The Role of Bonds in a Portfolio

Introduction

The Role of Bonds in a Portfolio is one of the most important concepts in modern investing. Bonds help investors generate income, reduce risk, preserve capital, and create a balanced investment strategy that can withstand different market conditions.

When most people think about investing, they immediately think about stocks. Stocks receive most of the media attention because they can generate high returns, create millionaires, and move dramatically during market booms and crashes. However, professional investors, retirement planners, pension funds, insurance companies, and wealthy families rarely build portfolios using stocks alone. Instead, they combine stocks with another major asset class: bonds.

Bonds play a critical role in portfolio construction because they help investors manage risk, preserve capital, generate stable income, and reduce overall volatility. In countries such as the United States, United Kingdom, Canada, and Australia, bonds are foundational components of retirement portfolios, pension systems, institutional investing, and wealth management strategies.

Understanding bonds is essential for anyone who wants to build long-term wealth while controlling financial risk. During economic crises, stock market crashes, recessions, and periods of uncertainty, bonds often act as stabilizers within an investment portfolio.

This article explains the role of bonds in a portfolio in detail, including:

- What bonds are

- How bonds work

- Types of bonds

- Benefits and risks of bonds

- Bond terminology

- Bond allocation strategies

- Bonds vs stocks

- How bonds reduce portfolio risk

- Interest rates and bond prices

- Real-world case studies

- Retirement portfolio examples

- Modern portfolio theory and bonds

- Mistakes investors make with bonds

- Bond investing strategies for Tier-1 countries

What Is a Bond?

A bond is a fixed-income investment where an investor lends money to a government, corporation, or institution in exchange for regular interest payments and repayment of the principal at maturity.

In simple terms:

- You lend money

- The issuer pays interest

- You receive your original investment back later

A bond is essentially a loan.

Simple Example of a Bond

Suppose the U.S. government issues a 10-year bond with:

- Face value: $1,000

- Interest rate: 5%

- Maturity: 10 years

If you buy this bond:

- You lend $1,000

- You receive $50 annually

- After 10 years, you get your $1,000 back

The annual interest payment is called the coupon payment.

Why Governments and Companies Issue Bonds

Organizations issue bonds to raise money.

Governments use bonds for:

- Infrastructure

- Defense

- Healthcare

- Public services

- Debt refinancing

Companies issue bonds for:

- Expansion

- Research

- Acquisitions

- Operations

- Debt management

Instead of borrowing from banks, issuers borrow from investors.

Important Bond Terms Explained

1. Face Value (Par Value)

The original amount of the bond.

Usually:

- $1,000 in the U.S.

- £100 in the UK

- CAD 1,000 in Canada

- AUD 1,000 in Australia

2. Coupon Rate

The annual interest paid by the bond.

Example:

A 4% coupon on a $1,000 bond pays $40 yearly.

3. Yield

Yield measures the return investors earn from a bond.

Different yields include:

- Current yield

- Yield to maturity

- Real yield

Yield is one of the most important concepts in bond investing.

4. Maturity

The date when the bond issuer repays the principal.

Examples:

- 2-year bond

- 10-year bond

- 30-year bond

5. Credit Rating

A measure of the issuer’s financial strength.

Major rating agencies include:

- Moody’s

- S&P Global

- Fitch Ratings

Higher ratings usually mean lower risk.

Types of Bonds

1. Government Bonds

Issued by national governments.

Examples include:

- U.S. Treasury Bonds

- UK Gilts

- Canadian Government Bonds

- Australian Government Bonds

Government bonds are usually considered safer than corporate bonds.

2. Corporate Bonds

Issued by companies.

Examples:

- Technology companies

- Banks

- Utility companies

Corporate bonds usually offer higher yields because they carry more risk.

3. Municipal Bonds

Issued by local governments or municipalities.

Common in the United States.

Used to fund:

- Schools

- Roads

- Hospitals

- Infrastructure

Many municipal bonds offer tax advantages.

4. High-Yield Bonds

Also called junk bonds.

These bonds:

- Offer higher interest

- Carry higher default risk

Used by:

- Risk-tolerant investors

- Income-focused portfolios

5. Inflation-Protected Bonds

These bonds adjust with inflation.

Examples:

- TIPS in the U.S.

- Inflation-linked gilts in the UK

They help protect purchasing power.

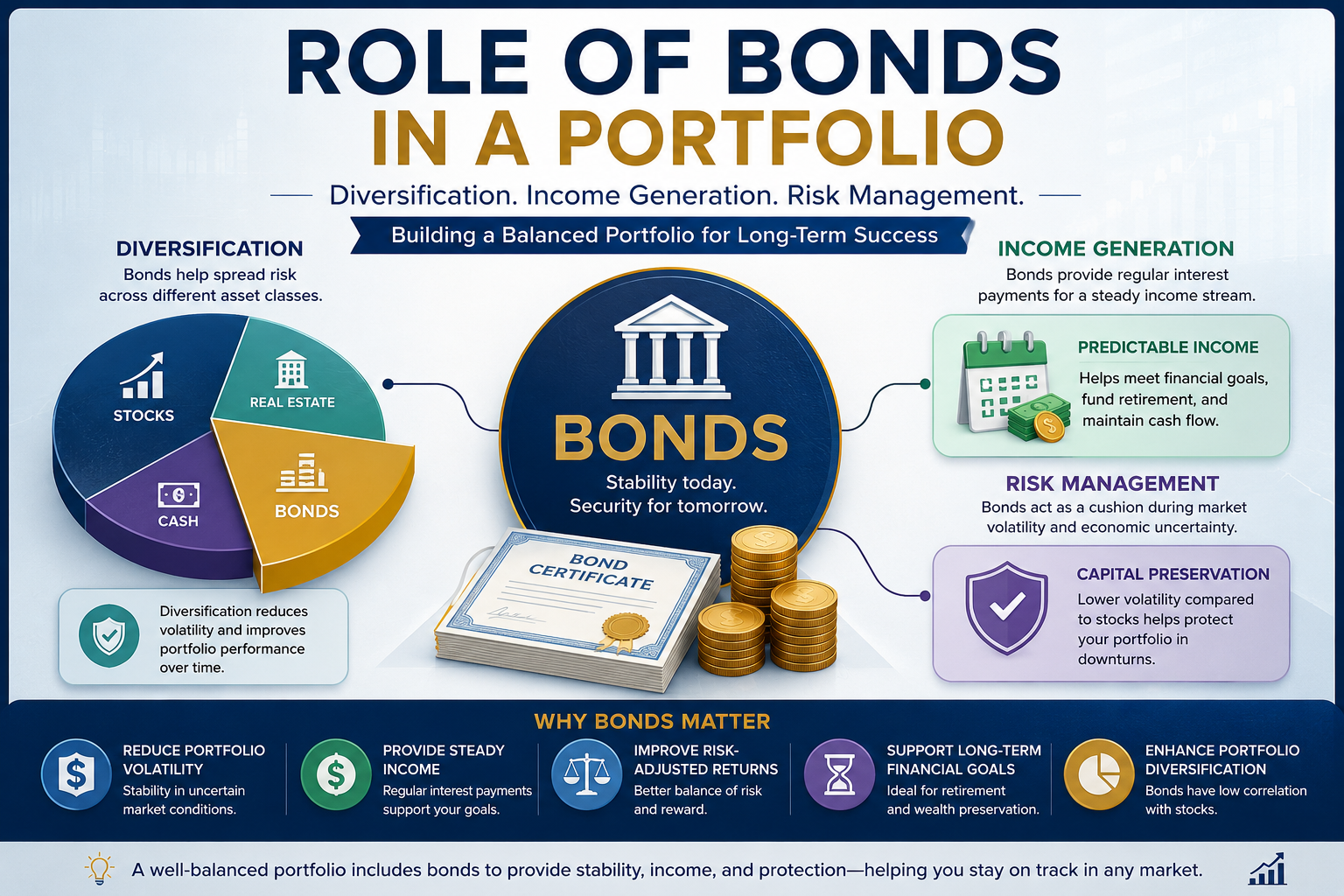

Why Bonds Matter in a Portfolio

The primary role of bonds is not maximizing returns.

The primary roles are:

- Capital preservation

- Income generation

- Risk reduction

- Portfolio diversification

- Stability during stock crashes

Bonds and Portfolio Diversification

Diversification means spreading investments across different asset classes.

A diversified portfolio may include:

- Stocks

- Bonds

- Real estate

- Cash

- Commodities

Bonds often move differently from stocks.

This lower correlation helps stabilize portfolios.

Understanding Correlation

Correlation measures how assets move relative to one another.

- Positive correlation = move together

- Negative correlation = move opposite

- Low correlation = move independently

Historically, high-quality bonds often had low or negative correlation with stocks during market stress.

How Bonds Reduce Portfolio Volatility

Volatility means how much investments fluctuate in value.

Stocks:

- Higher volatility

- Higher growth potential

Bonds:

- Lower volatility

- More stable returns

Adding bonds reduces large portfolio swings.

Example: Stock-Only Portfolio vs Balanced Portfolio

Portfolio A

- 100% stocks

Portfolio B

- 60% stocks

- 40% bonds

During a stock market crash:

- Portfolio A may decline 40%

- Portfolio B may decline 20%–25%

The balanced portfolio experiences smaller losses.

The Psychological Benefit of Bonds

One overlooked benefit of bonds is behavioral stability.

During bear markets:

- Many investors panic

- They sell stocks at losses

- Emotional decisions destroy long-term wealth

Bonds help investors stay calm because:

- Portfolio declines are smaller

- Income continues

- Stability improves confidence

This psychological advantage is extremely important.

Bonds as an Income Source

Bonds generate predictable cash flow.

This is valuable for:

- Retirees

- Pension funds

- Conservative investors

- Income-focused portfolios

Unlike stocks, which may cut dividends, many bonds provide contractual interest payments.

Bonds in Retirement Portfolios

Retirement investing focuses on:

- Income stability

- Risk management

- Capital preservation

As investors age, bonds become increasingly important.

The Traditional 60/40 Portfolio

The classic retirement portfolio is:

- 60% stocks

- 40% bonds

This strategy became popular because it balanced:

- Growth

- Income

- Risk reduction

Historically, the 60/40 portfolio performed well during many economic cycles.

Case Study: 2008 Financial Crisis

What Happened?

The 2008 crisis caused:

- Massive stock declines

- Bank failures

- Housing market collapse

The severely impacted investors worldwide.

Stock Market Performance

The S&P 500 fell approximately 37% in 2008.

Many investors panicked.

Bond Performance

High-quality U.S. Treasury bonds performed relatively well because investors sought safety.

Portfolios containing bonds:

- Experienced smaller losses

- Recovered faster

- Maintained liquidity

This demonstrated bonds’ defensive role.

Bonds During Recessions

During recessions:

- Businesses slow down

- Unemployment rises

- Stock earnings decline

Central banks often reduce interest rates to stimulate the economy.

Lower rates can increase bond prices, especially for high-quality bonds.

Understanding Interest Rates and Bonds

Interest rates are one of the most important drivers of bond prices.

Key Rule

When interest rates rise:

- Bond prices fall

When interest rates fall:

- Bond prices rise

This inverse relationship is fundamental to bond investing.

Why Bond Prices Fall When Rates Rise

Suppose:

- You own a 3% bond

- New bonds now pay 5%

Your bond becomes less attractive.

To compete:

- Your bond’s price falls

This adjusts the yield upward.

Duration Explained

Duration measures bond sensitivity to interest rate changes.

Long-duration bonds:

- More sensitive to rates

- Higher volatility

Short-duration bonds:

- Less sensitive

- More stable

Example of Duration Risk

Short-Term Bond

- 2-year maturity

- Smaller price swings

Long-Term Bond

- 30-year maturity

- Larger price swings

Long-term bonds can decline sharply when rates rise.

Case Study: 2022 Bond Market Decline

In 2022:

- Inflation surged

- Central banks aggressively raised rates

Both stocks and bonds declined simultaneously.

This challenged the belief that bonds always protect portfolios.

However:

- Bonds still provided income

- Future yields improved

- Long-term diversification benefits remained relevant

Inflation and Bonds

Inflation reduces purchasing power.

If inflation exceeds bond yields:

- Real returns become negative

Example:

- Bond yield = 3%

- Inflation = 5%

- Real return = -2%

This is inflation risk.

Inflation-Protected Securities

Governments created inflation-linked bonds to address this issue.

Examples:

- TIPS (Treasury Inflation-Protected Securities)

- Inflation-indexed bonds

These securities adjust principal values with inflation.

Bonds vs Stocks

| Feature | Bonds | Stocks |

|---|---|---|

| Ownership | Loan | Ownership stake |

| Income | Fixed interest | Dividends |

| Volatility | Lower | Higher |

| Growth Potential | Lower | Higher |

| Priority in Bankruptcy | Higher | Lower |

| Stability | More stable | More volatile |

Risk Types in Bond Investing

1. Interest Rate Risk

Bond prices fall when rates rise.

2. Credit Risk

Issuer may default.

Higher in:

- Corporate bonds

- High-yield bonds

Lower in:

- Government bonds

3. Inflation Risk

Inflation reduces real returns.

4. Reinvestment Risk

Future interest payments may be reinvested at lower rates.

5. Liquidity Risk

Some bonds are difficult to sell quickly.

Bond Ratings Explained

Investment-grade bonds:

- Lower default risk

- Lower yields

Junk bonds:

- Higher default risk

- Higher yields

Ratings categories:

- AAA

- AA

- A

- BBB

- BB

- B

- CCC

BBB and above are generally investment grade.

Investment Grade vs High Yield

Investment Grade Bonds

Suitable for:

- Conservative investors

- Retirees

- Stability-focused portfolios

High-Yield Bonds

Suitable for:

- Aggressive investors

- Higher income strategies

But they behave more like stocks during crises.

Bond Funds vs Individual Bonds

Individual Bonds

Advantages:

- Predictable maturity

- Known cash flow

Disadvantages:

- Less diversification

- More complex

Bond Funds

Advantages:

- Diversification

- Professional management

- Easy access

Disadvantages:

- No fixed maturity date

ETFs and Bond Investing

Bond ETFs became extremely popular.

Major providers include:

- Vanguard

- BlackRock

- State Street Global Advisors

Bond ETFs provide:

- Liquidity

- Diversification

- Low fees

Case Study: Retiree Portfolio

Investor Profile

Name: Sarah

Age: 67

Country: United States

Goal: Retirement income

Portfolio Allocation

- 45% stocks

- 50% bonds

- 5% cash

Why Bonds Matter Here

Sarah depends on her portfolio for living expenses.

Bonds provide:

- Predictable income

- Lower volatility

- Stability during market downturns

Without bonds, retirement withdrawals during crashes could permanently damage her portfolio.

Sequence of Returns Risk

This risk occurs when:

- Retirees withdraw money

- Markets decline early in retirement

Poor early returns can significantly reduce portfolio longevity.

Bonds help reduce this risk.

Bond Ladder Strategy

A bond ladder involves buying bonds with different maturities.

Example:

- 1-year bond

- 3-year bond

- 5-year bond

- 10-year bond

Benefits:

- Reduced reinvestment risk

- Regular cash flow

- Interest rate management

The Role of Bonds for Young Investors

Young investors often focus heavily on stocks.

However, bonds can still help:

- Reduce volatility

- Improve diversification

- Provide stability

Some younger investors use:

- 10%–20% bond allocations

Others prefer nearly all-stock portfolios.

Age-Based Bond Allocation

Traditional rule:

Bond percentage = your age

Example:

- Age 40 = 40% bonds

- Age 60 = 60% bonds

Modern investors sometimes use lower bond allocations because:

- People live longer

- Inflation risk increased

- Interest rates vary

Modern Portfolio Theory and Bonds

Harry Markowitz developed Modern Portfolio Theory (MPT).

Core idea:

- Investors should maximize return for a given level of risk.

Bonds improve portfolio efficiency because they:

- Reduce volatility

- Improve diversification

- Stabilize returns

Efficient Frontier

The efficient frontier represents portfolios offering:

- Maximum expected return

- For a specific risk level

Bonds help optimize portfolio positioning.

Case Study: Balanced Investor

Investor

Michael, age 45, Canada

Portfolio

- 70% global stocks

- 25% government bonds

- 5% cash

During Market Decline

Stocks fall 30%.

Government bonds rise 8%.

Overall portfolio loss becomes much smaller than a stock-only portfolio.

Michael avoids panic selling and stays invested.

Bonds and Central Banks

Central banks strongly influence bond markets.

Examples include:

- Federal Reserve

- Bank of England

- Bank of Canada

- Reserve Bank of Australia

Their interest rate policies directly affect bond yields and prices.

Quantitative Easing and Bonds

After the 2008 crisis, central banks used quantitative easing (QE).

This involved:

- Buying government bonds

- Lowering long-term interest rates

- Supporting economic growth

QE significantly influenced global bond markets.

International Bonds

Investors can also buy foreign bonds.

Benefits:

- Geographic diversification

- Currency exposure

- Different interest rate cycles

Risks:

- Currency fluctuations

- Political risk

- Foreign economic instability

Municipal Bonds and Taxes

In the U.S., municipal bonds often provide tax-free income.

This is attractive for:

- High-income earners

- Wealth preservation strategies

Tax-equivalent yield becomes important when comparing investments.

Bond Allocation by Risk Profile

Conservative Investor

- 70% bonds

- 25% stocks

- 5% cash

Goal:

- Capital preservation

Moderate Investor

- 40% bonds

- 55% stocks

- 5% cash

Goal:

- Balanced growth and stability

Aggressive Investor

- 10% bonds

- 85% stocks

- 5% alternatives

Goal:

- Maximum long-term growth

Common Mistakes Investors Make with Bonds

1. Ignoring Inflation

Low yields may not beat inflation.

2. Chasing Yield

Higher yield often means higher risk.

3. Overconcentration

Owning too many long-term bonds can increase rate risk.

4. Not Diversifying

Holding only one bond issuer increases credit risk.

5. Panic Selling

Bond prices fluctuate too.

Investors should understand bond behavior before investing.

How Wealthy Investors Use Bonds

High-net-worth investors often use bonds for:

- Capital preservation

- Income generation

- Tax planning

- Risk balancing

- Liquidity management

Institutional investors frequently maintain significant bond allocations.

Pension Funds and Bonds

Pension funds rely heavily on bonds because they need:

- Stable income

- Predictable liabilities

- Lower volatility

Many pension systems in Tier-1 countries allocate large percentages to bonds.

Bonds During Economic Uncertainty

When uncertainty rises:

- Investors seek safety

- Demand for government bonds often increases

This phenomenon is called a flight to safety.

Are Bonds Still Relevant Today?

Some investors argue:

- Stocks outperform bonds long term

- Rising rates hurt bond prices

- Inflation reduces real returns

However, bonds remain relevant because they:

- Reduce risk

- Provide income

- Improve diversification

- Stabilize retirement portfolios

The role of bonds is not to outperform stocks.

The role is to create balance.

Example Portfolio Comparisons

Portfolio 1 — 100% Stocks

Expected:

- Higher growth

- Larger crashes

- Greater emotional stress

Portfolio 2 — 80/20

Expected:

- Strong growth

- Some stability

Portfolio 3 — 60/40

Expected:

- Balanced performance

- Moderate volatility

Portfolio 4 — 40/60

Expected:

- Lower growth

- Higher stability

- Stronger income focus

The Future of Bond Investing

Future bond investing may be influenced by:

- Higher interest rates

- Persistent inflation

- Aging populations

- Government debt levels

- Central bank policies

Technology and ETFs are also transforming access to bond markets.

Key Lessons About Bonds

Bonds Are Not Designed for Maximum Growth

Their primary purpose is:

- Stability

- Income

- Diversification

Bonds Help Investors Stay Invested

Reducing emotional panic can improve long-term outcomes.

Bonds Reduce Portfolio Risk

Balanced portfolios often experience smaller drawdowns.

Bonds Are Critical for Retirement Planning

Income and capital preservation become increasingly important with age.

Bond Allocation Depends on Personal Goals

There is no universal perfect allocation.

Factors include:

- Age

- Risk tolerance

- Income needs

- Time horizon

- Financial goals

Final Thoughts

Bonds are one of the foundational building blocks of intelligent portfolio construction. While they may appear less exciting than stocks, their role is incredibly important in managing risk, generating reliable income, protecting capital, and improving long-term investing discipline.

For investors in the United States, United Kingdom, Canada, and Australia, bonds remain essential components of retirement accounts, pension funds, balanced portfolios, and wealth preservation strategies.

A well-designed portfolio is not built solely for maximum returns. It is built for survivability across economic cycles, recessions, inflationary periods, market crashes, and changing financial conditions.

Stocks provide growth.

Bonds provide stability.

Together, they create balance — and balance is often the key to long-term investing success.