A bulletproof monthly budget is not just about tracking expenses—it’s about building a reliable financial system.

In high-cost economies like the United States, United Kingdom, Canada, and Australia, the margin for financial error is shrinking. Housing costs are rising, inflation remains persistent, and lifestyle inflation quietly erodes savings. A structured, strategic monthly budgeting system is no longer optional—it is foundational to long-term financial stability and wealth accumulation.

Studies show that individuals who follow structured budgeting systems are significantly more likely to achieve long-term financial independence.

Financial planners consistently rank budgeting as one of the top foundational habits for long-term wealth building and financial independence.

While budgeting may not be glamorous, it remains one of the most effective systems for achieving financial stability in high-cost economies. Yet it’s one of the most powerful financial tools a person can use to take control of money, eliminate stress, and achieve lifelong financial goals. Whether you’re trying to pay down debt, save for a home, or finally understand where your money actually goes each month, a bulletproof budget is the foundation.

In most developed economies, household savings rates typically range between 10%–20%, highlighting the importance of structured financial planning.

In this guide, we’ll walk through practical steps to create a monthly budget that actually works—not one that fails by week two.

According to financial data from central banking institutions and long-term investment firms, consistent budgeting and disciplined saving habits are among the strongest predictors of long-term wealth accumulation. Individuals who follow structured budgeting systems tend to build financial stability faster than those who rely on unplanned spending.

By the end of this guide, you will have a complete, practical monthly budgeting system that you can implement immediately—even if you’ve struggled with budgeting in the past.

What is a Bulletproof Monthly Budget?

A bulletproof monthly budget is a structured financial plan that helps you manage income, control expenses, and consistently save money to achieve long-term financial stability and growth.

1. Why Most Bulletproof Monthly Budgets Fail

Before we build a strong system, it’s important to understand why many people struggle to maintain a bulletproof monthly budget:

❌ Unrealistic Expectations

Many people create overly strict budgets that are impossible to follow long-term. They cut too many expenses at once without considering real-life needs and habits. This leads to frustration and eventually abandoning the budget completely.

❌ One‑Size‑Fits‑All Models

Using generic budgeting templates from apps or influencers often doesn’t match your personal financial situation. Everyone has different income levels, responsibilities, and goals. A budget must be customized to your lifestyle to be effective.

❌ Lack of Accountability

Without tracking spending regularly, a budget becomes more of a suggestion than a rule. When there is no system to monitor expenses, overspending goes unnoticed. Accountability is what turns a plan into actual financial discipline.

❌ Not Addressing Emotional Spending

Many people overlook the emotional reasons behind their spending habits. Stress, boredom, or impulse can lead to unnecessary purchases. Without understanding these triggers, it becomes very difficult to stick to any budget.

A successful budget doesn’t just monitor your money—it reflects your lifestyle, goals, and habits, making it easier to follow consistently.

2. What a Bulletproof Monthly Budget Looks Like (Complete Breakdown)

A bulletproof budget is:

✅ Clear & simple

A bulletproof monthly budget should be easy to understand and manage without confusion. It avoids unnecessary categories, complex formulas, or overwhelming spreadsheets that make tracking difficult. Simplicity ensures consistency, which is key to long-term success.

✅ Flexible

Your budget should adapt to real-life changes such as a new job, relocation, salary increase, or unexpected expenses. A rigid system often fails because life is unpredictable. Flexibility allows you to adjust without breaking your entire financial plan.

✅ Actionable

A good budget doesn’t just show numbers—it gives clear direction on how much to spend, save, and invest. It acts like a financial roadmap, helping you make informed decisions every day. Without actionability, a budget becomes just a passive document.

✅ Trackable

A bulletproof monthly budget allows you to monitor your progress regularly—weekly or monthly. You should be able to compare planned vs actual spending easily. Tracking helps identify patterns, control overspending, and improve financial discipline over time.

3. Step-by-Step: Building a Bulletproof Monthly Budget That Actually Works

Let’s break down the process from zero to finish.

Step 1 — Know Your Net Income

The first and most important number in your budget is your net income—what you actually bring home after taxes, retirement contributions, health insurance, etc.

📌 Gross income ≠ Take‑home pay

Your budget must use net pay, not gross.

If you have irregular income, use an average from the last 6 months.

Step 2 — List Every Monthly Expense

Write down every expense you have, including:

🟢 Fixed Expenses

These don’t change month to month:

- Rent / mortgage

- Insurance

- Phone bill

- Subscriptions

🔵 Variable Expenses

These do change:

- Groceries

- Gas / ride‑hailing

- Dining out

- Entertainment

🔴 Periodic Expenses

Not monthly, but predictable:

- Car maintenance

- Annual memberships

- Holidays / birthdays

🔥 Emotional Spending

Impulse buys:

- Coffee runs

- Online shopping

- Eating out

This step requires honesty.

💡 Tip: Look at the last 3 months of bank/credit card statements and include everything.

Step 3 — Categorize & Prioritize Your Bulletproof Monthly Budget

Group expenses into needs vs wants:

| Needs (fixed/essential) | Wants (optional/variable) |

|---|---|

| Rent / mortgage | Streaming subscriptions |

| Groceries | Dining out |

| Utilities | Travel |

| Insurance | Hobbies |

| Transportation | Premium coffee |

Your budget should fund needs first, then savings, then wants.

Step 4 — Set Clear Financial Goals

Every budget should be tied to goals. Goals fall into three buckets:

🎯 Short‑Term (0–12 months)

- Build an emergency fund

- Pay off credit card debt

- Save for a vacation

📈 Medium‑Term (1–5 years)

- Save for a down payment

- Buy a car

- Fund education

🏆 Long‑Term (5+ years)

- Retirement

- Investment portfolio

- Financial independence

Write down your goals and assign a timeline and dollar amount to each.

Step 5 — Choose a Budgeting Method

Here are popular budgeting frameworks:

🧮 50/30/20 Rule

- 50% Needs

- 30% Wants

- 20% Savings / Debt Repayment

Good for beginners.

📊 Zero‑Based Budget

Every dollar is assigned a job:

Income − Expenses − Savings = $0

Best for control and accountability.

🏦 Envelope / Digital Envelope System

Allocate money into categories (cash envelopes or app wallets).

When the envelope is empty, spending stops.

📆 Paycheck Budgeting

Split your budget based on pay dates (e.g., 1st vs 15th of the month).

Pick one that fits your style. You can change later.

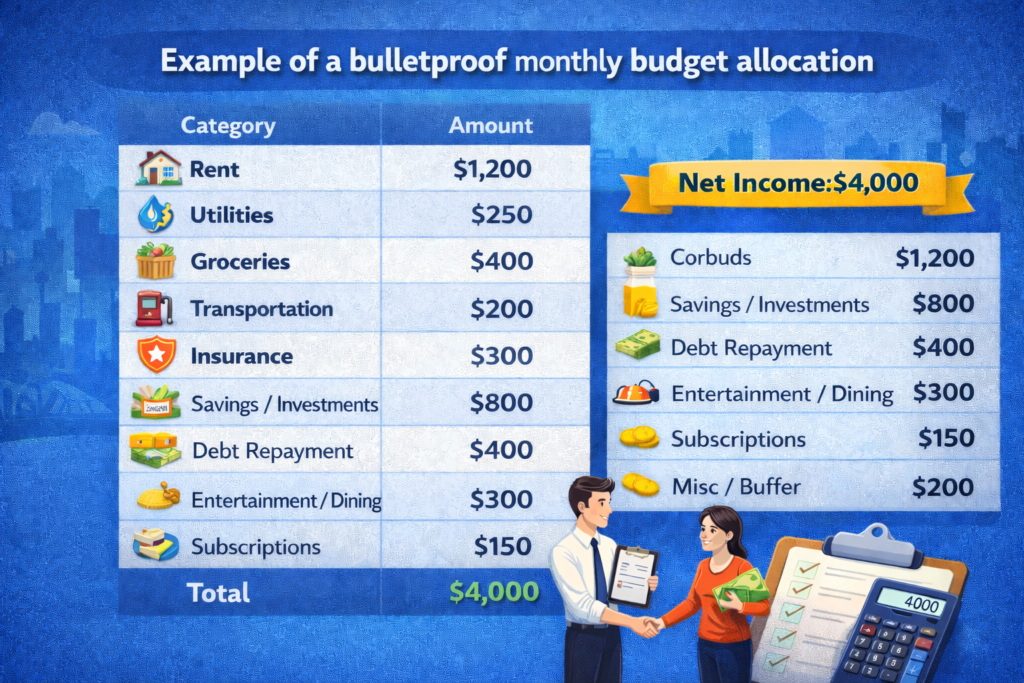

Step 6 — Allocate Money to Categories

At this stage, your bulletproof monthly budget plan becomes actionable. Now assign dollar amounts to each category based on your priorities:

- Needs first → make sure essentials are covered

- Savings next → pay yourself first

- Wants last — after everything else

Example — Monthly Budget (Net Income $4,000):

| Category | Amount |

|---|---|

| Rent | $1,200 |

| Utilities | $250 |

| Groceries | $400 |

| Transportation | $200 |

| Insurance | $300 |

| Savings / Investments | $800 |

| Debt Repayment | $400 |

| Entertainment / Dining | $300 |

| Subscriptions | $150 |

| Misc / Buffer | $200 |

| Total | $4,000 |

Step 7 — Track Spending Daily to Maintain a Bulletproof Monthly Budget

Tracking is what transforms a simple plan into a bulletproof monthly budget. A budget only works if you track it.

Use:

✅ Banking app categories

✅ Budgeting apps (You Need a Budget, EveryDollar, Mint)

✅ Spreadsheets

✅ Manual notebook

Track actual spending vs budgeted spending. Studies show that individuals who track their spending weekly are significantly more likely to stay within budget and achieve their financial goals compared to those who don’t monitor their expenses.

Ask yourself:

🔹 Did I overspend this week?

🔹 Why?

🔹 Is it a one‑time thing or a habit?

4. Real‑World Tested Budgeting Tools

Here are highly effective tools you can choose from:

💻 Digital Tools

| Tool | Best For |

|---|---|

| YNAB | Zero‑based budgeting |

| Mint | Free tracking & alerts |

| EveryDollar | Simple budgeting |

| Personal Capital | Investments + budget |

| Excel / Google Sheets | Custom control |

📱 Practical Tools for Daily Tracking

- Bank alerts for large transactions

- Quick note in phone after spending

- Weekly budget check‑ins

These small habits dramatically increase success.

5. Clever Ways to Reduce Expenses

Budget must be realistic. If expenses exceed income, cut costs.

💡 Simple Reductions

- Switch phone plans

- Negotiate bills (internet, insurance)

- Cancel unused subscriptions

- Use public transit when possible

🍎 Grocery Savings

- Meal plan weekly

- Use loyalty programs

- Shop sales

- Buy generic brands

💰 Big Expense Tactics

- Refinance student loans

- Refinance mortgage

- Lower rent by downsizing or moving

6. How to Stop Emotional Spending

Most budgets fail because people ignore the emotional side of money. Understanding your behavior is just as important as tracking numbers.

Strategies That Work

🎯 Track Your Triggers

Ask: Identify the situations, emotions, or habits that lead to overspending. It could be stress, boredom, or social pressure.

By recognizing these triggers, you gain awareness and can take control before making impulsive purchases.

Write them down.

🛑 Create Barriers

Make spending less convenient by removing saved credit card details or unsubscribing from marketing emails.

Simple rules like waiting 24 hours before buying can significantly reduce impulse spending and improve decision-making.

🧠 Replace the Habit

Instead of spending to cope with emotions, replace it with healthier alternatives like walking, reading, or talking to a friend.

Over time, these positive habits reduce dependency on spending and help build long-term financial discipline.

Budgeting is a behavior change, not just math.

7. Mid‑Month Check‑Ins & Adjustments

Don’t wait until month’s end, regular reviews are essential to keep your bulletproof monthly budget on track and effective.

Weekly Budget Reviews

✔ How much spent vs budgeted

Review your actual spending against your planned budget at least once a week. This helps you clearly see where your money is going and ensures your bulletproof monthly budget stays aligned with your financial goals.

✔ Any categories going over

Identify categories where you’re overspending, such as dining or shopping. Catching these early allows you to make quick corrections and prevents your bulletproof monthly budget from falling off track.

✔ Adjust remaining spending

If one category exceeds its limit, reallocate funds from another category with lower spending. This flexibility keeps your bulletproof monthly budget balanced without disrupting your overall financial plan.

Example:

If you overspent on groceries but underspent on entertainment, shift the remaining funds accordingly. This simple adjustment helps maintain consistency and keeps your bulletproof monthly budget realistic and sustainable.

8. How to Budget with Irregular Income

This is common for freelancers, contractors, or commission‑based work.

Steps That Work

- Calculate a baseline monthly income using a 6‑month average.

- Build a buffer (goal: 1 month of expenses saved).

- Prioritize fixed costs first.

- Use excess income for savings and variable costs.

With irregular income, your buffer is your superpower.

9. Emergency Fund: Your Financial Safety Net

No bulletproof monthly budget is complete without a strong emergency fund. A bulletproof budget isn’t complete without an emergency fund.

What It Is

Cash saved for unexpected events:

- Job loss

- Medical emergencies

- Major car/home repairs

How Much You Need

Tier‑1 averages recommend:

➡ 3–6 months of essential expenses

Save this before tackling large discretionary budgets.

Financial experts widely recommend maintaining at least 3–6 months of essential expenses, as unexpected events are one of the leading causes of financial instability.

10. Automation: Budgeting Without the Pain

Today’s banks and apps let you automate:

✔ Savings transfers

✔ Bill payments

✔ Investments

✔ Debt payments

Automation helps because:

➡ You don’t have to remember every transfer

➡ It prevents spending what should be saved

11. Budgeting for Couples or Families

When money is shared, communication becomes the most important tool.

Best Practices

- Share goals together

- Decide on joint vs personal accounts

- Do weekly or monthly budget meetings

- Agree on spending limits for discretionary items

12. How to Handle Budget “Failures”

You will slip up. It’s not failure — it’s feedback.

Instead of guilt:

✔ Identify the cause

✔ Ask what you learned

✔ Adjust budget categories

The best budgets are fluid, not fixed.

13. Ways to Make Budgeting More Motivational

Budgeting shouldn’t feel like punishment. When your bulletproof monthly budget is engaging and rewarding, it becomes easier to stick with it long-term.

Make it fun:

🎉 Reward progress

Celebrate small wins when you follow your bulletproof monthly budget, such as staying within limits or hitting savings goals. Rewards don’t have to be expensive—they can be simple treats or experiences. This positive reinforcement keeps you motivated and consistent.

📈 Track savings visually

Seeing your progress visually makes your bulletproof monthly budget more exciting and real. Use charts, apps, or simple trackers to watch your savings grow over time. Visual feedback builds momentum and encourages you to stay disciplined.

📊 Use graphs and charts

Graphs and charts turn your bulletproof monthly budget into a clear and engaging system. They help you quickly understand spending patterns and identify areas to improve. This makes budgeting feel more like progress tracking than restriction.

👫 Budget with a partner or friend

Sharing your bulletproof monthly budget journey with someone increases accountability and support. You can discuss goals, track progress together, and stay motivated during challenges. Having a partner makes the process more enjoyable and sustainable.

Motivation leads to consistency and consistency is what makes a bulletproof monthly budget truly effective.

14. Advanced Tactics for Bulletproof Success

Once basics are mastered, level up:

📍 Split Accounts

Use accounts for specific purposes:

- Bills account

- Saving account

- Credit buffer account

📍 Pay Yourself First

Make savings a fixed expense, not optional.

📍 Annual Budget Review

At year’s end:

- Evaluate goals achieved

- Adjust next year’s budget

📍 Use Financial KPIs

Track:

- Savings rate

- Debt‑to‑income

- Spending trends

Numbers create clarity.

15. How Budgeting Improves Life Beyond Money

A good budget doesn’t just manage money—it improves life:

✔ Less stress

A well-structured budget removes uncertainty about where your money is going each month. When you have a clear plan, financial anxiety reduces significantly. You feel more in control and less worried about unexpected expenses.

✔ More confidence

Knowing that you are managing your money effectively builds strong financial confidence. You can make decisions without hesitation because you understand your financial position. This confidence extends to bigger life choices like investments or career moves.

✔ Financial freedom

Budgeting helps you allocate money toward savings and investments consistently. Over time, this builds wealth and reduces dependence on paycheck-to-paycheck living. Financial freedom means having choices, not restrictions.

✔ Better decisions

With a clear budget, every financial decision becomes more intentional and informed. You can evaluate whether a purchase aligns with your goals or not. This leads to smarter spending and fewer regrets.

✔ Long‑term security

A disciplined budgeting system ensures you are preparing for the future, not just the present. It helps build emergency funds, retirement savings, and financial stability. Over time, this creates a strong safety net for any life situation.

🔚 Closing Line

Many people find that once they start budgeting consistently, it feels like finally gaining full control over their financial life—and that clarity often leads to overall life improvement.

16. Sample Budget Templates

📄 Budget Template — Zero‑Based

| Category | Budget | Actual | Difference |

|---|---|---|---|

| Income | $ | $ | – |

| Fixed Expenses | $ | $ | $ |

| Variable Expenses | $ | $ | $ |

| Savings/Investments | $ | $ | $ |

| Debt Payments | $ | $ | $ |

| Total | $ | $ | $ |

17. Common Budgeting Mistakes to Avoid

🚫 Ignoring annual bills

🚫 Using gross income

🚫 Not tracking spending

🚫 Not updating the budget regularly

🚫 Forgetting to save for irregular expenses

🚫 Trying to be perfect

Perfection isn’t the goal — consistency is.

18. How to Maintain a Bulletproof Monthly Budget Long-Term

Maintaining a bulletproof monthly budget long-term requires consistency, flexibility, and regular review. Track your spending weekly and adjust categories as your income or expenses change.

Automate savings and bill payments to remove decision fatigue and ensure discipline. Periodically revisit your financial goals to stay motivated and aligned with your priorities. Most importantly, treat your budget as a dynamic system—not a fixed rulebook—so it evolves with your life.

19. Final Thoughts

A bulletproof monthly budget gives you control, clarity, and confidence over your financial future.

A budget isn’t a prison—it’s a roadmap. It doesn’t restrict your life; it frees you from financial guessing, anxiety, and uncertainty. With discipline, clarity, and simple systems in place, you can turn your money into a tool that supports your goals, not controls you.

20. Trusted Financial Resources

- Budgeting data from the Federal Reserve highlights the importance of structured savings habits.

- Tax-saving strategies from the Internal Revenue Service can help optimize your financial planning.

- Long-term investment insights from Vanguard Group support disciplined wealth building.

❓ Frequently Asked Questions

What is a bulletproof monthly budget?

A bulletproof monthly budget is a structured financial plan that tracks income, expenses, savings, and investments to ensure financial stability and long-term growth.

How much should I save monthly?

A common rule is the 50/30/20 budget where at least 20% of income is allocated toward savings and debt repayment.

Which budgeting method is best?

Zero-based budgeting is considered the most effective because it assigns every dollar a purpose.

How do beginners start a monthly budget?

Start by calculating your net income, listing all expenses, and using a simple rule like the 50/30/20 method to allocate money clearly.

What is the best budgeting rule in 2026?

The 50/30/20 rule remains the best for simplicity, while zero-based budgeting is ideal for those who want maximum control over every dollar.

21. Quick Start Checklist

✔ Calculate net income

✔ List every expense

✔ Prioritize needs first

✔ Build a simple budget framework

✔ Track spending weekly

✔ Automate savings

✔ Review & adjust

✔ Build an emergency fund

How to Save $10,000 a Year Without Sacrificing Your Lifestyle (2026 Guide)How Inflation Destroys Savings (2026 Survival Guide to Beat Inflation)Biggest Money Mistakes Middle-Class Families Make in 2026Improve Credit Score Fast (Legally & Safely) – 2026 Ultimate Guide

How Inflation Destroys Savings (2026 Survival Guide to Beat Inflation)