1️⃣ Introduction: Simplicity That Beats Complexity

The 3-Fund Portfolio Strategy is one of the simplest and most powerful ways to build long-term wealth. In a world of stock tips, crypto hype, YouTube gurus, and algorithmic trading systems, one investment strategy continues to quietly outperform most investors:

The 3-Fund Portfolio Strategy.

It is simple.

It is low-cost.

It is diversified.

It is evidence-based.

And it is widely recommended by researchers, fiduciary advisors, and institutions such as Vanguard Group.

The 3-Fund Portfolio Strategy does not attempt to predict markets.

It does not rely on stock picking skill.

It does not require daily monitoring.

Instead, it is built on three core pillars of global capitalism:

- U.S. Stocks

- International Stocks

- Bonds

Over decades, this approach has created millions of disciplined, quietly wealthy investors.

Today, we break down every term, every concept, every assumption, and examine real-world case studies to understand why this strategy works.

“Before you start investing, it’s important to manage your finances properly.

👉 Read our guide on How to Build an Emergency Fund Fast.”

2️⃣ What Is a 3-Fund Portfolio Strategy?

A 3-Fund Portfolio Strategy is an investment strategy that uses three broad, low-cost index funds to capture nearly the entire global investable market.

It typically consists of:

- A Total U.S. Stock Market Index Fund

- A Total International Stock Market Index Fund

- A Total Bond Market Index Fund

Let’s define these clearly.

Term: Portfolio

A portfolio is the collection of all investments owned by an individual or institution.

Example:

- 60% Stocks

- 40% Bonds

= That mix is your portfolio.

Term: Index Fund

An index fund is a fund that tracks (replicates) a market index.

An index is a basket of securities representing a segment of the market.

Example:

- S&P 500 tracks 500 large U.S. companies.

An index fund does not try to beat the market.

It tries to match the market.

Term: Total Market

A total market fund attempts to own almost every publicly traded company in that category.

Example:

A Total U.S. Market Fund owns:

- Large-cap stocks

- Mid-cap stocks

- Small-cap stocks

This gives you instant diversification.

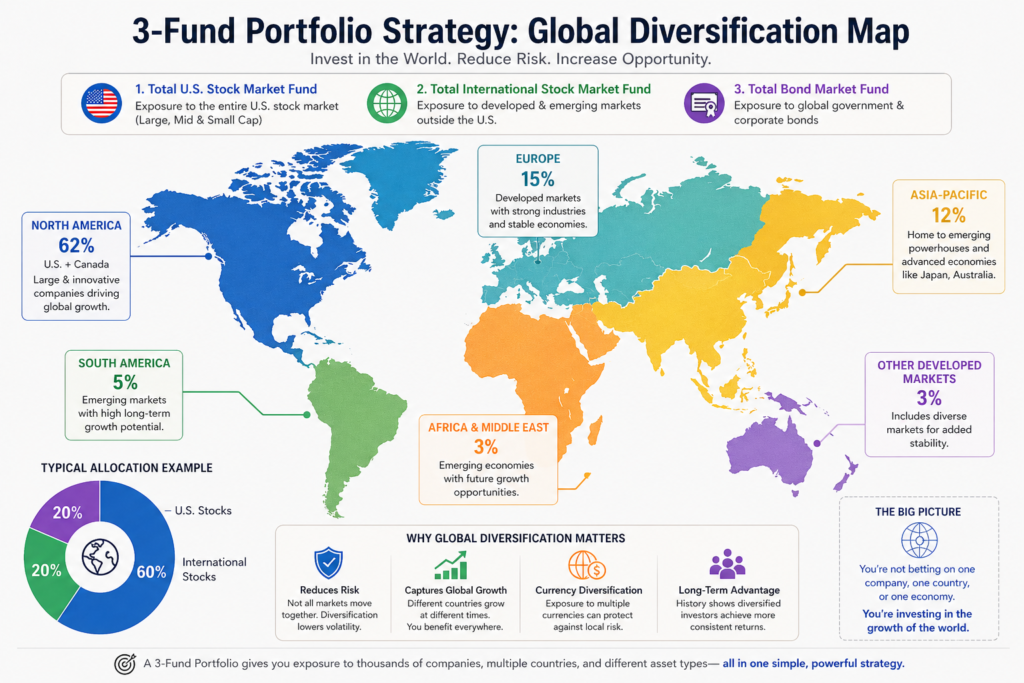

3️⃣ The Three Core Funds

1️⃣ Total U.S. Stock Market Fund

📌 What Is a Total U.S. Stock Market Fund?

A Total U.S. Stock Market Fund is an index fund that invests in almost every publicly traded company in the United States.

It includes large, mid, and small-cap companies, giving investors complete exposure to the U.S. equity market.

🏢 Examples of Companies Included

• Apple Inc.

One of the largest companies globally, Apple represents innovation and consumer technology growth.Its consistent revenue and global demand make it a major contributor to index performance.

• Microsoft Corporation

Microsoft dominates in software, cloud computing, and enterprise solutions.

It reflects long-term stability and recurring income within the U.S. market.

• Amazon.com, Inc.

Amazon showcases the power of e-commerce and digital infrastructure.

Its growth highlights how disruptive businesses drive market expansion.

📊 What It Provides

• Exposure to U.S. Economic Growth

Investing in this fund means your money grows alongside the U.S. economy.

As businesses expand and GDP rises, company earnings—and your returns—tend to increase.

• Corporate Profits

Companies generate profits through sales, and shareholders benefit from this growth.

Higher profits often lead to rising stock prices and dividends over time.

• Innovation

The U.S. market is a global leader in technology and innovation.

Breakthroughs in AI, software, and healthcare drive long-term stock performance.

• Productivity Growth

As companies become more efficient, they produce more with fewer resources.

This increased productivity boosts profits, which ultimately benefits investors.

📈 Historical Context

Over the past century, U.S. stocks have delivered an average return of about 9–10% annually before inflation.This long-term growth reflects economic expansion, innovation, and reinvested earnings.

💡 Why It Matters (Engine of Wealth)

The Total U.S. Stock Market Fund acts as the primary growth engine in a portfolio.

Over time, compounding returns from this fund play a major role in building long-term wealth.

2️⃣ Total International Stock Market Fund

📌 What Is a Total International Stock Market Fund?

A Total International Stock Market Fund invests in companies outside the United States, covering both developed and emerging markets. It gives investors exposure to global economies beyond a single country. This helps capture worldwide growth opportunities.

🌍 Global Company Exposure

These funds include major global companies such as:

- Toyota Motor Corporation

- Nestlé S.A.

- Samsung Electronics

By investing in such companies, you gain access to industries and innovations happening across different countries. This broad exposure reduces dependence on any one economy.

📊 Why This Matters

🔹 Protection Against U.S. Underperformance

If the U.S. stock market performs poorly for a long period, international markets may perform better. This balance helps stabilize your overall portfolio returns.

🔹 Real Example (2000–2010)

During this decade, U.S. markets delivered very low or near-zero returns. Meanwhile, international markets—especially emerging economies—performed better at certain times, helping diversified investors.

⚖️ Reduces Country-Specific Risk

Investing only in one country exposes you to its economic, political, and currency risks. International funds spread investments across multiple countries, reducing the impact of any single nation’s downturn.

3️⃣ Total Bond Market Fund

📌 What is a Bond ?

A bond is a type of investment where you lend money to an entity such as a government or corporation. In return, they promise to pay you regular interest and return your original amount after a fixed period.

🔹 How Bonds Work

1️⃣ You Lend Money

When you buy a bond, you are acting like a lender. Governments or companies use this money to fund projects, operations, or expansion.

2️⃣ You Receive Interest

The issuer pays you fixed interest (coupon payments) at regular intervals, such as annually or semi-annually. This provides a predictable income stream.

3️⃣ You Get Principal Back at Maturity

At the end of the bond’s term (called maturity), you receive your original investment amount back, making bonds relatively safer than stocks.

🔹 What Bonds Provide

1️⃣ Stability

Bonds are generally less volatile than stocks, meaning their prices don’t fluctuate as much. This helps stabilize your overall portfolio during uncertain market conditions.

2️⃣ Income

Bonds generate steady income through interest payments, making them ideal for retirees or investors seeking passive cash flow.

3️⃣ Lower Volatility

Compared to stocks, bonds experience smaller price swings. This reduces the emotional stress of investing and helps maintain long-term discipline.

4️⃣ Protection During Market Crashes

When stock markets fall, investors often move money into bonds, increasing their demand and stability. This makes bonds a protective asset in downturns.

📊 Real-World Example

🧠 During the 2008 Financial Crisis

- Stock markets around the world crashed significantly

- Many investors lost 30–50% of their portfolio value

- Bond investments, especially government bonds, remained stable or even gained value

👉 This shows how bonds act as a shock absorber in a diversified portfolio.

4️⃣ Why the 3-Fund Portfolio Strategy Uses Only Three Funds?

🔹 1. Nearly Every Public Company in the World

A 3-fund portfolio includes funds that track broad indexes like the S&P 500 and global markets, giving exposure to thousands of companies worldwide.Instead of relying on a few stocks, you participate in the growth of the entire global economy, reducing the risk of any single company failure.

🔹 2. Government and Corporate Bonds

The bond portion includes loans to governments (like U.S. Treasuries) and corporations, typically through total bond market funds.Bonds provide stability and regular income, helping balance stock market volatility and protect your portfolio during downturns.

🔹 3. Multiple Industries

Your portfolio automatically includes sectors like technology, healthcare, finance, energy, and consumer goods.If one industry underperforms (e.g., tech crash), others may perform well, ensuring your overall portfolio remains balanced.

🔹 4. Multiple Countries

Through international funds, you invest in economies across Europe, Asia, and emerging markets—not just one country. Economic growth varies globally. Diversifying across countries protects you from risks tied to a single nation’s economy.

🔹 5. Multiple Currencies

International investments expose you to currencies like the euro, yen, and others beyond your home currency. Currency diversification can protect your portfolio if your local currency weakens, adding another layer of risk management.

🚫 What You Are NOT Betting On

🔸 1. One CEO

You’re not dependent on the decisions of a single leader like Elon Musk or any individual executive. Even great leaders can make mistakes. Diversification ensures one bad decision doesn’t damage your entire portfolio.

🔸 2. One Sector

You’re not concentrating only on one industry like technology or real estate. Sector-specific crashes (like the dot-com bubble) can wipe out concentrated portfolios, but diversification protects you.

🔸 3. One Country

You’re not relying only on a single economy like the U.S. or India. If one country faces recession or political issues, your global exposure keeps your investments resilient.

🔸 4. One Trend

You’re not chasing short-term hype like AI stocks, crypto booms, or meme stocks. Trends come and go. A diversified strategy focuses on long-term growth rather than temporary excitement.

🌍 Final Perspective

🔹 Betting on Global Capitalism

You are investing in the collective growth of businesses, economies, and innovation worldwide. As long as businesses grow, innovate, and generate profits globally, your portfolio benefits—making this strategy one of the most reliable long-term wealth builders.

5️⃣ Core Concepts Behind the Strategy

🔶 Concept 1: Diversification

🔹 What is Diversification?

Diversification means spreading your investments across different assets to reduce overall risk. Instead of relying on one investment, you own many, so losses in one area can be offset by gains in another.

🔹 If One Company Fails, Others Succeed

When you invest in thousands of companies, the failure of one has minimal impact. Strong-performing companies help balance or even outweigh weak performers.

🔹 If One Country Slows, Another Grows

Different economies grow at different times. While one country may face recession, others may expand, helping stabilize your overall returns.

🔹 Types of Diversification in 3-Fund Portfolio Strategy

📌 Company Diversification

You invest in a large number of companies instead of a few, reducing the risk of individual business failure.

📌 Sector Diversification

Your portfolio includes industries like tech, healthcare, energy, and finance, so downturns in one sector don’t heavily impact you.

📌 Geographic Diversification

By investing globally, you reduce dependence on a single country’s economy and benefit from worldwide growth.

📌 Asset-Class Diversification

You combine stocks and bonds, balancing growth (stocks) with stability (bonds).

🔶 Concept 2: Asset Allocation

🔹 What is Asset Allocation?

Asset allocation is the percentage distribution of your investments between asset classes like stocks and bonds.

🔹 Example Allocation

A portfolio with 80% stocks and 20% bonds is growth-oriented, aiming for higher returns while maintaining some stability.

🔹 Why It Matters

Research by Brinson Partners shows that asset allocation drives most of a portfolio’s performance, more than stock picking.

🔹 Key Insight

Your stock-to-bond ratio has a bigger impact on long-term results than choosing “hot” or trending stocks.

🔶 Concept 3: Risk vs Return

🔹 Stocks: High Risk, High Return

Stocks tend to fluctuate more in the short term (volatility) but offer higher long-term returns due to business growth and innovation.

🔹 Bonds: Low Risk, Low Return

Bonds are more stable and provide fixed income, but their returns are generally lower compared to stocks.

🔹 Balancing Risk and Return

📌 Emotional Stability

A mix of stocks and bonds reduces large swings in portfolio value, helping investors stay calm during market downturns.

📌 Long-Term Growth

Proper balance ensures steady growth while managing risk, allowing you to stay invested and benefit from compounding over time.

6️⃣ Case Study: Two Investors

👤 Investor A – The Stock Picker

🔹 Owns 15 Tech Stocks

Investor A concentrates money in a single sector—technology—buying a limited number of companies like Apple Inc. or Tesla, Inc.. Lack of diversification means if the tech sector crashes, the entire portfolio suffers significant losses.

🔹 Trades Frequently

He buys and sells stocks regularly, trying to time the market based on news, trends, or predictions. Frequent trading increases transaction costs and often leads to poor timing decisions, reducing overall returns.

🔹 Pays High Fees

Active trading, brokerage charges, and possibly advisory fees increase the cost of investing. Even small fees (1–2%) can significantly reduce wealth over 20 years due to lost compounding.

🔹 Panics During Downturns

When markets fall, Investor A sells investments out of fear instead of staying invested. Selling during crashes locks in losses and prevents recovery gains when markets bounce back.

📉 Result Over 20 Years: Underperforms Market Average

Explanation:

Due to poor diversification, emotional decisions, and high costs, Investor A earns less than the overall market return.

👤 Investor B – The 3-Fund Investor

🔹 60% U.S. Stocks

A major portion is invested in the U.S. market through broad indexes like the S&P 500.This captures long-term growth of strong, innovative companies across multiple industries.

🔹 20% International Stocks

Investor B invests in global markets outside the U.S., including Europe and Asia.This provides geographic diversification, reducing dependence on a single country’s economy.

🔹 20% Bonds

A portion is allocated to bonds, which are safer, income-generating investments.Bonds reduce volatility and provide stability during stock market downturns.

🔹 Rebalances Annually

Investor B adjusts the portfolio once a year to maintain the original allocation (60/20/20).This enforces disciplined investing—selling high and buying low automatically.

🔹 Invests Monthly

He invests a fixed amount regularly, regardless of market conditions.This strategy (called dollar-cost averaging) reduces timing risk and builds consistency.

📈 Result Over 20 Years: Matches Market Performance with Minimal Stress

By staying diversified, low-cost, and disciplined, Investor B captures overall market returns without emotional stress or complex decisions.

⚖️ Final Comparison Insight

- Investor A relies on prediction and emotion

- Investor B relies on system and discipline

👉 Over time, systems consistently outperform speculation.

7️⃣ The Power of Rebalancing

🔹 What Is Rebalancing?

Definition:

Rebalancing means adjusting your portfolio back to its original asset allocation after market movements change the percentages.

Over time, some investments grow faster than others. Rebalancing keeps your risk level consistent and aligned with your long-term plan.

📊 Example Breakdown

🔹 Target Allocation: 60% Stocks / 40% Bonds

You initially decide to invest 60% in stocks (growth assets) and 40% in bonds (stable assets). This balance is chosen based on your risk tolerance—stocks for higher returns, bonds for stability.

🔹 After a Stock Rally: 70% Stocks / 30% Bonds

Stocks perform well and increase in value, automatically taking up a larger portion of your portfolio. Your portfolio becomes riskier than intended because stocks are more volatile than bonds.

🔹 Action: Sell Stocks and Buy Bonds

You sell some stock investments and use that money to purchase bonds. This restores your original 60/40 allocation and brings your portfolio back to the desired risk level.

🔄 The Core Principle Behind Rebalancing

🔹 Sell High

You sell assets (stocks) after they have increased in value. This locks in profits instead of letting gains disappear during future market corrections.

🔹 Buy Low

You buy assets (bonds, in this case) that have relatively underperformed or grown slower. You accumulate more units at a lower relative price, positioning for future stability or growth.

⚖️ Final Insight

Rebalancing is not about predicting the market—it’s about maintaining discipline. By following a fixed strategy, you:

- Control risk

- Avoid emotional decisions

- Systematically apply “buy low, sell high”

This is one of the simplest yet most powerful habits in long-term investing.

8️⃣ Real Historical Example

🔹 What Is the “Lost Decade” (2000–2010)?

Definition:

The period from 2000 to 2010 is often called the “lost decade” for U.S. investors because stock market returns were extremely low or near zero.

It shows that even strong markets like the U.S. can go through long periods of stagnation, highlighting the importance of diversification.

📊 Performance Breakdown (2000–2010)

🔹 U.S. Stocks ≈ Flat

Major indexes like the S&P 500 delivered little to no overall growth during this 10-year period. Events like the dot-com crash (2000) and the 2008 financial crisis significantly impacted returns.

🔹 International Stocks Positive at Times

Markets outside the U.S., including Europe and emerging economies, experienced periods of growth during the same decade.While the U.S. struggled, global diversification allowed investors to benefit from growth in other regions.

🔹 Bonds Showed Steady Growth

Bond investments provided consistent returns and income throughout the decade. Bonds acted as a stabilizer, especially during stock market crashes, protecting overall portfolio value.

⚖️ Final Outcome Comparison

🔹 Diversified 3-Fund Portfolio Strategy Performance

A portfolio combining U.S. stocks, international stocks, and bonds continued to grow modestly during this period. Losses in U.S. stocks were offset by gains in international markets and stability from bonds.

🔹 Pure U.S. Portfolio Performance

Investors who only held U.S. stocks saw little to no progress over 10 years. Lack of diversification meant they were fully exposed to U.S.-specific downturns.

📌 Key Insight

A single market can stagnate for years—but global diversification ensures your money continues working.

👉 The 3-fund strategy protects you not by avoiding downturns, but by not depending on one market alone.

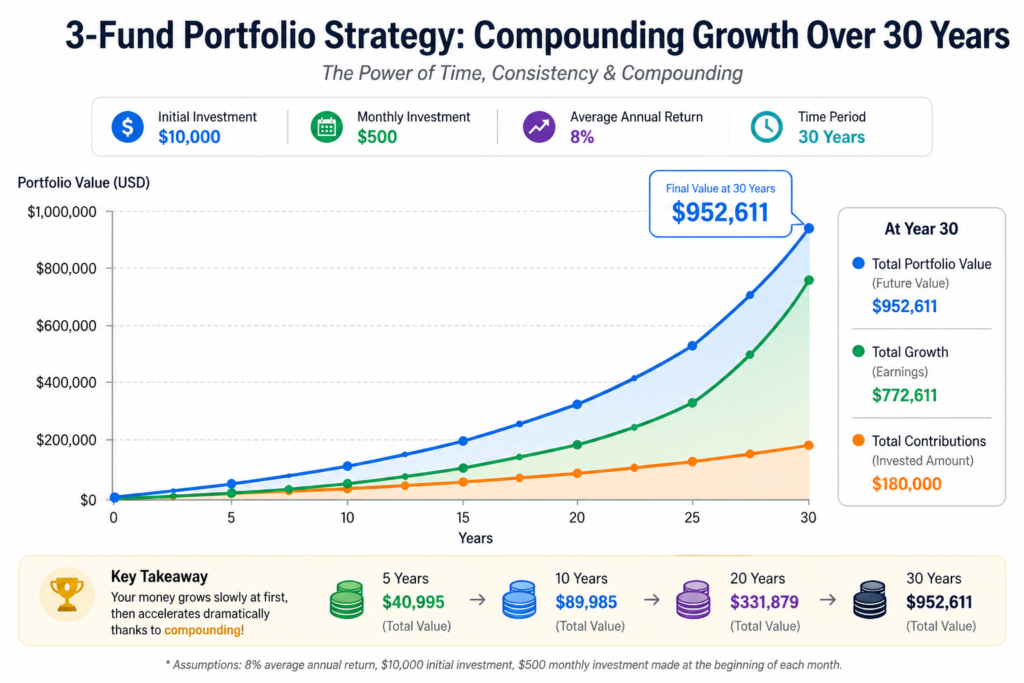

9️⃣ 3-Fund Portfolio Strategy: Long-Term Compounding Example

📊 Investment Scenario Breakdown

🔹 Initial Investment: $10,000

You start with a one-time investment of $10,000 in a diversified portfolio. This initial amount becomes the foundation on which compounding builds wealth over time.

🔹 Return: 8% Annually

Your investment grows at an average annual return of 8%, which is typical for a balanced stock-heavy portfolio over the long term. Consistent returns—even if not guaranteed every year—are the key driver of long-term wealth creation.

🔹 Time: 30 Years

You stay invested for three decades without withdrawing money or interrupting the growth. Time is the most powerful factor in compounding—the longer you stay invested, the faster your money grows.

🔹 Final Value ≈ $100,000+

Your original $10,000 grows nearly 10 times due to continuous compounding over 30 years. This demonstrates how patience and consistency can turn small investments into significant wealth.

🔁 Understanding Compounding

🔹 Compounding = Interest on Interest

You earn returns not only on your original investment but also on the returns generated each year. This creates exponential growth, where your wealth accelerates faster over time instead of growing linearly.

⚙️ Why the 3-Fund Strategy Enhances Compounding

🔹 Low Fees

Index funds typically charge very small expense ratios compared to actively managed funds. Lower fees mean more of your returns stay invested and continue compounding over time.

🔹 Broad Exposure

You invest across thousands of companies and global markets instead of a few selected stocks.

This ensures consistent participation in overall market growth, reducing the risk of missing long-term gains.

🔹 Minimal Turnover

The portfolio requires very little buying and selling, often only during periodic rebalancing. Less trading reduces costs, taxes, and mistakes—allowing compounding to work uninterrupted.

📌 Final Insight

Compounding is not about quick profits—it’s about time, discipline, and consistency.

👉 The 3-fund strategy creates the perfect environment for compounding by minimizing friction and maximizing long-term growth.

🔟 Expense Ratios (Critical Factor)

🔹 What Is an Expense Ratio?

Definition:

An expense ratio is the annual fee charged by a mutual fund or ETF to manage your investment, expressed as a percentage of your total investment.

This fee is automatically deducted from your returns, meaning you don’t see it directly—but it continuously reduces your overall wealth.

🔹 Example: 0.03% vs 1%

A fund with a 0.03% expense ratio charges ₹30 per year on ₹1,00,000 invested, while a 1% fund charges ₹1,000 on the same amount. The difference looks small yearly, but over decades, it creates a massive gap in final returns due to compounding.

🔹 Impact Over 30 Years

Higher fees reduce the amount of money that stays invested and compounds over time. Even a 1% higher fee can cost you lakhs or even crores over 30 years, especially with large investments.

🔹 Low-Cost Investment Providers

Companies like Vanguard Group and Fidelity Investments offer index funds with very low expense ratios. Lower fees allow more of your money to remain invested, maximizing long-term compounding and overall returns.

📌 Final Insight

Expense ratios may seem small, but they are one of the most powerful hidden factors in investing.

👉 The less you pay in fees, the more you keep—and over time, that difference becomes enormous.

11️⃣ Sample Allocation Models

👶 Age 25 (Aggressive Allocation)

🔹 70% U.S. Stocks

A large portion is invested in U.S. companies through broad indexes like the S&P 500. At a young age, you have time to handle market volatility, so higher stock exposure maximizes long-term growth potential.

🔹 20% International Stocks

You invest in global markets outside the U.S., including developed and emerging economies. This adds diversification and allows you to benefit from growth opportunities worldwide.

🔹 10% Bonds

A small portion is allocated to safer, income-generating assets like bonds. Even aggressive investors need some stability to reduce extreme volatility during market downturns.

👨💼 Age 45 (Moderate Allocation)

🔹 50% U.S. Stocks

A balanced allocation still favors growth through U.S. equities. You continue building wealth but start reducing risk compared to a younger investor.

🔹 20% International Stocks

Global exposure remains constant to maintain diversification. It protects against country-specific risks and ensures participation in worldwide economic growth.

🔹 30% Bonds

A higher portion is invested in bonds compared to earlier years. As retirement approaches, stability becomes more important, and bonds help protect accumulated wealth.

👴 Age 65 (Conservative Allocation)

🔹 30% U.S. Stocks

A smaller portion remains in equities to provide some growth.

Even in retirement, you need growth to beat inflation and sustain long-term expenses.

🔹 20% International Stocks

You maintain global diversification even at a conservative stage. This ensures your portfolio is not overly dependent on one country’s economy.

🔹 50% Bonds

Half of the portfolio is invested in bonds for safety and income. At this stage, preserving capital and generating stable income becomes the top priority.

📌 Final Insight

Asset allocation evolves with age:

- Young investors focus on growth

- Mid-age investors balance growth + safety

- Older investors prioritize capital preservation + income

👉 The goal is not maximum return at all times, but the right return for your life stage and risk tolerance.

12️⃣ Why It Beats Most Active Investors

🔹 What Do Studies Show?

Long-term research shows that most actively managed funds fail to beat their benchmark index, such as the S&P 500. Even professional fund managers struggle to consistently outperform the market after accounting for costs and risks.

📉 Reasons Active Investors Underperform

🔹 Higher Fees

Active funds charge higher management fees compared to low-cost index funds. These fees reduce your net returns every year, significantly impacting long-term compounding.

🔹 Trading Costs

Frequent buying and selling leads to brokerage fees, bid-ask spreads, and hidden costs. These costs add up over time, quietly reducing the overall performance of the portfolio.

🔹 Tax Inefficiency

Frequent trading generates short-term capital gains, which are often taxed at higher rates. Higher taxes mean less money stays invested, slowing down long-term wealth growth.

🔹 Human Emotion

Investors often make decisions based on fear, greed, or market noise. Emotional decisions lead to buying high and selling low—the opposite of successful investing.

✅ Why the 3-Fund Investor Wins

🔹 Avoids High Fees

Uses low-cost index funds instead of expensive actively managed funds. More money stays invested and compounds over time.

🔹 Minimizes Trading

Only occasional rebalancing is needed instead of constant buying and selling. Lower costs and fewer mistakes improve long-term returns.

🔹 Improves Tax Efficiency

Low turnover results in fewer taxable events. More capital remains invested, boosting compounding.

🔹 Removes Emotional Decisions

Follows a fixed strategy instead of reacting to market movements. Consistency leads to better long-term performance.

📌 Final Insight

Active investing sounds attractive, but data tells a different story.

👉 The 3-fund strategy wins not because it is complex, but because it eliminates the common mistakes that reduce returns.

13️⃣ Psychological Advantage

🔹 Why Simplicity Matters

A simple portfolio like the 3-fund strategy removes complexity and constant decision-making. Less complexity means fewer mistakes, better consistency, and stronger long-term investing behavior.

❌ What Simplicity Reduces

🔹 Overtrading

Constant buying and selling in response to market movements or short-term opportunities. Overtrading increases costs and often leads to poor decisions, reducing overall returns.

🔹 News Obsession

Continuously following financial news, market predictions, and daily price movements. Too much information creates confusion and can lead to unnecessary changes in your investment strategy.

🔹 Market Timing

Trying to predict when to enter or exit the market to maximize profits. Even professionals struggle with timing, and missing just a few best days can significantly reduce returns.

🔹 Fear-Based Decisions

Selling investments during market crashes due to panic or uncertainty. This locks in losses and prevents you from benefiting when markets recover.

✅ What Simplicity Encourages

🔹 Discipline

Following a fixed investment plan regardless of market conditions. Discipline ensures consistency, which is essential for long-term success.

🔹 Patience

Staying invested for years or decades without reacting to short-term fluctuations. Wealth is built over time, and patience allows compounding to work effectively.

🔹 Long-Term Thinking

Focusing on future goals rather than short-term market movements.

Long-term investors are more likely to capture overall market growth and avoid emotional mistakes.

📌 Final Insight

Investing success is not just about strategy—it’s about behavior.

👉 A simple system like the 3-fund portfolio helps you stay calm, consistent, and focused, which is where real wealth is built.

14️⃣ When the Strategy Underperforms

🔹 Understanding Underperformance

Even a well-diversified strategy like the 3-fund portfolio will have periods where it does not deliver the highest returns compared to specific markets.

No strategy wins all the time. Accepting temporary underperformance is essential for long-term success.

📉 Situations Where It May Underperform

🔹 U.S. Dominates and International Lags

There are periods when U.S. markets outperform global markets, such as strong performance in indexes like the S&P 500.

Since part of your portfolio is invested internationally, overall returns may be slightly lower than a U.S.-only portfolio during such times.

🔹 Bonds Underperform Stocks

In strong bull markets, stocks generate much higher returns than bonds.

Holding bonds reduces total returns in these periods, but they are included for stability and risk control.

🔹 One Region Crashes

A specific country or region (e.g., Europe, emerging markets) may face economic or political crises.

Your international allocation may decline temporarily, pulling down overall portfolio performance.

⚖️ The Core Philosophy

🔹 Not About Winning Every Year

Diversification ensures you won’t always be the top performer in any given year.

Trying to always win leads to risky decisions and poor long-term outcomes.

🔹 About Surviving Every Decade

The goal is to remain stable and grow steadily across all market conditions over long periods.

Consistent survival and participation in the market lead to compounding and long-term wealth creation.

📌 Final Insight

Short-term underperformance is the price you pay for long-term stability.

👉 Diversification may limit extreme gains—but it protects you from extreme losses, which is far more important for building wealth.

15️⃣ 30-Year Case Simulation

🔹 Overview of the Scenario

This example shows how regular investing over a long period can build significant wealth using disciplined strategy.

It highlights the power of consistency and compounding rather than relying on large one-time investments.

📊 Investment Breakdown

🔹 $500/Month Investment

You invest a fixed amount of $500 every month, regardless of market conditions.

This approach (systematic investing) builds discipline and reduces the risk of poor market timing.

🔹 8% Average Return

Your portfolio grows at an average annual return of 8%, typical of a diversified stock-heavy portfolio.

Even though returns fluctuate yearly, a steady long-term average creates strong compounding growth.

🔹 30 Years Investment Period

You stay invested continuously for three decades without withdrawing funds.

Time allows compounding to accelerate, turning small contributions into large wealth.

💰 Final Results

🔹 Total Invested: $180,000

Over 30 years, you contribute $500/month, totaling $180,000 from your own pocket.

This shows that consistent small investments can accumulate into a meaningful base amount.

🔹 Estimated Value: $750,000+

Due to compounding, your portfolio grows to more than four times your invested amount.

This demonstrates how returns—not just contributions—drive long-term wealth creation.

🔁 The Real Power Behind Growth

🔹 Compounding vs Contributions

A large portion of the final value comes from returns generated on previous returns, not just your monthly investments.

Over time, compounding becomes the dominant force, making early and consistent investing extremely powerful.

📌 Final Insight

Wealth is not built by investing large amounts once—it’s built by investing consistently over time.

👉 The longer you stay invested, the more compounding works in your favor, turning small monthly amounts into substantial wealth.

16️⃣ Common Mistakes

🔹 Why Avoiding Mistakes Matters

Investment success is often less about picking the “best” assets and more about avoiding costly behavioral and strategic errors.

Even a strong strategy like the 3-fund portfolio can fail if these common mistakes are repeated over time.

❌ Common Mistakes Investors Make

🔹 Adding Too Many Funds

Investors keep adding multiple funds, thinking more funds = better diversification.

This creates overlap, complexity, and confusion without adding real benefit—reducing the simplicity advantage of the 3-fund strategy.

🔹 Chasing Performance

Buying funds or stocks that have recently performed well, expecting the trend to continue.

Markets are cyclical, and this behavior often leads to buying high and selling low.

🔹 Changing Allocation Frequently

Regularly adjusting your stock/bond ratio based on market news or predictions.

Frequent changes disrupt long-term planning and often lead to inconsistent and poor results.

🔹 Ignoring Bonds Entirely

Some investors avoid bonds completely to maximize stock returns.

Without bonds, portfolios become highly volatile, increasing the risk of panic selling during downturns.

🔹 Panic Selling

Selling investments during market crashes due to fear or uncertainty.

This locks in losses and prevents participation in market recovery, damaging long-term returns.

✅ The Core Strength of the Strategy

🔹 Consistency Is the Real Power

The 3-fund strategy works best when followed consistently over time without emotional interference.

Discipline and patience allow compounding and diversification to deliver reliable long-term results.

📌 Final Insight

Most investors don’t fail because of bad investments—they fail because of bad decisions.

👉 Avoiding these simple mistakes is often enough to outperform the majority of investors.

17️⃣ Who Should Use This Strategy?

🔹 Beginners

People who are new to investing and don’t have deep knowledge of stock picking or market analysis.

The 3-fund strategy is simple, low-risk, and easy to manage, making it perfect for building a strong foundation.

🔹 Busy Professionals

Individuals with demanding careers who don’t have time to monitor markets daily.

This strategy requires minimal effort—just periodic investing and occasional rebalancing.

🔹 Long-Term Retirement Investors

People saving for retirement over decades rather than short-term goals.

It focuses on steady growth, compounding, and risk management—key factors for retirement planning.

🔹 FIRE Community

Investors following the Financial Independence, Retire Early (FIRE) approach.

Low costs, disciplined investing, and long-term compounding align perfectly with FIRE goals.

🔹 People Who Value Simplicity

Investors who prefer a straightforward, easy-to-understand investment approach.

The 3-fund portfolio eliminates complexity while still delivering strong, diversified returns.

18️⃣ Who Should NOT Use This Strategy?

🔹 Day Traders

Investors who buy and sell assets frequently within short timeframes to profit from price movements.

The 3-fund strategy is designed for long-term investing, not rapid trading or short-term gains.

🔹 Speculators

Individuals who take high risks hoping for quick, large profits based on predictions or trends.

This strategy focuses on stability and consistency, not high-risk, high-reward speculation.

🔹 Crypto-Focused Traders

Investors primarily focused on cryptocurrencies and highly volatile digital assets.

The 3-fund approach is based on traditional markets (stocks and bonds), not speculative digital assets.

🔹 Investors Seeking Short-Term Gains

People aiming to make profits within months or a few years.

The strategy relies on long-term compounding and may not deliver quick returns in the short run.

19️⃣ Final Case Study: 25-Year Retirement Plan

🔹 Starting Age: 30

You begin investing at age 30, giving yourself a long time horizon before retirement.

Starting early allows compounding to work longer, significantly increasing your final wealth.

🔹 Invest $600/Month

You consistently invest $600 every month into your portfolio.

Regular contributions build discipline and take advantage of market fluctuations through systematic investing.

🔹 Average Return: 7.5%

Your investments grow at an average annual return of 7.5%, typical of a balanced portfolio.

Even moderate returns can generate large wealth over time when combined with consistency and compounding.

🔹 Retire at 60

You stay invested for 30 years, from age 30 to 60.

A long investment period allows your money to grow exponentially rather than linearly.

💰 Final Outcome

🔹 Estimated Value: ~$900,000+

By retirement, your portfolio grows close to $900,000 through consistent investing and compounding.

This shows how disciplined investing can create substantial wealth without needing large initial capital.

🔹 Add Employer Match → Likely Crosses $1M

If your employer contributes to your retirement plan (like matching contributions), your total investment increases.

Employer match acts like “free money,” significantly boosting your final retirement value beyond $1 million.

⚙️ Key Advantages of This Approach

🔹 Without Stock Picking

You don’t need to select individual stocks or predict which companies will perform best. Broad market investing ensures you capture overall economic growth without added risk.

🔹 Without Market Timing

You don’t try to predict market highs and lows. Avoiding timing mistakes ensures you stay invested and benefit from long-term market trends.

🔹 Without Stress

The strategy is simple, automated, and requires minimal decision-making. Less emotional involvement leads to better consistency and improved long-term results.

This case study proves that wealth is built through time, consistency, and discipline—not complexity.

👉 You don’t need to be an expert—you just need to start early and stay invested.

20️⃣ Final Thoughts: Why the 3-Fund Portfolio Strategy Works Long-Term

The 3-Fund Portfolio Strategy works because it:

- Captures global growth

- Minimizes costs

- Controls risk

- Simplifies decisions

- Maximizes compounding

It is not exciting.

It is not trendy.

It is not viral.

It is disciplined.

And discipline, not brilliance, builds wealth.