1. Introduction: The Silent Thief in Your Bank Account

How inflation destroys savings is something most people don’t fully understand — until it’s too late.

Inflation doesn’t knock on your door or send you a warning, but it quietly reduces the value of your money every single year.

Even if your bank balance is growing, your purchasing power may be shrinking. This is why millions of people in Tier-1 countries feel financially stuck despite saving consistently.

Inflation doesn’t kick down your door. It doesn’t send you a bill. It doesn’t make headlines every day. Yet, quietly, relentlessly, and legally, it drains the value of your hard-earned savings.

You can work overtime, skip vacations, and save diligently — but if your money is sitting still, inflation is actively shrinking its purchasing power. This is why people in Tier-1 countries often feel like they’re running faster but getting nowhere financially.

In 2000, $100 could fill a grocery cart. Today, that same $100 barely covers a few bags. The money didn’t disappear — its value did.

This article will show you:

- Exactly how inflation destroys your savings

- Why traditional saving strategies no longer work

- How to protect and grow your wealth in an inflationary world

- How to turn inflation from an enemy into a financial advantage

2. What Is Inflation and How It Destroys Savings?

Inflation is the gradual increase in the price of goods and services over time — which means each unit of currency buys less than it used to.

In simple terms:

Inflation = Declining purchasing power of money.

If inflation is 5% per year, something that costs $100 today will cost $105 next year — even if the product itself hasn’t changed.

Example:

- In 2010, a cup of coffee cost $2.

- In 2026, the same coffee costs $4.

- Your money didn’t double — the price did.

This is why inflation is often called a “hidden tax.” You’re paying more, even though your income may not rise at the same rate.

3. Why Inflation Hurts Savers More Than Spenders

It may sound counterintuitive, but inflation punishes savers — not spenders.

Here’s why:

- Savers hold cash, which loses value over time.

- Spenders buy assets (homes, businesses, stocks) that often rise with inflation.

If you keep money in a low-interest savings account, inflation is eating away at it daily. Meanwhile, someone who invests or owns assets often sees their wealth grow as prices rise.

This creates a dangerous illusion:

“I’m being responsible by saving, but I feel poorer every year.”

That’s inflation at work.

4. The Real Cost of Inflation: What the Numbers Actually Mean

Let’s look at the math — because inflation’s real damage becomes obvious when you quantify it. Understanding how inflation destroys savings becomes much clearer when you see the numbers over time.

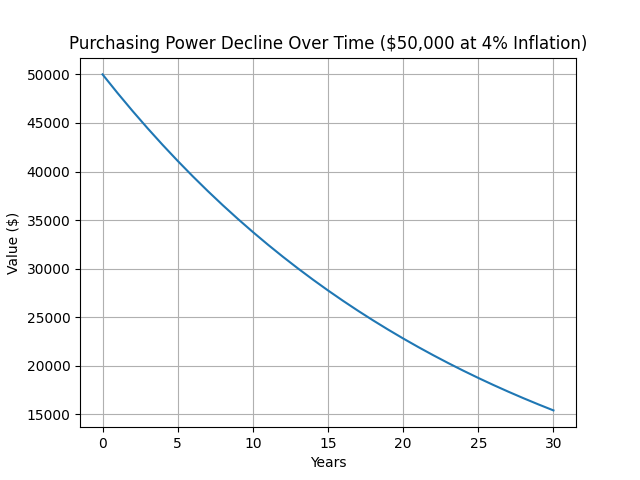

Example: 4% Inflation

If you save $50,000 in cash and inflation averages 4% per year, your money may look the same — but its purchasing power steadily declines.

Purchasing Power Decline Chart

This chart demonstrates how inflation destroys savings over time.

Even at a moderate 4% inflation rate, the purchasing power of $50,000 drops by nearly 70% over 30 years, making long-term cash savings extremely risky.

📉 Purchasing Power Over Time

| Year | Purchasing Power ($) |

|---|---|

| 0 | 50,000 |

| 5 | 41,100 |

| 10 | 33,800 |

| 15 | 27,800 |

| 20 | 22,800 |

| 25 | 18,700 |

| 30 | 15,400 |

🔎 What This Means in Real Terms

- After 10 years → Your $50,000 feels like $33,800

- After 20 years → It drops to $22,800

- After 30 years → It’s worth only ~$15,400

👉 This clearly shows:

$50,000 → ~$15,400 (nearly 70% loss in purchasing power)

⚠️ Why This Matters

This is exactly how inflation destroys savings over time.

Even though your bank balance still shows $50,000, what that money can actually buy has dropped dramatically. Groceries, housing, healthcare, and everyday expenses become more expensive — while your money stays the same.

You didn’t lose the money — but you lost 70% of its real value.

📉 Real-World Impact

This silent erosion has serious long-term consequences:

- Retirement goals become harder to achieve

- Emergency funds lose effectiveness

- Long-term savings fall short of expectations

- Financial independence gets delayed by years (or decades)

💡 Key Takeaway

If your money isn’t growing faster than inflation, you’re effectively losing wealth every year.

That’s why understanding how inflation destroys savings is not just important — it’s essential for building a secure financial future.

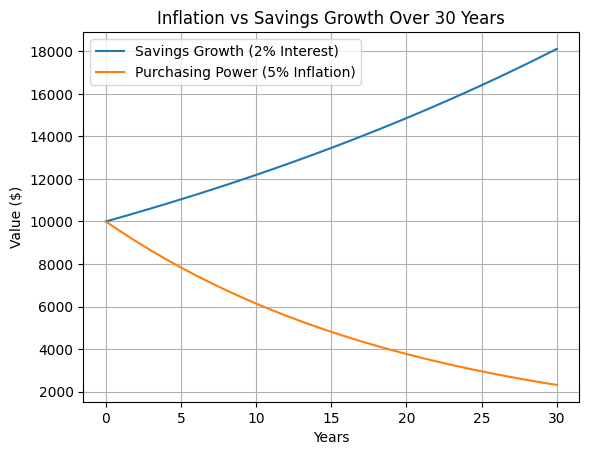

5. How Inflation Destroys Savings Over Time

This chart clearly shows how inflation destroys savings over time. Even though your savings grow slowly, inflation rises faster — reducing your real purchasing power year after year.

Cash is the most vulnerable asset in an inflationary world.

Why?

Because:

- Cash earns little to no return.

- Inflation compounds against it.

Example:

You save $10,000 and leave it in a 1% savings account while inflation runs at 5%.

Your real return:

1% interest – 5% inflation = –4% real return

You’re losing 4% per year in purchasing power — guaranteed.

This is why holding excessive cash long-term is one of the biggest wealth destroyers.

6. Why Inflation Destroys Savings Faster Than Interest Rates Grow

Banks advertise interest rates as if they’re helping you grow your money — but they rarely keep up with inflation.

In most Tier-1 countries:

- Average savings account yield: 1%–4%

- Average inflation rate (2020–2025): 3%–8%

Unless your interest rate exceeds inflation, your money is shrinking.

This creates what economists call a negative real interest rate environment, where savers are effectively punished for being conservative.

7. The Psychological Trap: Why People Ignore Inflation

Humans are wired to think in nominal terms (dollars, pounds, euros), not real terms (purchasing power).

So people think:

- “My savings are growing.”

- “My salary increased.”

- “My bank balance is higher.”

But what really matters is:

“What can this money buy?”

Inflation is invisible because:

- It’s slow.

- It’s gradual.

- It feels normal.

This cognitive blind spot leads people to underestimate inflation’s long-term damage — until it’s too late.

8. How Inflation Affects Different Asset Classes

Not all assets respond to inflation the same way. Some suffer, some survive, and some thrive.

Assets That Suffer:

- Cash

- Fixed-rate bonds

- Long-term savings accounts

Assets That Survive:

- Short-term bonds

- High-yield savings

- Floating-rate debt

Assets That Thrive:

- Stocks

- Real estate

- Commodities

- Businesses

- Inflation-linked bonds

Understanding this is the foundation of building an inflation-resistant portfolio.

9. Inflation’s Impact on Retirees and Fixed-Income Earners

Retirees are among the most vulnerable to inflation because:

- Their income is often fixed.

- They rely on savings.

- They may not be able to increase earnings.

Example:

A retiree living on $40,000 per year:

- At 3% inflation → needs $72,000 in 20 years to maintain the same lifestyle.

- At 6% inflation → needs $128,000.

Without inflation-adjusted income streams, retirees face declining living standards — even if they “saved enough.”

10. Inflation in Tier-1 Countries: What’s Different Today

Inflation dynamics in Tier-1 countries (USA, UK, Canada, Australia, Western Europe) are shaped by:

- Aging populations

- Rising healthcare costs

- Housing shortages

- Supply chain fragility

- Massive government debt

- Central bank stimulus

The post-2020 world introduced:

- Persistent inflation rather than temporary spikes

- Structural cost pressures

- Less predictable monetary policy

This means inflation is no longer a short-term anomaly — it’s a long-term reality.

11. The Hidden Inflation Tax

Inflation acts like a tax — but without legislation or public debate.

Instead of taxing your income, it taxes your purchasing power.

If inflation is 5%:

- Your money is taxed 5% every year — even if your salary doesn’t rise.

- Governments benefit because their debts shrink in real terms.

- Savers and wage earners pay the price.

This is why inflation is sometimes called “the most regressive tax” — it hurts low and middle-income households the most.

12. How Governments Measure Inflation (And Why It Often Feels Wrong)

Most countries use Consumer Price Index (CPI) or similar measures.

But people often feel inflation is higher than official numbers because:

- CPI uses averages, not your personal spending.

- Housing, education, healthcare, and childcare costs often rise faster than CPI.

- Substitution bias (replacing steak with chicken) masks real lifestyle decline.

So while official inflation might say 3%, your personal inflation could be 7% or higher.

13. Inflation-Proofing Your Savings: The Core Principles

You should always maintain a safety buffer.

👉 Learn: How to Build an Emergency Fund Fast to protect against financial shocks.Before choosing specific investments, understand these core principles:

- Money must grow faster than inflation.

- Assets beat cash over time.

- Diversification protects against inflation shocks.

- Income streams must rise with the cost of living.

- Debt can be an asset if structured correctly.

With these principles, we can build a strategy that not only protects — but grows — your wealth.

14. High-Yield Savings Accounts: First Line of Defense

While cash loses value, you still need liquidity for emergencies.

Solution: High-yield savings accounts (HYSAs).

These offer:

- Higher interest than traditional banks

- FDIC or government insurance

- Easy access

They won’t beat inflation — but they reduce the damage.

Think of HYSAs as:

A shield, not a sword.

15. Treasury Inflation-Protected Securities (TIPS) and Index-Linked Bonds

TIPS (U.S.), Index-Linked Gilts (UK), and similar instruments in Canada and Europe adjust their principal based on inflation.

This means:

- Your investment grows with inflation.

- Interest payments rise as prices rise.

- Your purchasing power is preserved.

These are ideal for:

- Retirees

- Conservative investors

- Fixed-income allocation

They won’t make you rich — but they protect you from being quietly robbed.

16. Stocks as an Inflation Hedge

Stocks represent ownership in businesses — and businesses can raise prices.

Historically:

- Stocks outperform inflation over long periods.

- Companies pass higher costs to consumers.

- Earnings and dividends rise with inflation.

However:

- Short-term volatility increases during inflationary periods.

- Not all sectors perform equally.

Best-performing sectors during inflation:

- Energy

- Consumer staples

- Financials

- Real estate

- Healthcare

Long-term equity investing remains the most powerful inflation defense.

17. Real Estate and Rental Income in Inflationary Periods

Real estate is one of the strongest inflation hedges because:

- Property values rise with inflation.

- Rents increase over time.

- Mortgage payments (fixed-rate) stay the same.

This creates a powerful dynamic:

Your income rises, but your debt stays fixed — meaning inflation works for you.

This is why real estate has created more millionaires than almost any other asset class.

18. Commodities and Gold: Do They Really Protect Against Inflation?

Commodities — especially gold — are often seen as inflation hedges.

Gold:

- Preserves value over centuries.

- Performs well during currency debasement.

- Does not produce income.

Commodities:

- Rise when raw material prices increase.

- Highly volatile.

- Cyclical.

These assets are best used as:

A diversification hedge, not a primary wealth builder.

19. The Role of Cash: How Much Should You Actually Hold?

You should hold:

- 3–6 months of expenses in emergency savings.

- Short-term funds for known expenses.

- No more than necessary.

Beyond that:

- Cash becomes a liability.

- Idle money = guaranteed loss.

Cash is a tool, not a long-term investment.

20. Smart Debt: Using Inflation to Your Advantage

Inflation hurts savers — but it helps borrowers.

Why?

- You repay debt with future dollars that are worth less.

- Fixed-rate debt becomes cheaper over time.

Example:

- A 30-year fixed mortgage at 4%.

- Inflation averages 5%.

- Your real interest rate is –1%.

Smart debt:

- Fixed-rate

- Long-term

- Invested into appreciating or income-producing assets

This is how the wealthy use leverage — safely and strategically.

21. Salary Negotiation in an Inflationary Economy

If your income doesn’t rise faster than inflation, you’re getting a pay cut — even if your salary increases.

Example:

- Your raise: 3%

- Inflation: 5%

- Real income change: –2%

Inflation makes salary negotiation non-negotiable.

Strategies:

- Tie raises to CPI.

- Negotiate annually, not biannually.

- Switch employers strategically.

- Upskill continuously.

Your earning power is your first line of inflation defense.

22. Side Income and Skill-Based Inflation Protection

In an inflationary world, relying on a single income stream is risky.

Best inflation-resistant income sources:

- Freelancing

- Consulting

- Online businesses

- Rentals

- Dividend portfolios

- Royalties

- Digital products

Skills that protect against inflation:

- Tech

- Data

- Finance

- Healthcare

- AI

- Cybersecurity

- Sales

Skills compound faster than money.

23. The Power of Automation and Rebalancing

Inflation defense is not a one-time decision — it’s a system.

Automation:

- Auto-invest monthly.

- Auto-rebalance annually.

- Auto-increase contributions.

Rebalancing:

- Sells overperforming assets.

- Buys undervalued ones.

- Maintains risk alignment.

This removes emotion — and emotion is inflation’s greatest ally.

24. Common Inflation Myths That Cost You Money

Myth 1: “Cash is safe.”

Reality: Cash is the most guaranteed way to lose purchasing power.

Myth 2: “Inflation will go back to normal.”

Reality: Structural forces make persistent inflation likely.

Myth 3: “Investing during inflation is too risky.”

Reality: Not investing is riskier.

Myth 4: “Only the wealthy can protect against inflation.”

Reality: Anyone can — with the right strategy.

25. A Simple Inflation-Fighting Portfolio for 2026

Here’s a balanced, inflation-resistant portfolio:

- 50% Stocks (global equity index funds)

- 20% Real Estate (REITs or direct property)

- 10% Inflation-Protected Bonds

- 10% Commodities / Gold

- 10% Cash / High-Yield Savings

Adjust based on:

- Age

- Risk tolerance

- Income stability

- Time horizon

26. How to Adjust Your Strategy at Different Life Stages

In Your 20s–30s:

- Maximize growth.

- Focus on stocks and skills.

- Use leverage responsibly.

In Your 40s–50s:

- Balance growth and protection.

- Increase real estate and inflation-linked bonds.

In Retirement:

- Prioritize income.

- Use inflation-adjusted payouts.

- Protect purchasing power.

Inflation affects every stage — but your response should evolve.

27. Case Study: Two Savers, Two Outcomes

Saver A:

- Saves $500/month in cash.

- Earns 2% interest.

- Inflation averages 5%.

After 30 years:

- Account balance: ~$250,000

- Real purchasing power: ~$110,000

Saver B:

- Invests $500/month.

- Earns 8% return.

- Inflation averages 5%.

After 30 years:

- Account balance: ~$745,000

- Real purchasing power: ~$330,000

Same savings effort. Drastically different outcomes.

Inflation rewards investors — and punishes idle savers.

28. What Happens If Inflation Persists for a Decade?

If inflation remains elevated for 10+ years:

- Cash savings become almost worthless in real terms.

- Housing becomes increasingly unaffordable.

- Retirement timelines extend.

- Wealth inequality widens.

- Only asset owners preserve purchasing power.

This isn’t hypothetical — history has shown this repeatedly.

29. Mistakes to Avoid During Inflationary Periods

- Hoarding cash

- Panic selling investments

- Chasing hype assets

- Ignoring income growth

- Avoiding debt entirely

- Overreacting to short-term market noise

- Failing to rebalance

- Delaying financial education

The biggest mistake:

Doing nothing.

30. Trusted Financial Resources

- Inflation data from the U.S. Bureau of Labor Statistics

- UK inflation insights from the Office for National Statistics

- Monetary policy updates from the Federal Reserve

31.❓ Frequently Asked Questions

What does it mean that inflation destroys savings?

Inflation reduces the purchasing power of money, meaning your savings can buy less over time.

How can I protect my savings from inflation?

You can invest in stocks, real estate, and inflation-protected securities to beat inflation.

Is keeping money in savings accounts safe?

No, because inflation destroys savings if interest rates are lower than inflation.

32. Final Thoughts: Turning Inflation from Enemy to Ally

Inflation is not your enemy — ignorance is.

Inflation will happen whether you prepare or not. But you get to choose:

- Be a victim — or a strategist.

- Lose purchasing power — or gain it.

- Watch your savings shrink — or grow.

When you understand inflation, you can:

- Use debt intelligently.

- Invest strategically.

- Earn more.

- Protect your future.

- Build real wealth.

The people who thrive in inflationary times are not lucky — they’re informed, disciplined, and proactive.

And now, so are you.