Risk Tolerance Explained

Risk Tolerance Explained is one of the most important concepts every investor must understand before building an investment portfolio. Whether you invest in stocks, bonds, ETFs, mutual funds, or retirement accounts, understanding your risk tolerance helps you make smarter financial decisions and avoid costly emotional mistakes.

In Tier-1 countries such as the United States, United Kingdom, Canada, and Australia, risk tolerance plays a central role in retirement investing, long-term wealth creation, tax-efficient investing, and financial independence planning.

A person with high risk tolerance may comfortably invest heavily in stocks during market crashes, while another person may panic after a 10% decline and sell everything. Neither investor is automatically “right” or “wrong.” The correct approach depends on financial goals, time horizon, income stability, personality, and investment experience.

This guide explains risk tolerance in detail, including terminology, types of investors, portfolio allocation, behavioral finance, examples, and real-world case studies.

What Is Risk Tolerance?

Risk tolerance refers to the amount of financial uncertainty, volatility, or potential investment loss an investor is willing and able to accept.

In simple words:

- It measures how comfortable someone is with investment risk.

- It determines how much market fluctuation they can emotionally tolerate.

- It influences investment decisions and portfolio allocation.

For example:

- If a portfolio drops 30% during a recession and the investor remains calm, that investor likely has high risk tolerance.

- If an investor panics during a 10% decline and sells investments immediately, they likely have low risk tolerance.

Risk tolerance combines both:

- Emotional capacity for risk

- Financial ability to absorb losses

These two factors are different.

A wealthy investor may financially survive a large loss but emotionally dislike volatility. Another investor may emotionally tolerate volatility but financially cannot afford losses because retirement is near.

Understanding the Word “Risk”

In investing, risk does not simply mean “losing money.”

Risk means uncertainty regarding future investment outcomes.

Common investment risks include:

| Risk Type | Meaning |

|---|---|

| Market Risk | Entire market declines |

| Inflation Risk | Purchasing power decreases |

| Interest Rate Risk | Bond prices fall when rates rise |

| Credit Risk | Borrower may default |

| Liquidity Risk | Hard to sell an investment quickly |

| Currency Risk | Exchange rates affect returns |

| Sequence of Returns Risk | Poor early retirement returns damage portfolios |

For long-term investors, volatility is often temporary, but emotional reactions to volatility can permanently damage wealth.

Risk vs Volatility

Many beginners confuse risk with volatility.

Volatility means price fluctuations.

For example:

- A stock moving up and down 5% daily is volatile.

- A government bond with stable prices has low volatility.

However:

- Volatility is not always dangerous.

- Long-term investors may benefit from temporary volatility.

Example:

During the 2008 Global Financial Crisis, many stock portfolios lost over 40%.

But investors who stayed invested often recovered and achieved strong long-term returns later.

Why Risk Tolerance Matters

Risk tolerance affects nearly every financial decision.

It influences:

- Asset allocation

- Retirement planning

- Investment strategy

- Portfolio diversification

- Stock selection

- Bond allocation

- Emergency fund requirements

- Withdrawal strategies

- Rebalancing decisions

A mismatch between investments and risk tolerance often causes:

- Panic selling

- Emotional investing

- Poor long-term returns

- Financial stress

- Retirement shortfalls

Example of Risk Tolerance

Suppose two investors each invest $100,000.

Investor A

- Age: 30

- Stable technology job

- Long-term investing horizon

- Comfortable with market volatility

Portfolio:

- 90% stocks

- 10% bonds

During a market crash, portfolio falls to $70,000.

Investor A continues investing monthly and waits for recovery.

Investor B

- Age: 60

- Near retirement

- Depends on investments for income

- Dislikes volatility

Portfolio:

- 40% stocks

- 60% bonds

During the same market crash, portfolio falls only slightly.

Investor B prioritizes stability over aggressive growth.

This example shows how risk tolerance changes investment strategy.

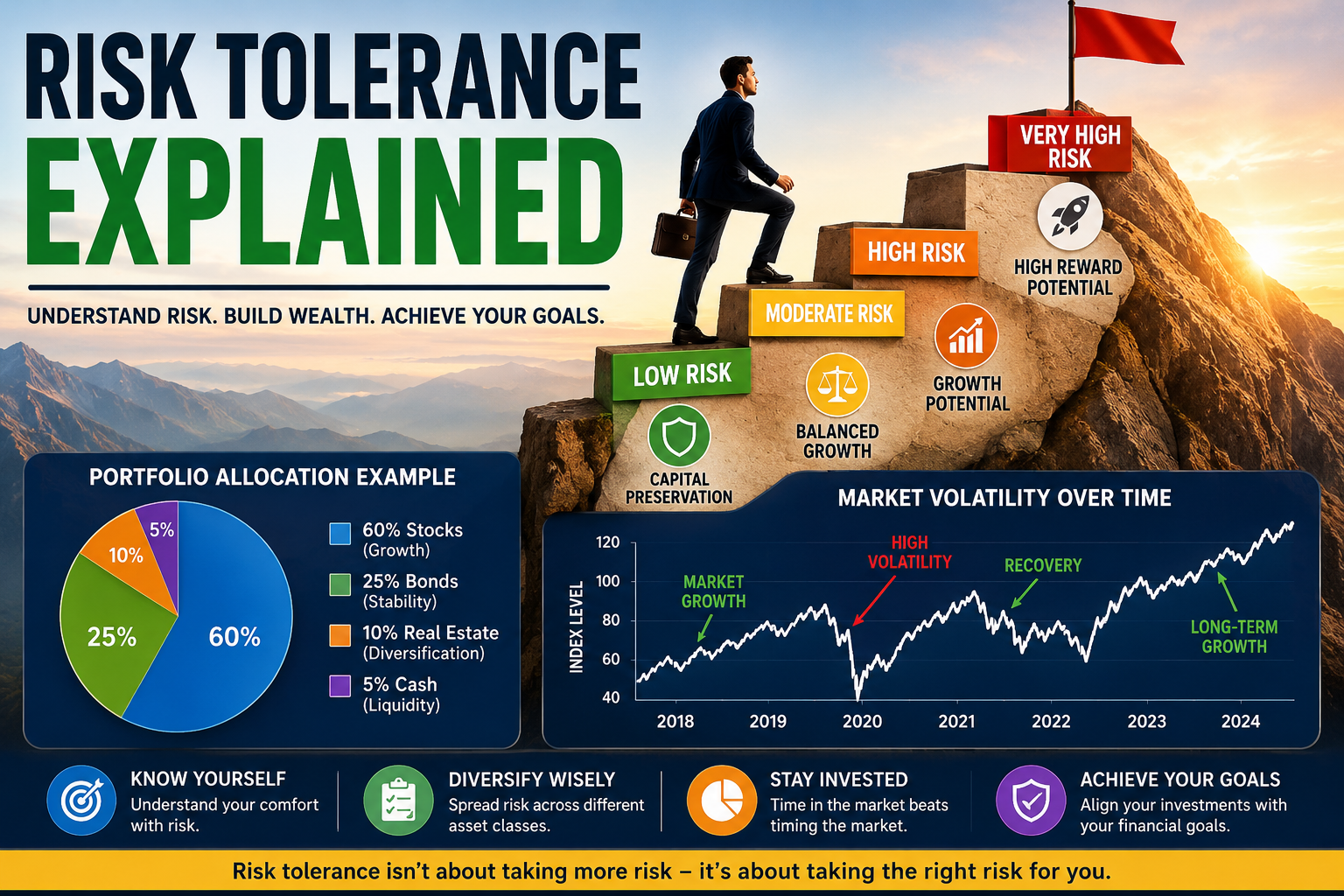

Types of Risk Tolerance

Financial advisors usually divide investors into three categories.

1. Conservative Investor

A conservative investor prioritizes capital preservation over growth.

Characteristics

- Dislikes market volatility

- Prefers stable returns

- Focuses on protecting wealth

- Avoids speculative investments

Typical Investments

- Government bonds

- Treasury securities

- High-yield savings accounts

- Certificates of deposit (CDs)

- Dividend stocks

- Conservative mutual funds

Example Allocation

| Asset | Percentage |

|---|---|

| Bonds | 70% |

| Stocks | 20% |

| Cash | 10% |

Suitable For

- Retirees

- Near-retirement investors

- Investors with low emotional tolerance for losses

2. Moderate Investor

Moderate investors balance growth and stability.

Characteristics

- Accepts some volatility

- Wants long-term growth

- Prefers diversified portfolios

- Comfortable with temporary declines

Typical Allocation

| Asset | Percentage |

|---|---|

| Stocks | 60% |

| Bonds | 35% |

| Cash | 5% |

Suitable For

- Mid-career professionals

- Long-term retirement investors

- Balanced investors

3. Aggressive Investor

Aggressive investors seek maximum growth.

Characteristics

- Comfortable with major volatility

- Long investment horizon

- Strong focus on wealth accumulation

- Accepts temporary large losses

Typical Allocation

| Asset | Percentage |

|---|---|

| Stocks | 90% |

| Bonds | 5% |

| Cash | 5% |

Suitable For

- Young investors

- High-income earners

- Investors with decades before retirement

Risk Capacity vs Risk Tolerance

These terms are often confused.

Risk Tolerance

Emotional willingness to accept volatility.

Risk Capacity

Financial ability to handle losses.

Example:

A 28-year-old software engineer may have:

- High risk capacity

- High risk tolerance

A 63-year-old retiree may have:

- Low risk capacity

- Moderate emotional tolerance

Investment plans must consider both.

Factors That Affect Risk Tolerance

Several factors influence investor behavior.

1. Age

Younger investors generally tolerate more risk because they have more time to recover from market downturns.

Example:

A 25-year-old investing for retirement has decades before withdrawals begin.

A 65-year-old retiree may prioritize capital preservation.

2. Income Stability

People with stable income often tolerate more investment risk.

Example:

- Government employee with pension → higher stability

- Freelancer with irregular income → lower stability

Stable income allows continued investing during market declines.

3. Time Horizon

Time horizon means the length of time before funds are needed.

Longer time horizons generally support higher equity exposure.

Example:

- Retirement in 35 years → aggressive allocation possible

- Home purchase in 2 years → conservative allocation preferred

4. Financial Knowledge

Experienced investors usually understand market cycles better.

This often improves emotional control during volatility.

5. Personality

Some individuals naturally tolerate uncertainty better.

Behavioral finance studies show emotions strongly affect investment decisions.

6. Family Responsibilities

Investors supporting children or dependents may become more conservative.

Psychological Side of Risk Tolerance

Risk tolerance is deeply connected to psychology.

Common emotional biases include:

| Bias | Meaning |

|---|---|

| Loss Aversion | Losses feel more painful than gains |

| Herd Mentality | Following crowds |

| Recency Bias | Believing recent events continue forever |

| Overconfidence | Assuming superior investing ability |

| Panic Selling | Selling during market crashes |

Behavioral mistakes often reduce long-term returns.

Loss Aversion Explained

Loss aversion is one of the most powerful investing emotions.

People generally feel:

- A $10,000 loss hurts more than

- A $10,000 gain feels good

This causes investors to:

- Sell during crashes

- Avoid risk entirely

- Miss long-term growth

Real-World Example: COVID-19 Crash (2020)

During the COVID-19 market crash:

- Major indices fell rapidly

- Investors panicked globally

- Many sold investments near market lows

However:

Investors who remained invested often experienced strong recoveries afterward.

This demonstrated how emotional reactions affect long-term wealth creation.

Risk Tolerance and Asset Allocation

Asset allocation refers to dividing investments among different asset classes.

The main asset classes include:

- Stocks

- Bonds

- Cash

- Real estate

- Commodities

- Alternatives

Risk tolerance determines allocation percentages.

Stocks and Risk Tolerance

Stocks historically produce higher returns but higher volatility.

Example characteristics:

| Feature | Stocks |

|---|---|

| Growth Potential | High |

| Volatility | High |

| Income Stability | Lower |

| Inflation Protection | Strong |

Long-term investors often hold more stocks.

Bonds and Risk Tolerance

Bonds generally provide:

- Lower volatility

- Stable income

- Lower expected returns

Common bond types include:

- Government bonds

- Corporate bonds

- Municipal bonds

Bonds become increasingly important near retirement.

Cash and Emergency Funds

Cash reduces volatility but loses purchasing power due to inflation.

Emergency funds help investors avoid selling investments during crises.

Typical recommendation:

- 3–12 months of living expenses

Risk Tolerance in Retirement Planning

Risk tolerance changes during retirement planning stages.

In Your 20s

Focus:

- Growth

- Aggressive investing

- Long-term compounding

Typical allocation:

- 80–100% equities

In Your 30s and 40s

Focus:

- Growth with increasing diversification

- Family responsibilities

- Retirement accumulation

Typical allocation:

- 60–80% equities

In Your 50s and 60s

Focus:

- Capital preservation

- Income generation

- Sequence risk management

Typical allocation:

- Higher bond exposure

Sequence of Returns Risk

This risk becomes important during retirement.

Bad market returns early in retirement can permanently damage portfolios.

Example:

Two retirees earn identical average returns.

However:

- One experiences crashes early

- Another experiences crashes later

The retiree facing early losses may run out of money faster.

Risk Tolerance Questionnaires

Financial advisors use questionnaires to assess investors.

Questions include:

- How would you react to a 20% market decline?

- When will you need the money?

- What is your investment goal?

- How stable is your income?

- How experienced are you with investing?

These help determine suitable portfolio allocations.

Example Portfolio Allocations

Conservative Portfolio

| Asset Class | Allocation |

|---|---|

| Bonds | 60% |

| Stocks | 30% |

| Cash | 10% |

Balanced Portfolio

| Asset Class | Allocation |

|---|---|

| Stocks | 60% |

| Bonds | 35% |

| Cash | 5% |

Aggressive Portfolio

| Asset Class | Allocation |

|---|---|

| Stocks | 90% |

| Bonds | 5% |

| Cash | 5% |

Case Study 1: Young Tech Employee in the USA

Location: United States

Investor:

- Age 29

- Software engineer

- High income

- No children

- Retirement goal in 35 years

Risk tolerance:

- High

Strategy:

- 90% stock index funds

- 10% bonds

- Monthly investing into 401(k) and Roth IRA

Why aggressive allocation works:

- Long investment horizon

- Stable career

- Strong earning potential

- Ability to recover from downturns

Case Study 2: Retired Couple in Canada

Location: Canada

Investor profile:

- Ages 67 and 69

- Retired teachers

- Depend on investment income

Risk tolerance:

- Moderate to low

Strategy:

- 45% dividend stocks

- 45% bonds

- 10% cash

Goal:

- Stable retirement income

- Reduced volatility

- Protection from severe downturns

Case Study 3: Business Owner in Australia

Location: Australia

Investor profile:

- Age 45

- Owns construction business

- Variable income

Risk tolerance:

- Moderate

Strategy:

- Diversified ETF portfolio

- Real estate exposure

- Large emergency reserve

Reason:

Business income already creates financial uncertainty, so portfolio risk is moderated.

Risk Tolerance and Market Crashes

Market crashes test true risk tolerance.

Many investors believe they are aggressive investors until major losses occur.

Example:

An investor says they can tolerate risk.

But during a 35% decline:

- Panic begins

- Sleep is affected

- Investments are sold

This indicates actual tolerance is lower than assumed.

Dot-Com Bubble Example

During the late 1990s:

Technology stocks surged dramatically.

After the bubble burst:

- Many companies collapsed

- Investors lost large amounts

- Some portfolios required years to recover

Investors with diversified portfolios and appropriate risk management recovered more effectively.

2008 Global Financial Crisis

The Global Financial Crisis became one of the most important investing lessons about risk tolerance.

Key lessons:

- Diversification matters

- Panic selling destroys wealth

- Emotional investing creates poor outcomes

- Long-term investing often outperforms market timing

Inflation Risk

Being “too conservative” also creates risk.

Example:

If inflation averages 3% annually and savings accounts earn only 1%, purchasing power declines.

This means:

Avoiding all risk may actually increase long-term financial danger.

Risk Tolerance and Inflation

Growth assets like stocks historically help combat inflation.

Over long periods:

- Equities generally outpace inflation

- Cash often loses real purchasing power

This is why younger investors typically hold more equities.

Diversification and Risk Reduction

Diversification means spreading investments across multiple asset classes.

Goal:

Reduce overall portfolio risk.

Example diversified portfolio:

- US stocks

- International stocks

- Bonds

- Real estate

- Cash reserves

Diversification helps reduce dependence on a single investment.

International Diversification

Investing globally can reduce country-specific risk.

Example:

An investor holding only domestic stocks may face concentrated economic exposure.

Global diversification spreads risk across regions.

Risk Tolerance and ETFs

ETFs are popular because they offer:

- Diversification

- Low costs

- Simplicity

- Broad market exposure

Example ETFs:

- S&P 500 ETFs

- Total market ETFs

- International ETFs

- Bond ETFs

Investors choose ETF allocations based on risk tolerance.

Risk Tolerance in High-Net-Worth Investing

Wealthy investors may take different approaches.

Some prioritize:

- Capital preservation

- Tax efficiency

- Alternative investments

Others continue aggressive growth investing.

Risk tolerance remains personal regardless of wealth level.

Risk Tolerance and FIRE Movement

The FIRE movement stands for:

Financial Independence, Retire Early.

FIRE investors often maintain:

- High savings rates

- Aggressive equity allocations

- Long-term investing discipline

However, early retirement increases sequence risk considerations.

How Financial Advisors Use Risk Tolerance

Advisors build portfolios aligned with client profiles.

Typical process:

- Assess goals

- Evaluate risk tolerance

- Analyze time horizon

- Determine asset allocation

- Rebalance periodically

Professional portfolio management often focuses more on behavior management than stock picking.

Rebalancing and Risk Tolerance

Over time, portfolio allocations change.

Example:

- Stocks rise significantly

- Portfolio becomes more aggressive

Rebalancing restores target allocations.

Example:

- Sell some stocks

- Buy bonds

- Return to desired risk level

Dynamic Risk Tolerance

Risk tolerance can change over time.

Reasons include:

- Marriage

- Children

- Retirement

- Economic conditions

- Job loss

- Wealth increase

Periodic reassessment is important.

Common Mistakes Investors Make

1. Taking Too Much Risk

Example:

- Investing entire savings in speculative stocks

- Ignoring diversification

Result:

Large losses during downturns.

2. Taking Too Little Risk

Example:

- Holding only cash for decades

Result:

Inflation erodes wealth.

3. Emotional Investing

Buying high and selling low damages returns.

4. Chasing Trends

Investing based on hype often increases risk.

Examples include:

- Meme stocks

- Speculative bubbles

- Cryptocurrency mania

Risk Tolerance and Wealth Building

Long-term wealth creation usually requires accepting some level of market risk.

Historically:

- Equities outperform cash over long periods

- Compounding rewards disciplined investors

- Diversification improves risk-adjusted returns

Understanding Risk-Adjusted Return

Higher returns alone are not enough.

Investors should evaluate:

Return relative to risk taken.

Example:

| Portfolio | Return | Risk |

|---|---|---|

| Portfolio A | 10% | Very High |

| Portfolio B | 8% | Moderate |

Many investors prefer Portfolio B because the risk-adjusted return is superior.

Sharpe Ratio Explained

The Sharpe Ratio measures return relative to volatility.

Higher Sharpe Ratio:

- Better risk-adjusted performance

Professional investors often use this metric when comparing portfolios.

Emotional Discipline and Risk Tolerance

Successful investing often depends less on intelligence and more on emotional control.

Important habits include:

- Staying invested during downturns

- Avoiding panic

- Maintaining diversification

- Following long-term plans

- Ignoring short-term noise

Example of Long-Term Discipline

Suppose an investor consistently contributes monthly into diversified index funds for 30 years.

Even after:

- Recessions

- Crashes

- Bear markets

- Inflation spikes

Long-term compounding may create substantial wealth.

Consistency often matters more than perfect timing.

Building a Portfolio Based on Risk Tolerance

Step 1: Define Goals

Examples:

- Retirement

- Home purchase

- Financial independence

- Education funding

Step 2: Determine Time Horizon

Longer horizons generally allow higher risk exposure.

Step 3: Assess Emotional Comfort

Ask:

“How would I react during a major market decline?”

Step 4: Build Asset Allocation

Choose stock, bond, and cash percentages.

Step 5: Diversify

Reduce concentration risk.

Step 6: Rebalance Periodically

Maintain desired risk profile.

Modern Portfolio Theory and Risk Tolerance

Modern Portfolio Theory suggests investors can optimize portfolios by balancing risk and return through diversification.

Core idea:

Different assets behave differently under market conditions.

Combining assets may improve portfolio efficiency.

Efficient Frontier Explained

The efficient frontier represents portfolios offering:

- Maximum expected return

for - A given level of risk

This concept helps advisors design optimized portfolios.

Risk Tolerance Across Economic Cycles

Investor emotions change during:

- Bull markets

- Bear markets

- Recessions

- Recoveries

People often become:

- Overconfident during booms

- Fearful during crashes

True risk tolerance is revealed during downturns.

Key Lessons About Risk Tolerance

- Every investor has different risk preferences.

- Risk tolerance changes over time.

- Emotional discipline matters greatly.

- Diversification reduces unnecessary risk.

- Avoiding all risk may increase inflation risk.

- Asset allocation should match goals and personality.

- Long-term investing generally rewards patience.

Final Thoughts

Risk tolerance is the foundation of successful investing. It shapes portfolio construction, retirement planning, wealth preservation, and long-term financial success.

Understanding risk tolerance helps investors:

- Avoid emotional decisions

- Stay invested during volatility

- Build sustainable portfolios

- Align investments with life goals

- Improve long-term outcomes

The best portfolio is not necessarily the one with the highest return potential. The best portfolio is the one an investor can consistently hold through market cycles without abandoning the strategy.

For investors in the United States, United Kingdom, Canada, and Australia, understanding risk tolerance is essential for navigating retirement systems, tax-efficient investing, market volatility, and long-term wealth creation.

In investing, managing emotions is often just as important as managing money.