during economic conditions.

Allocation

Allocation means dividing investments among assets.

Example:

If an investor has $100,000:

- $60,000 in stocks

- $30,000 in bonds

- $10,000 in cash

This division is the asset allocation.

Why Strategic Asset Allocation Matters

Research in finance consistently shows that asset allocation is one of the biggest drivers of long-term portfolio returns and risk.

Investment performance is often influenced more by:

- Portfolio structure

than by: - Individual stock selection

A properly diversified allocation can:

- Reduce volatility

- Improve consistency

- Lower emotional decision-making

- Protect during recessions

- Increase long-term compounding

Core Principle of Strategic Asset Allocation

The central principle is:

Different asset classes perform differently under different economic conditions.

Because no asset wins forever, diversification helps stabilize returns.

Major Asset Classes Explained

1. Stocks (Equities)

Stocks represent ownership in businesses.

Examples include:

- Apple

- Microsoft

- Amazon

Stocks provide:

- Capital appreciation

- Dividend income

- Inflation protection

Advantages

- Highest long-term growth potential

- Strong wealth creation

- Ownership in economic growth

Risks

- High volatility

- Market crashes

- Emotional stress

2. Bonds

Bonds are debt instruments.

When you buy a bond, you lend money to:

- Governments

- Corporations

Examples:

- U.S. Treasury Bonds

- Canadian Government Bonds

- Corporate Bonds

Advantages

- Stability

- Predictable income

- Lower volatility

Risks

- Interest rate risk

- Inflation risk

- Credit risk

3. Cash and Cash Equivalents

Includes:

- Savings accounts

- Treasury bills

- Money market funds

Advantages

- Liquidity

- Safety

- Emergency access

Risks

- Low returns

- Inflation erosion

4. Real Estate

Real estate can include:

- Residential property

- Commercial buildings

- REITs (Real Estate Investment Trusts)

Advantages

- Rental income

- Inflation hedge

- Diversification

Risks

- Illiquidity

- Property market downturns

- Maintenance costs

5. Commodities

Examples:

- Gold

- Silver

- Oil

- Agricultural products

Advantages

- Inflation protection

- Diversification

Risks

- Extreme price volatility

- Economic sensitivity

Strategic Asset Allocation vs Tactical Asset Allocation

| Strategic | Tactical |

|---|---|

| Long-term | Short-term |

| Stable allocation | Frequently adjusted |

| Disciplined | Opportunistic |

| Passive approach | Active management |

| Goal-oriented | Market timing oriented |

Strategic allocation focuses on consistency.

Tactical allocation attempts to outperform markets through temporary changes.

The Role of Risk Tolerance

Risk tolerance means the ability and willingness to handle investment losses.

Three common investor types:

| Investor Type | Characteristics |

|---|---|

| Conservative | Prioritizes safety |

| Moderate | Balanced approach |

| Aggressive | Pursues growth |

Example Asset Allocations

Conservative Portfolio

| Asset | Allocation |

|---|---|

| Bonds | 60% |

| Stocks | 30% |

| Cash | 10% |

Suitable for:

- Retirees

- Risk-averse investors

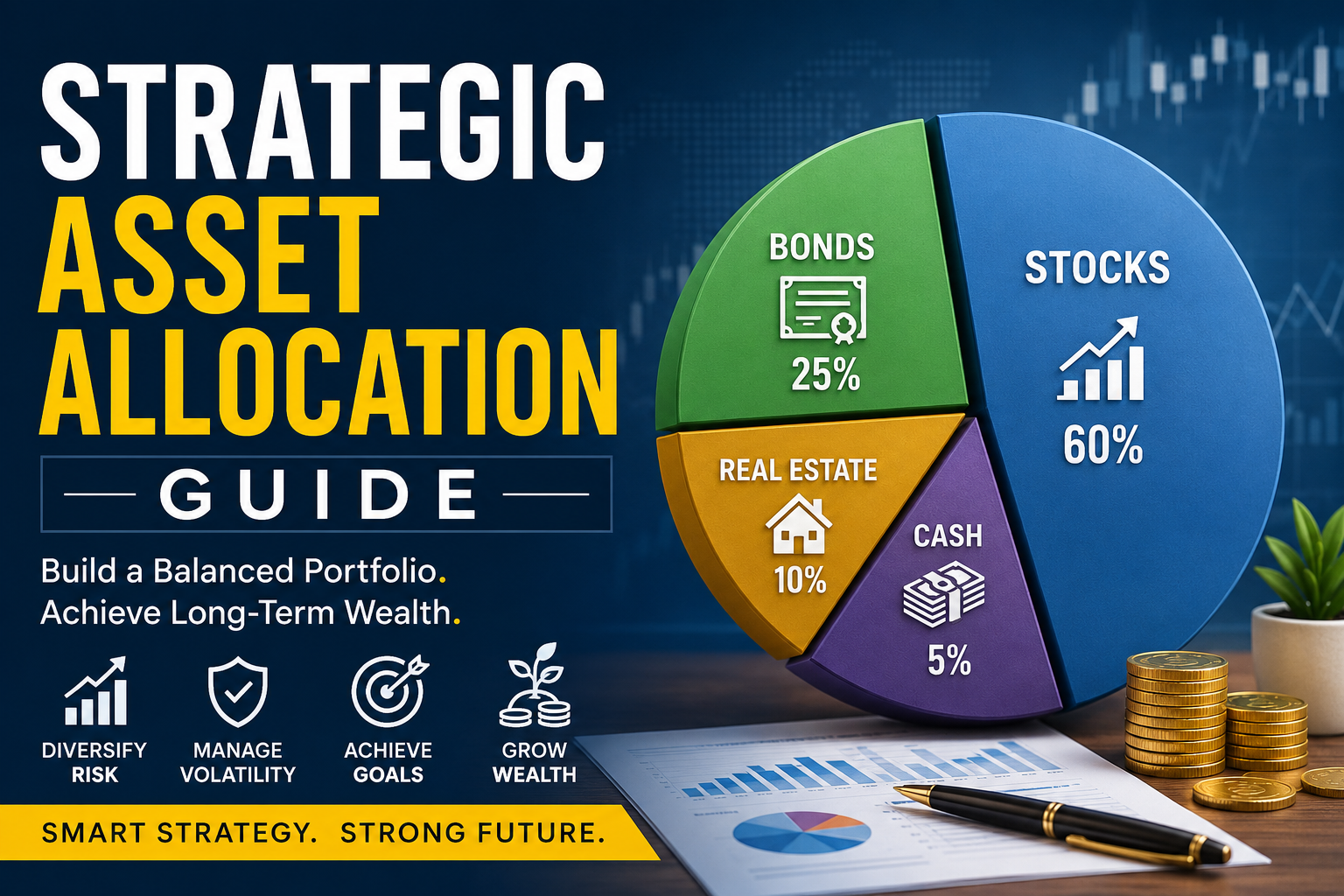

Moderate Portfolio

| Asset | Allocation |

|---|---|

| Stocks | 60% |

| Bonds | 35% |

| Cash | 5% |

Suitable for:

- Middle-aged professionals

- Long-term savers

Aggressive Portfolio

| Asset | Allocation |

|---|---|

| Stocks | 85% |

| Bonds | 10% |

| Cash | 5% |

Suitable for:

- Young investors

- Long investment horizons

Time Horizon and Allocation

Time horizon means how long money remains invested.

Generally:

| Time Horizon | Common Allocation |

|---|---|

| 1–3 years | Conservative |

| 5–10 years | Balanced |

| 20+ years | Aggressive |

Longer horizons allow investors to tolerate market volatility.

Modern Portfolio Theory (MPT)

Strategic Asset Allocation is heavily influenced by Modern Portfolio Theory developed by Harry Markowitz.

MPT suggests that investors can maximize returns for a given level of risk through diversification.

The key insight:

- Combining imperfectly correlated assets reduces portfolio risk.

Correlation in Asset Allocation

Correlation measures how assets move relative to each other.

| Correlation | Meaning |

|---|---|

| +1 | Move together |

| 0 | No relationship |

| -1 | Move opposite |

Strategic allocation seeks low-correlation assets.

Example:

- Stocks and bonds often behave differently during recessions.

Rebalancing Explained

Over time, portfolio weights change because assets grow at different rates.

Example:

- Original allocation: 60% stocks / 40% bonds

- After stock rally: 75% stocks / 25% bonds

Rebalancing means selling overweight assets and buying underweight assets.

Benefits:

- Maintains risk profile

- Encourages discipline

- Prevents overexposure

Example of Rebalancing

Suppose:

- Portfolio value = $200,000

- Target allocation = 60/40

After a stock boom:

- Stocks = $150,000

- Bonds = $50,000

Current allocation:

- 75% stocks

- 25% bonds

To rebalance:

- Sell some stocks

- Buy bonds

Return to:

- $120,000 stocks

- $80,000 bonds

Strategic Asset Allocation During Market Crashes

One major advantage of Strategic Asset Allocation is emotional stability.

During crises like:

- 2008 Financial Crisis

- COVID-19 crash

- Dot-com bubble

Disciplined investors often avoid panic selling.

Case Study: 2008 Global Financial Crisis

During 2008:

- Global stocks crashed

- Real estate collapsed

- Credit markets froze

Aggressive investors holding 100% stocks suffered major losses.

However, balanced portfolios containing:

- Bonds

- Cash

- Defensive assets

experienced smaller drawdowns.

Example:

| Portfolio | Approximate Loss |

|---|---|

| 100% Stocks | -50% |

| 60/40 Portfolio | -20% to -30% |

This demonstrates the value of diversification.

Case Study: COVID-19 Market Crash (2020)

In March 2020:

- Markets fell rapidly

- Fear dominated investors

Yet diversified portfolios recovered faster because:

- Central banks lowered rates

- Bonds stabilized portfolios

- Technology stocks rebounded strongly

Investors who maintained allocation discipline benefited from recovery.

Strategic Asset Allocation in Retirement Planning

Strategic allocation is central to retirement systems in Tier-1 countries.

Examples:

United States

Used in:

- 401(k) plans

- IRAs

- Pension funds

United Kingdom

Used in:

- ISA accounts

- SIPPs

Canada

Used in:

- RRSPs

- TFSAs

Australia

Used in:

- Superannuation funds

Target-date retirement funds automatically adjust allocations over time.

Lifecycle Investing

Lifecycle investing changes allocation as investors age.

General pattern:

| Age | Stock Allocation |

|---|---|

| 25 | 90% |

| 40 | 70% |

| 55 | 50% |

| 70 | 30% |

This reduces risk near retirement.

Inflation and Asset Allocation

Inflation reduces purchasing power.

Strategic allocation combats inflation through:

- Stocks

- Real estate

- Commodities

Cash alone usually loses value over time.

International Diversification

Many investors diversify globally.

Instead of owning only domestic companies, they invest internationally.

Benefits:

- Geographic diversification

- Currency diversification

- Exposure to emerging growth

Example regions:

- United States

- Europe

- Asia-Pacific

- Emerging markets

Currency Risk

International investing introduces currency fluctuations.

Example:

- U.S. investor buys European stocks

- Euro weakens against dollar

- Returns may decline

Strategic allocation may include currency-hedged investments.

Role of ETFs in Strategic Asset Allocation

Exchange-Traded Funds (ETFs) simplified diversification.

Popular providers include:

- Vanguard

- BlackRock

- State Street Global Advisors

ETFs allow investors to buy:

- Entire stock markets

- Bond indexes

- Commodity baskets

with one investment.

Example of a Strategic ETF Portfolio

| ETF Category | Allocation |

|---|---|

| U.S. Stocks | 40% |

| International Stocks | 20% |

| Bonds | 30% |

| REITs | 5% |

| Gold | 5% |

This creates broad diversification.

Behavioral Finance and Discipline

Human psychology often harms investing.

Common mistakes:

- Panic selling

- Chasing trends

- Buying high

- Selling low

Strategic allocation reduces emotional behavior through rules-based investing.

Dollar-Cost Averaging and Strategic Allocation

Many investors combine SAA with dollar-cost averaging.

This means investing fixed amounts regularly.

Example:

- $1,000 monthly into diversified funds

Benefits:

- Reduces timing risk

- Encourages consistency

- Builds investing habit

Tax Efficiency

Strategic allocation can improve after-tax returns.

Tax-efficient strategies include:

- Holding bonds in retirement accounts

- Using low-turnover ETFs

- Tax-loss harvesting

Different countries have different tax rules.

Strategic Asset Allocation for Institutions

Large institutions heavily depend on SAA.

Examples:

- Pension funds

- University endowments

- Insurance companies

- Sovereign wealth funds

Institutional portfolios may include:

- Private equity

- Infrastructure

- Hedge funds

- Venture capital

Yale Endowment Case Study

The Yale University endowment became famous for diversified allocation strategies.

Its portfolio included:

- Stocks

- Private equity

- Real assets

- Hedge funds

The approach emphasized:

- Long-term investing

- Diversification

- Illiquid assets

This influenced institutional investing globally.

Common Strategic Allocation Models

60/40 Portfolio

Classic balanced portfolio:

- 60% stocks

- 40% bonds

Traditionally popular among retirement investors.

All-Weather Portfolio

Popularized by Ray Dalio.

Designed to perform across:

- Inflation

- Deflation

- Growth

- Recession

Uses multiple asset classes.

Risk Parity Strategy

Risk parity allocates based on risk contribution rather than capital amount.

Goal:

- Equalize portfolio risk across assets

This differs from traditional allocation methods.

Challenges of Strategic Asset Allocation

1. Market Uncertainty

Future returns are unpredictable.

2. Inflation Shocks

High inflation can hurt bonds.

3. Interest Rate Changes

Rising rates affect fixed income assets.

4. Emotional Investing

Investors often abandon plans during crises.

5. Overconfidence

Some investors believe they can consistently time markets.

Advantages of Strategic Asset Allocation

| Advantage | Explanation |

|---|---|

| Discipline | Prevents emotional decisions |

| Diversification | Reduces concentration risk |

| Simplicity | Easy to manage |

| Long-term focus | Encourages patience |

| Risk control | Matches investor goals |

Disadvantages

| Disadvantage | Explanation |

|---|---|

| Limited flexibility | May miss short-term opportunities |

| Requires patience | Slow wealth-building process |

| Rebalancing costs | Taxes and transaction fees |

| Underperformance periods | Certain assets may lag for years |

Example: Young Professional in the USA

Sarah is 28 years old and saving for retirement.

Goals:

- Retire at 65

- Long investment horizon

- Moderate risk tolerance

Allocation:

- 80% global stocks

- 15% bonds

- 5% cash

She contributes monthly to:

- Index funds

- Retirement accounts

During market crashes:

- She continues investing

- Rebalances annually

Over decades, compounding may significantly grow wealth.

Example: Retiree in Canada

David is 68 and retired.

Goals:

- Preserve capital

- Generate income

- Reduce volatility

Allocation:

- 40% stocks

- 50% bonds

- 10% cash

This lower-risk allocation helps protect retirement income.

Strategic Asset Allocation and Economic Cycles

Different assets perform better during different environments.

| Economic Condition | Likely Winners |

|---|---|

| Expansion | Stocks |

| Recession | Bonds |

| Inflation | Commodities |

| Deflation | Government bonds |

Diversification helps navigate changing conditions.

Importance of Staying Invested

Missing the best market recovery days can dramatically reduce returns.

Strategic allocation encourages:

- Staying invested

- Long-term thinking

- Consistent participation

Strategic Allocation vs Stock Picking

Many investors focus too heavily on:

- Finding the next big stock

However, long-term success often depends more on:

- Allocation

- Diversification

- Risk management

than on selecting individual winners.

How Financial Advisors Use Strategic Allocation

Financial advisors assess:

- Goals

- Income

- Age

- Risk tolerance

- Time horizon

Then they recommend:

- Suitable allocation models

- Rebalancing schedules

- Tax strategies

Technology and Robo-Advisors

Modern robo-advisors automate Strategic Asset Allocation.

Examples include:

- Betterment

- Wealthfront

These platforms:

- Build diversified portfolios

- Rebalance automatically

- Lower investment costs

ESG and Strategic Allocation

ESG means:

- Environmental

- Social

- Governance

Many investors now integrate ESG preferences into allocations.

This may involve:

- Sustainable ETFs

- Low-carbon funds

- Ethical investing strategies

Future Trends in Strategic Asset Allocation

Emerging trends include:

- AI-driven portfolio management

- Alternative assets

- Cryptocurrency exposure

- Personalized investing

- Sustainable investing

Institutional portfolios continue evolving.

Final Thoughts

Strategic Asset Allocation is the backbone of successful long-term investing.

It helps investors:

- Manage risk

- Build diversified portfolios

- Stay disciplined

- Avoid emotional decisions

- Achieve financial goals

Rather than attempting to predict daily market movements, Strategic Asset Allocation focuses on:

- Structure

- Consistency

- Patience

- Long-term compounding

For investors in Tier-1 countries such as the United States, United Kingdom, Canada, and Australia, Strategic Asset Allocation remains one of the most effective frameworks for retirement planning, wealth preservation, and financial independence.

The key lesson is simple:

Long-term investing success is often determined not by predicting markets perfectly, but by maintaining a disciplined and diversified allocation strategy through all market conditions.