Portfolio Rebalancing Explained

Portfolio Rebalancing Explained is one of the most important concepts in long-term investing. It helps investors maintain their target asset allocation, control portfolio risk, and improve investment discipline during changing market conditions.

This comprehensive guide explains portfolio rebalancing, how it works, why it matters, common strategies, real-world examples, and case studies from major investment markets including the United States, Canada, Australia, and the United Kingdom.

A portfolio that is not rebalanced can slowly become far riskier than intended. For example, an investor who originally wanted a “moderate-risk” portfolio may accidentally end up with an “aggressive-growth” portfolio after years of stock market gains.

This article explains portfolio rebalancing in detail, including:

- What portfolio rebalancing means

- Why it matters

- Types of rebalancing strategies

- Rebalancing frequency

- Tax implications

- Behavioral finance principles

- Retirement portfolio management

- ETF and index fund rebalancing

- Case studies from Tier-1 countries

- Common mistakes

- Real-world examples

What Is Portfolio Rebalancing?

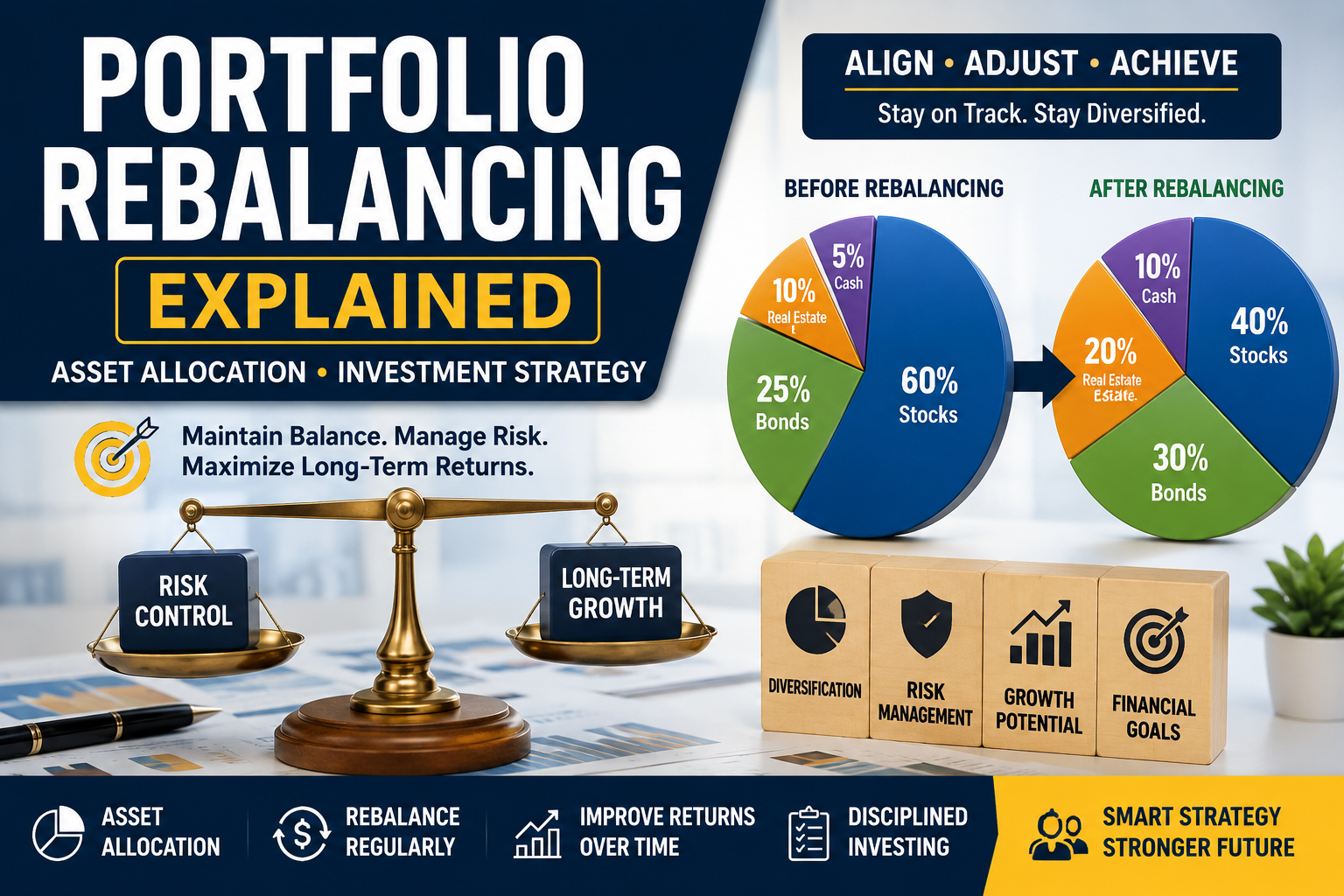

Portfolio rebalancing is the process of adjusting investments back to their intended allocation after market movements change the weight of assets inside a portfolio.

A portfolio usually contains multiple asset classes such as:

- Stocks

- Bonds

- Cash

- Real estate

- Commodities

- International equities

When markets move, some investments grow faster than others.

For example:

| Asset | Original Allocation | After Market Growth |

|---|---|---|

| Stocks | 60% | 75% |

| Bonds | 40% | 25% |

This means the portfolio now carries more stock market risk than originally planned.

Rebalancing restores the intended allocation.

The investor may:

- Sell some stocks

- Buy more bonds

- Return to 60/40 allocation

Understanding Asset Allocation

Portfolio rebalancing cannot be understood without understanding asset allocation.

Asset allocation refers to how investments are distributed across asset categories.

A common retirement portfolio in the USA might look like:

| Asset Class | Allocation |

|---|---|

| US Stocks | 50% |

| International Stocks | 20% |

| Bonds | 25% |

| Cash | 5% |

Each asset behaves differently under economic conditions.

Stocks

Stocks represent ownership in companies.

Examples include:

- Apple

- Microsoft

- Amazon

Stocks generally provide:

- Higher growth

- Higher volatility

- Inflation protection

Bonds

Bonds are loans to governments or corporations.

Examples:

- US Treasury bonds

- Corporate bonds

- Municipal bonds

Bonds generally provide:

- Lower volatility

- Stable income

- Capital preservation

Cash

Cash includes:

- Savings accounts

- Money market funds

- Treasury bills

Cash provides:

- Liquidity

- Stability

- Emergency reserves

Why Portfolio Rebalancing Matters

1. Risk Control

The primary purpose of rebalancing is risk management.

Without rebalancing, a portfolio can drift far away from the investor’s original risk tolerance.

Example:

An investor aged 60 nearing retirement may begin with:

- 50% stocks

- 50% bonds

After a strong bull market:

- Stocks rise to 70%

- Bonds fall to 30%

Now the investor faces substantially greater downside risk before retirement.

Rebalancing restores safety.

2. Emotional Discipline

Rebalancing creates a rules-based investing system.

This reduces emotional decisions caused by:

- Fear

- Greed

- Panic selling

- Euphoria

Rebalancing forces investors to:

- Sell assets after large gains

- Buy assets after declines

This is psychologically difficult but financially beneficial over long periods.

3. Buy Low, Sell High

One hidden advantage of rebalancing is that it naturally encourages buying undervalued assets and trimming overvalued ones.

Example:

During a stock market crash:

- Stock allocation falls

- Bond allocation rises proportionally

Rebalancing requires:

- Selling some bonds

- Buying cheaper stocks

This creates disciplined contrarian investing.

4. Retirement Stability

Retirees need predictable risk exposure.

Without rebalancing:

- Large stock exposure may cause major losses

- Withdrawals during downturns become dangerous

This is known as sequence-of-returns risk.

Rebalancing helps retirees preserve wealth during market volatility.

How Portfolio Drift Happens

Portfolio drift occurs when market performance changes the percentage allocation of investments.

Example:

Initial portfolio:

- $100,000 total

- 60% stocks = $60,000

- 40% bonds = $40,000

After several years:

- Stocks grow to $120,000

- Bonds grow to $45,000

New portfolio:

- Total = $165,000

- Stocks = 73%

- Bonds = 27%

Even though the investor never changed strategy, risk increased dramatically.

Types of Portfolio Rebalancing

There are several major rebalancing methods.

1. Calendar Rebalancing

This means rebalancing at fixed time intervals.

Examples:

- Monthly

- Quarterly

- Semi-annually

- Annually

Most long-term investors rebalance:

- Once or twice per year

Advantages:

- Simple

- Easy to automate

- Reduces overtrading

Disadvantages:

- May ignore major market changes between dates

2. Threshold Rebalancing

Threshold rebalancing occurs when allocations move beyond a predefined percentage.

Example:

- Target stock allocation = 60%

- Rebalance if stocks exceed 65% or fall below 55%

Advantages:

- More responsive to market conditions

- Better risk control

Disadvantages:

- Requires monitoring

3. Hybrid Rebalancing

Many institutional investors use hybrid systems.

Example:

- Check quarterly

- Rebalance only if deviation exceeds 5%

This reduces unnecessary trades while maintaining discipline.

Strategic Asset Allocation

Strategic asset allocation uses long-term target percentages based on:

- Risk tolerance

- Age

- Goals

- Time horizon

Example for a 30-year-old investor:

| Asset | Allocation |

|---|---|

| US Stocks | 70% |

| International Stocks | 20% |

| Bonds | 10% |

Rebalancing maintains these targets over decades.

Tactical Asset Allocation

Tactical allocation temporarily adjusts portfolio weights based on market expectations.

Example:

- Increasing bonds before recession

- Increasing stocks during economic recovery

This approach is more active and requires forecasting skill.

Many professional investors fail to consistently outperform simple strategic rebalancing.

The Psychology of Rebalancing

Behavioral finance plays a major role in investing.

Humans naturally:

- Chase performance

- Buy during bubbles

- Sell during crashes

Rebalancing counters these biases.

Recency Bias

Investors assume recent performance will continue forever.

Example:

- Technology stocks soar

- Investors keep buying more tech

Rebalancing forces reduction in overweight sectors.

Loss Aversion

People fear losses more than they value gains.

During bear markets:

- Investors panic

- Sell at lows

Rebalancing encourages disciplined buying during downturns.

Rebalancing and Modern Portfolio Theory

Harry Markowitz developed Modern Portfolio Theory (MPT).

MPT argues investors can maximize returns for a given level of risk through diversification.

Portfolio rebalancing is essential to maintaining:

- Efficient diversification

- Target risk exposure

- Optimal risk-return balance

The 60/40 Portfolio

One of the most famous rebalanced portfolios is the 60/40 portfolio.

Typical allocation:

- 60% stocks

- 40% bonds

Historically:

- Stocks provide growth

- Bonds reduce volatility

Example:

| Market Condition | Stocks | Bonds |

|---|---|---|

| Bull Market | Strong | Moderate |

| Recession | Weak | Strong |

| Inflation Shock | Mixed | Weak |

Rebalancing keeps the portfolio aligned with intended risk.

Rebalancing with Index Funds and ETFs

Many investors today rebalance using:

- Index funds

- Exchange-traded funds (ETFs)

Popular examples include:

- Vanguard index funds

- BlackRock iShares ETFs

- Fidelity Investments mutual funds

Advantages:

- Low fees

- Broad diversification

- Tax efficiency

- Easy rebalancing

Example of ETF Rebalancing

Portfolio:

| ETF | Allocation |

|---|---|

| S&P 500 ETF | 50% |

| International ETF | 20% |

| Bond ETF | 30% |

After a tech rally:

- S&P ETF rises sharply

- Allocation becomes 65%

Investor sells part of S&P ETF and buys bond ETF.

This restores balance.

Tax Implications of Rebalancing

Taxes are extremely important in Tier-1 countries.

Selling appreciated investments may trigger:

- Capital gains tax

- Income tax consequences

United States Tax Rules

In the United States:

- Short-term gains taxed at ordinary income rates

- Long-term gains taxed at preferential rates

Investors often rebalance inside:

- 401(k)

- IRA

- Roth IRA

These accounts reduce tax impact.

United Kingdom Tax Rules

In the United Kingdom:

- Capital Gains Tax applies above annual allowance

- ISAs provide tax-free investing

Many UK investors rebalance within Stocks & Shares ISAs.

Canada Tax Rules

In Canada:

- 50% of capital gains are taxable

- TFSAs and RRSPs provide tax advantages

Australia Tax Rules

In Australia:

- Capital gains discounts apply after 12 months

- Superannuation accounts provide tax benefits

Tax-Efficient Rebalancing Strategies

1. Use New Contributions

Instead of selling winners:

- Direct new money into underweighted assets

Example:

- Stocks overweight

- Buy bonds with new contributions

This reduces taxes.

2. Rebalance in Retirement Accounts

Tax-sheltered accounts are ideal for rebalancing.

Examples:

- 401(k)

- IRA

- RRSP

- Superannuation

3. Harvest Tax Losses

Tax-loss harvesting involves:

- Selling investments at losses

- Offsetting gains

This strategy is popular among high-income investors.

Rebalancing Frequency

How often should investors rebalance?

Research suggests:

- Over-rebalancing may reduce returns

- Under-rebalancing increases risk

Most experts recommend:

- Annual review

- Threshold-based adjustments

Case Study: The Tech Bubble

During the late 1990s:

- Technology stocks surged

- Investors abandoned diversification

When the dot-com crash occurred:

- Many concentrated portfolios collapsed

Investors who rebalanced:

- Reduced tech exposure

- Preserved more capital

This demonstrates how rebalancing protects against bubbles.

Case Study: The 2008 Financial Crisis

Before 2008:

- Stocks dominated portfolios

- Real estate boomed

After the crisis:

- Equity markets crashed

Disciplined rebalancing helped investors:

- Buy equities at depressed prices

- Participate in the recovery

Those who panicked often locked in permanent losses.

Case Study: COVID-19 Market Crash

In March 2020:

- Global markets fell sharply

- Fear dominated investors

Balanced portfolios required:

- Buying equities during panic

Investors who rebalanced benefited enormously during the recovery rally.

Rebalancing for Different Age Groups

Investors in Their 20s

Goals:

- Growth

- Long time horizon

Possible allocation:

- 80–90% equities

Rebalancing still matters because:

- Tech concentration risk can become excessive

Investors in Their 30s and 40s

Focus:

- Wealth accumulation

- Retirement planning

- Family financial goals

Balanced diversification becomes more important.

Investors in Their 50s and 60s

Focus shifts toward:

- Capital preservation

- Income generation

Rebalancing protects retirement savings from large drawdowns.

Glide Paths and Target-Date Funds

Target-date funds automatically rebalance portfolios over time.

Example:

- Younger investors hold more stocks

- Allocation gradually shifts toward bonds

Major providers include:

- Vanguard

- Fidelity Investments

- Charles Schwab

These funds simplify retirement investing.

Rebalancing During Inflation

Inflation affects asset classes differently.

High inflation may hurt:

- Bonds

- Cash purchasing power

Assets that may perform better:

- Stocks

- Commodities

- Real estate

Rebalancing prevents portfolios from becoming overly exposed to inflation-sensitive assets.

Common Rebalancing Mistakes

1. Rebalancing Too Frequently

Constant trading:

- Increases taxes

- Raises fees

- Reduces efficiency

2. Ignoring Taxes

Selling appreciated assets carelessly can create large tax bills.

3. Emotional Decision-Making

Many investors stop rebalancing during crises because fear overrides discipline.

4. Chasing Winners

Investors often increase allocations to recently successful sectors.

This creates concentration risk.

Institutional Rebalancing

Large pension funds and endowments regularly rebalance portfolios.

Examples include:

- University endowments

- Sovereign wealth funds

- Pension systems

Institutional investors use:

- Risk models

- Allocation bands

- Automated systems

Automated Rebalancing and Robo-Advisors

Modern technology allows automatic rebalancing.

Popular robo-advisors include:

- Betterment

- Wealthfront

Benefits:

- Automation

- Low emotional interference

- Tax optimization

- Consistency

Example of Full Portfolio Rebalancing

Initial portfolio:

| Asset | Amount | Allocation |

|---|---|---|

| US Stocks | $300,000 | 60% |

| Bonds | $150,000 | 30% |

| International Stocks | $50,000 | 10% |

After bull market:

| Asset | New Value |

|---|---|

| US Stocks | $450,000 |

| Bonds | $155,000 |

| International Stocks | $70,000 |

Total portfolio:

= $675,000

New allocation:

- US Stocks = 67%

- Bonds = 23%

- International = 10%

Investor sells part of US stocks and buys bonds.

Risk returns to intended level.

Rebalancing vs Market Timing

Rebalancing differs from market timing.

Market Timing

Attempts to predict:

- Tops

- Bottoms

- Economic cycles

Very difficult even for professionals.

Rebalancing

Uses:

- Rules

- Allocation targets

- Risk management

No prediction required.

This makes rebalancing more reliable for most investors.

Does Rebalancing Improve Returns?

Research shows:

- Rebalancing primarily improves risk-adjusted returns

- It may slightly reduce maximum returns during bull markets

- It significantly reduces catastrophic risk

For retirement investors, risk reduction is often more important than maximizing gains.

Real-World Example: American Retirement Investor

John, age 45 in the United States:

Initial portfolio:

- 70% US equities

- 20% international

- 10% bonds

After strong tech growth:

- US equities become 82%

John rebalances:

- Sells some US stock funds

- Buys bonds and international funds

Benefits:

- Reduces concentration risk

- Locks in gains

- Restores diversification

Real-World Example: Canadian Retiree

Sarah, age 67 in Canada:

Goal:

- Stable retirement income

Portfolio drift caused:

- Equity exposure to rise sharply

Sarah rebalanced toward:

- Bonds

- Dividend-paying stocks

- Cash reserves

This reduced volatility during retirement withdrawals.

Real-World Example: Australian Superannuation Investor

Michael in Australia uses automatic rebalancing inside his superannuation account.

Advantages:

- Minimal taxes

- Professional management

- Lower emotional investing mistakes

Mathematical Perspective of Rebalancing

Portfolio risk is often measured using:

- Standard deviation

- Correlation

- Volatility

Diversified portfolios reduce unsystematic risk.

A simple representation of portfolio return:

R_p = \sum_{i=1}^{n} w_i R_i

Where:

- (R_p) = portfolio return

- (w_i) = asset weight

- (R_i) = asset return

Rebalancing adjusts asset weights (w_i) back to target levels.

Volatility and Risk Control

Portfolio volatility depends on asset mix.

A simplified risk equation:

\sigma_p = \sqrt{w_1^2\sigma_1^2 + w_2^2\sigma_2^2 + 2w_1w_2\sigma_1\sigma_2\rho_{12}}

This formula shows:

- Portfolio risk depends on allocation

- Correlation matters

- Diversification reduces volatility

Rebalancing maintains intended risk characteristics.

Key Benefits of Portfolio Rebalancing

| Benefit | Explanation |

|---|---|

| Risk Management | Prevents excessive exposure |

| Emotional Discipline | Reduces panic decisions |

| Diversification | Maintains balance |

| Tax Planning | Supports efficient investing |

| Retirement Stability | Controls withdrawal risk |

| Long-Term Consistency | Keeps strategy aligned |

Final Thoughts

Portfolio rebalancing is not about predicting markets. It is about maintaining discipline, controlling risk, and staying aligned with long-term financial goals.

Many investors focus entirely on:

- Finding winning stocks

- Timing the market

- Following financial news

But long-term wealth creation often depends more on:

- Asset allocation

- Consistency

- Risk management

- Rebalancing discipline

For investors in the United States, United Kingdom, Canada, and Australia, portfolio rebalancing remains a foundational strategy for retirement planning, capital preservation, and sustainable wealth building.

A well-rebalanced portfolio:

- Prevents excessive risk

- Encourages disciplined investing

- Helps investors survive market crashes

- Supports steady long-term growth

In investing, success is often less about finding the perfect investment and more about managing risk intelligently over decades.