Portfolio Allocation by Age

Portfolio allocation by age is one of the most important concepts in investing and wealth management. It refers to how an investor divides money among different asset classes—such as stocks, bonds, cash, real estate, and alternative investments—based on their age, financial goals, risk tolerance, and investment horizon.

As people move through different stages of life, their financial priorities change. A 25-year-old professional saving for retirement has a very different investment strategy compared to a 65-year-old retiree relying on investments for income. Younger investors usually focus on growth and long-term wealth creation, while older investors often prioritize capital preservation and income stability.

In Tier-1 countries such as the United States, United Kingdom, Canada, and Australia, portfolio allocation by age is commonly used in retirement planning systems including 401(k)s, IRAs, ISAs, pension funds, RRSPs, and Superannuation accounts.

This guide explains every major concept in detail, including:

- What portfolio allocation means

- Why age matters in investing

- Risk tolerance and investment horizon

- Asset allocation strategies

- The “100 minus age” rule

- Conservative vs aggressive portfolios

- Retirement investing

- Case studies from Tier-1 countries

- Common mistakes

- Real-world examples

What Is Portfolio Allocation?

Portfolio allocation means dividing investments across multiple asset categories.

The goal is to balance:

- Risk

- Return

- Liquidity

- Stability

- Growth potential

An investment portfolio may include:

| Asset Class | Purpose |

|---|---|

| Stocks | Growth |

| Bonds | Stability and income |

| Cash | Liquidity and safety |

| Real Estate | Income and diversification |

| Commodities | Inflation protection |

| International Investments | Global diversification |

For example:

A 30-year-old investor may allocate:

- 80% stocks

- 15% bonds

- 5% cash

Meanwhile, a 65-year-old retiree may allocate:

- 40% stocks

- 50% bonds

- 10% cash

The younger investor seeks long-term growth, while the retiree seeks income and reduced volatility.

Understanding Asset Allocation

Asset allocation is the foundation of portfolio management.

Research from firms like Vanguard and BlackRock shows that asset allocation is one of the biggest drivers of long-term investment performance.

Asset allocation answers questions such as:

- How much should go into stocks?

- How much should remain in safer assets?

- How much risk is appropriate?

- How should investments change over time?

Why Age Matters in Portfolio Allocation

Age matters because investing involves time.

The younger the investor, the more time available to recover from market declines.

Older investors generally have:

- Shorter investment horizons

- Lower risk capacity

- Greater income needs

- Retirement concerns

Younger investors generally have:

- Longer investment horizons

- Higher risk capacity

- More earning years ahead

- Greater ability to tolerate volatility

Important Investment Terms

1. Risk Tolerance

Risk tolerance refers to the emotional and financial ability to handle investment losses.

Example:

If a portfolio falls by 30% during a market crash:

- A high-risk investor stays invested

- A low-risk investor may panic and sell

Risk tolerance depends on:

- Age

- Income

- Experience

- Personality

- Financial goals

2. Investment Horizon

Investment horizon means the length of time money will remain invested.

Examples:

| Goal | Time Horizon |

|---|---|

| Buying a car | 2 years |

| Buying a house | 7 years |

| Retirement at age 65 | 30 years |

Longer horizons allow more exposure to stocks because markets generally recover over long periods.

3. Volatility

Volatility means how much prices fluctuate.

Stocks are highly volatile.

Bonds are less volatile.

Cash has very low volatility.

Example:

- Stock market may fall 20% in a year

- Bond market may fall 5%

- Savings accounts rarely fluctuate

4. Diversification

Diversification means spreading investments across multiple assets to reduce risk.

Example:

Instead of buying only technology stocks, investors may own:

- US stocks

- International stocks

- Bonds

- REITs

- Commodities

Diversification reduces the impact of one asset performing poorly.

The Traditional “100 Minus Age” Rule

One famous investing rule says:

\text{Stock Allocation} = 100 – \text{Age}

Example:

| Age | Stock Allocation | Bond Allocation |

|---|---|---|

| 25 | 75% | 25% |

| 40 | 60% | 40% |

| 60 | 40% | 60% |

This rule is simple but somewhat outdated because people now live longer.

Modern Allocation Rules

Modern advisors sometimes use:

\text{Stock Allocation} = 110 – \text{Age}

or

\text{Stock Allocation} = 120 – \text{Age}

Why?

Because:

- Life expectancy increased

- Retirement periods became longer

- Inflation risk became more important

- Interest rates sometimes remain low

Example using the 110 rule:

| Age | Stocks | Bonds |

|---|---|---|

| 30 | 80% | 20% |

| 50 | 60% | 40% |

| 70 | 40% | 60% |

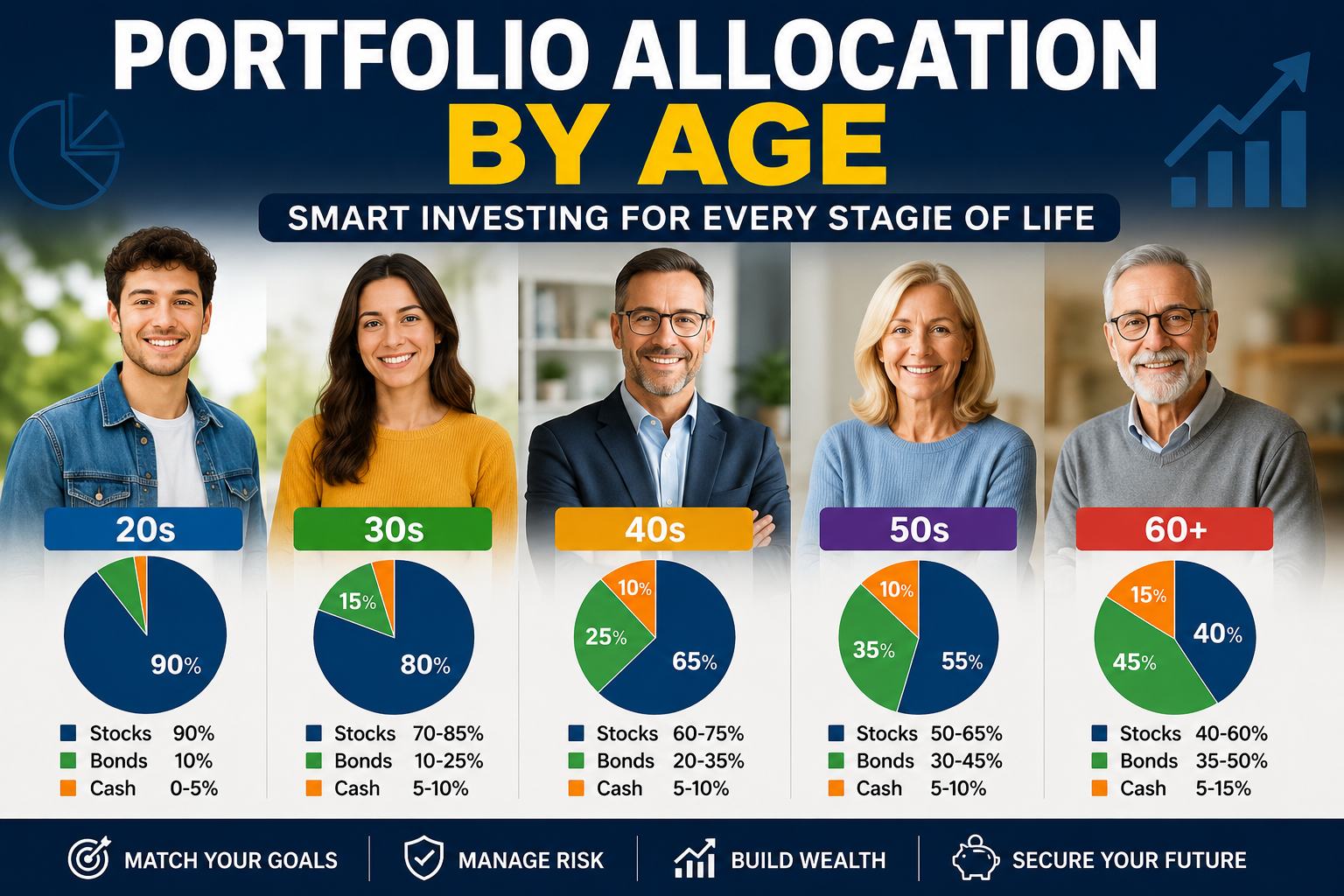

Portfolio Allocation in Your 20s

Your 20s are usually the most aggressive investing years.

Key Characteristics

- Long investment horizon

- High risk tolerance

- Smaller savings balances

- Higher growth potential

Typical Allocation

| Asset | Allocation |

|---|---|

| Stocks | 80–95% |

| Bonds | 5–15% |

| Cash | 0–5% |

Why Young Investors Can Take More Risk

Young investors have time on their side.

If markets crash, they may still have 30–40 years before retirement.

Historically, stock markets recover over long periods.

Example:

The Global Financial Crisis caused major declines in global markets, but long-term investors who stayed invested eventually recovered losses and achieved gains over the following decade.

Case Study: Young Investor in the United States

Sarah is 25 years old and works in New York City.

She contributes monthly to:

- 401(k)

- Roth IRA

- Index funds

Her allocation:

| Asset | Allocation |

|---|---|

| US Stocks | 70% |

| International Stocks | 20% |

| Bonds | 10% |

During a market correction, her portfolio falls 25%.

Instead of selling, she continues investing monthly.

Ten years later:

- Her investments recover

- Compounding accelerates growth

- Dollar-cost averaging lowers average purchase costs

This demonstrates long-term investing discipline.

Portfolio Allocation in Your 30s

People in their 30s often experience:

- Marriage

- Children

- Mortgage payments

- Career growth

Risk capacity remains relatively high, but stability becomes more important.

Typical Allocation

| Asset | Allocation |

|---|---|

| Stocks | 70–85% |

| Bonds | 10–25% |

| Cash | 5–10% |

Importance of Retirement Accounts

In Tier-1 countries, retirement investing becomes crucial during this stage.

Examples include:

| Country | Retirement System |

|---|---|

| USA | 401(k), IRA |

| UK | ISA, Pension |

| Canada | RRSP, TFSA |

| Australia | Superannuation |

These accounts provide tax advantages.

Case Study: Canadian Couple in Their 30s

David and Emma from Toronto invest through RRSPs and TFSAs.

Their allocation:

- 75% equities

- 20% bonds

- 5% cash

They diversify internationally to reduce dependence on the Canadian economy.

Their portfolio includes:

- US index funds

- Canadian dividend stocks

- International ETFs

- Government bonds

This creates balanced long-term exposure.

Portfolio Allocation in Your 40s

The 40s are often peak earning years.

Investors usually:

- Earn higher salaries

- Save more aggressively

- Become more focused on retirement

- Reduce excessive risk

Typical Allocation

| Asset | Allocation |

|---|---|

| Stocks | 60–75% |

| Bonds | 20–35% |

| Cash | 5–10% |

Sequence of Returns Risk

This is a critical concept.

Sequence risk means poor market returns occurring near retirement can significantly damage portfolios.

Example:

Two investors earn the same average return over 20 years.

However:

- Investor A experiences losses early

- Investor B experiences losses right before retirement

Investor B suffers more because there is less recovery time.

This is why allocation becomes more conservative with age.

Case Study: UK Professional in Midlife

James, age 45, lives in London.

He invests through:

- Workplace pension

- Stocks and Shares ISA

- Global ETFs

His allocation:

| Asset | Allocation |

|---|---|

| Global Stocks | 65% |

| Bonds | 25% |

| REITs | 5% |

| Cash | 5% |

James reduces technology stock exposure after realizing overconcentration risk.

Portfolio Allocation in Your 50s

Retirement planning becomes serious.

Goals shift toward:

- Wealth preservation

- Income generation

- Lower volatility

- Retirement readiness

Typical Allocation

| Asset | Allocation |

|---|---|

| Stocks | 50–65% |

| Bonds | 30–45% |

| Cash | 5–10% |

Importance of Bonds

Bonds become more important because they provide:

- Stability

- Predictable income

- Lower volatility

- Diversification

Common bonds include:

- Government bonds

- Treasury bonds

- Corporate bonds

- Municipal bonds

Inflation Risk

Even older investors cannot ignore growth.

Inflation reduces purchasing power.

Example:

If inflation averages 3% annually:

genui{“math_block_widget_always_prefetch_v2”:{“content”:”FV = PV(1+i)^n”}}

Over 20 years, prices may nearly double.

This is why retirees still hold stocks.

Portfolio Allocation in Your 60s

Many investors retire during this stage.

Primary goals:

- Income generation

- Capital preservation

- Reduced volatility

Typical Allocation

| Asset | Allocation |

|---|---|

| Stocks | 40–60% |

| Bonds | 35–50% |

| Cash | 5–15% |

The Retirement Income Challenge

Retirees must balance:

- Growth

- Withdrawals

- Inflation

- Longevity risk

Longevity risk means outliving savings.

Since people may live 25–30 years after retirement, portfolios still need growth exposure.

Case Study: Australian Retiree

Michael, age 67, lives in Sydney.

He uses a Superannuation retirement account.

His portfolio:

| Asset | Allocation |

|---|---|

| Dividend Stocks | 35% |

| Bonds | 45% |

| REITs | 10% |

| Cash | 10% |

This allocation generates retirement income while reducing large drawdowns.

Portfolio Allocation in Your 70s and Beyond

At this stage:

- Capital preservation becomes critical

- Medical expenses may increase

- Income stability becomes essential

Typical Allocation

| Asset | Allocation |

|---|---|

| Stocks | 30–50% |

| Bonds | 40–60% |

| Cash | 10–20% |

However, allocation depends heavily on:

- Health

- Retirement income

- Pension availability

- Estate planning goals

Aggressive vs Conservative Allocation

Aggressive Portfolio

Characteristics:

- High stock allocation

- Higher volatility

- Higher growth potential

Example:

- 90% stocks

- 10% bonds

Suitable for:

- Young investors

- Long-term goals

- High risk tolerance

Conservative Portfolio

Characteristics:

- Higher bond allocation

- Lower volatility

- Lower growth

Example:

- 40% stocks

- 60% bonds

Suitable for:

- Retirees

- Short-term goals

- Low risk tolerance

Role of International Diversification

Many Tier-1 investors diversify globally.

Why?

Because economies perform differently.

Example:

If US markets struggle, international markets may perform better.

Common international exposure includes:

- Europe

- Asia-Pacific

- Emerging markets

Importance of Rebalancing

Rebalancing means restoring target allocation percentages.

Example:

Initial allocation:

- 70% stocks

- 30% bonds

After a stock rally:

- 80% stocks

- 20% bonds

Investor sells some stocks and buys bonds to restore balance.

Benefits:

- Controls risk

- Prevents overexposure

- Maintains discipline

Dollar-Cost Averaging

Dollar-cost averaging means investing fixed amounts regularly.

Example:

Monthly investment:

- $500 every month

Benefits:

- Reduces emotional investing

- Lowers timing risk

- Builds consistency

This strategy is popular in retirement accounts.

Behavioral Finance and Age

Human emotions influence investing decisions.

Common emotional mistakes:

| Bias | Description |

|---|---|

| Fear | Selling during crashes |

| Greed | Buying speculative assets |

| Overconfidence | Excessive trading |

| Panic | Emotional decisions |

Older investors often become more conservative emotionally, even if financially capable of taking risk.

Common Portfolio Allocation Mistakes

1. Taking Too Much Risk

Example:

Near-retirement investors holding 100% stocks may suffer major losses during downturns.

2. Taking Too Little Risk

Holding excessive cash may fail to beat inflation.

3. Ignoring Diversification

Concentrated portfolios increase risk.

Example:

Owning only technology stocks during the Dot-com Bubble exposed investors to massive losses.

4. Emotional Investing

Selling during bear markets locks in losses.

5. No Rebalancing

Without rebalancing, risk exposure may become excessive.

The Role of Index Funds

Index funds are extremely popular in Tier-1 countries.

Reasons:

- Low fees

- Broad diversification

- Passive management

- Long-term efficiency

Popular indexes include:

| Index | Country |

|---|---|

| S&P 500 | USA |

| FTSE 100 | UK |

| TSX Composite | Canada |

| ASX 200 | Australia |

Active vs Passive Investing

Active Investing

Professional managers attempt to outperform markets.

Advantages:

- Potential higher returns

- Tactical flexibility

Disadvantages:

- Higher fees

- Underperformance risk

Passive Investing

Passive investors track market indexes.

Advantages:

- Lower costs

- Simplicity

- Tax efficiency

Disadvantages:

- No market outperformance

Many retirement portfolios now favor passive investing.

Tax Considerations by Age

Taxes strongly influence allocation decisions.

Examples:

| Country | Tax-Advantaged Accounts |

|---|---|

| USA | Roth IRA, 401(k) |

| UK | ISA |

| Canada | TFSA |

| Australia | Superannuation |

These accounts help reduce taxes and improve compounding.

Real Estate in Portfolio Allocation

Real estate provides:

- Rental income

- Diversification

- Inflation protection

Investors may own:

- Physical property

- REITs

- Real estate funds

However, real estate also carries:

- Illiquidity risk

- Maintenance costs

- Interest rate sensitivity

How Inflation Changes Age-Based Allocation

Inflation affects retirees heavily because fixed incomes lose purchasing power.

Therefore:

- Younger investors focus on growth

- Older investors balance growth and stability

Even retirees often maintain 30–50% stock exposure.

Technology and Modern Portfolio Management

Technology transformed investing.

Examples include:

- Robo-advisors

- Automated rebalancing

- AI portfolio analysis

- ETF investing

Companies like Betterment and Wealthfront automatically adjust allocation based on age and goals.

Case Study: Multi-Generational Family

Grandfather (72)

Allocation:

- 35% stocks

- 50% bonds

- 15% cash

Goal:

Capital preservation

Father (45)

Allocation:

- 70% stocks

- 25% bonds

- 5% cash

Goal:

Retirement growth

Son (24)

Allocation:

- 90% stocks

- 10% bonds

Goal:

Maximum long-term growth

This example shows how age changes investment priorities.

Sample Allocation Models

Conservative Model

| Asset | Allocation |

|---|---|

| Stocks | 40% |

| Bonds | 50% |

| Cash | 10% |

Moderate Model

| Asset | Allocation |

|---|---|

| Stocks | 60% |

| Bonds | 35% |

| Cash | 5% |

Aggressive Model

| Asset | Allocation |

|---|---|

| Stocks | 85% |

| Bonds | 10% |

| Cash | 5% |

How Economic Conditions Affect Allocation

Interest rates, inflation, and recessions influence allocation decisions.

Example:

During high inflation:

- Investors may increase commodity exposure

- Bond performance may weaken

- Real assets become attractive

During recessions:

- Defensive sectors gain popularity

- Investors may increase bond allocation

The Psychology of Retirement Investing

Retirement investing is emotional.

Major fears include:

- Running out of money

- Market crashes

- Medical expenses

- Inflation

Therefore, older investors often prefer stability even at the cost of lower returns.

Key Lessons About Portfolio Allocation by Age

1. Age Matters

Investment strategies should evolve with life stages.

2. Risk Changes Over Time

Younger investors can usually handle greater volatility.

3. Diversification Is Essential

Spreading investments reduces portfolio risk.

4. Inflation Cannot Be Ignored

Even retirees need growth assets.

5. Rebalancing Maintains Discipline

Regular reviews help maintain target allocation.

Conclusion

Portfolio allocation by age is a dynamic investment strategy that adjusts risk exposure according to an investor’s stage of life, financial goals, and retirement timeline.

Young investors generally focus on aggressive growth through stocks because they have time to recover from downturns. Middle-aged investors balance growth with stability as retirement approaches. Retirees prioritize income, preservation, and inflation protection while still maintaining some growth exposure.

In developed economies like the United States, United Kingdom, Canada, and Australia, age-based allocation is central to retirement planning systems and long-term wealth management.

The most successful investors understand that portfolio allocation is not static. It evolves with:

- Age

- Income

- Economic conditions

- Retirement goals

- Risk tolerance

- Market conditions

Ultimately, successful investing is not only about maximizing returns. It is about building a portfolio that matches personal goals, survives market volatility, and supports long-term financial security throughout every stage of life.