1. Introduction: Why Monthly Passive Income Matters More Than Ever

How to Build a Monthly Passive Income Portfolio (2026 Guide)

A monthly passive income portfolio is one of the most powerful financial strategies you can build in 2026.

Instead of relying solely on a paycheck, a monthly passive income portfolio allows your investments to generate consistent cash flow every month. This income can come from dividend stocks, REITs, bonds, rental properties, and other income-producing assets.

Across Tier-1 countries like the United States, United Kingdom, Canada, Australia, and Western Europe, more people are building a monthly passive income portfolio to protect themselves from inflation, job instability, and rising living costs.

In this guide, you’ll learn how to build a diversified monthly passive income portfolio that produces reliable cash flow and long-term financial freedom.

For decades, people believed that:

- A stable job

- A pension

- A savings account

were enough to guarantee financial comfort.

Today, this model no longer works.

Across Tier-1 countries—such as the United States, United Kingdom, Canada, Australia, and Western Europe—households are facing:

- Rising inflation, which silently erodes purchasing power

- Job insecurity, due to automation, outsourcing, and AI

- High housing costs, making homeownership and rent increasingly unaffordable

- Longer life expectancy, requiring retirement income to last 30–40 years

In this environment, relying solely on a paycheck is risky. What you need is income that does not depend on your time—income that continues even when you stop working.

This is where monthly passive income becomes transformational.

What Does “Monthly Passive Income” Mean?

Monthly passive income is money that:

- Arrives every month, like a salary

- Comes from investments or systems, not active labor

- Continues even when you are not working

Examples include:

- Dividends paid monthly from stocks or ETFs

- Rental income from property

- Interest from bonds

- Royalties from digital products

Instead of waiting for quarterly or annual payments, monthly income provides:

- Predictable cash flow

- Psychological stability

- Better budgeting

- Lower financial stress

Imagine this scenario:

On the 1st of every month, you receive:

- $500 from dividends

- $700 from rental property

- $300 from bonds

- $200 from royalties

That’s $1,700/month—without working a single hour.

This income can:

- Pay your rent or mortgage

- Cover groceries and utilities

- Fund vacations

- Build long-term wealth

- Allow you to work by choice, not necessity

This guide will show you—step by step—how to build a sustainable, diversified, tax-efficient, and inflation-resistant passive income portfolio that pays you every month.

What Is a Monthly Passive Income Portfolio?

A monthly passive income portfolio is a collection of income-producing investments that generate consistent cash flow every month. These assets may include dividend stocks, REITs, bonds, dividend ETFs, and rental properties. The goal of a monthly passive income portfolio is to provide reliable income without requiring active daily work.

2. What Is a Monthly Passive Income Portfolio? (And What It Is Not)

Before building passive income, it is critical to understand what the term truly means—and what it does not.

✅ Passive Income (True Definition)

Passive income is money that continues to flow after the initial work or investment is complete, with minimal ongoing effort.

You trade:

- Time + money today

for - Income tomorrow

Examples of true passive income:

| Source | Why It’s Passive |

|---|---|

| Dividends | Company pays you automatically |

| Rental property (with manager) | Rent arrives monthly |

| Bonds | Interest paid on schedule |

| Royalties | Product sells without your involvement |

| Index fund income | Managed automatically |

Passive income still requires:

- Initial setup

- Monitoring

- Occasional adjustments

But it does not require daily labor.

❌ What Passive Income Is NOT

Many people mistakenly label active income as passive.

These are not passive:

- Day trading

- Freelancing

- Gig work (Uber, delivery apps, etc.)

- Running a business that requires daily operations

- Flipping houses

These income streams depend on your continued effort. When you stop working, the income stops.

True passive income continues whether you:

- Sleep

- Travel

- Take time off

- Retire

Why Monthly Passive Income Is Special

Most investments pay:

- Quarterly (every 3 months)

- Semi-annually

- Annually

Monthly income is superior because it:

- Mimics a paycheck

- Smooths cash flow

- Reduces budgeting stress

- Improves financial predictability

This predictability is not just financial—it is psychological.

3. The Psychology of Monthly Cash Flow

Money is not just math—it is deeply emotional.

Financial stress is one of the leading causes of:

- Anxiety

- Depression

- Relationship conflict

- Burnout

Monthly passive income changes your mental relationship with money.

Psychological Benefits of Monthly Income

When income arrives every month automatically:

- You stop obsessing over your job.

- You stop panicking during market downturns.

- You stop fearing emergencies.

- You stop thinking in scarcity.

Instead, you think in:

- Systems, not paychecks

- Streams, not salaries

- Long-term strategies, not short-term survival

This mental shift leads to:

- Better financial decisions

- Reduced stress

- Higher risk tolerance in career and entrepreneurship

- Increased life satisfaction

Monthly income creates emotional stability, which is often more valuable than the money itself.

How to Build a Monthly Passive Income Portfolio (Explained)

4. The Three Pillars of a Successful Monthly Passive Income Portfolio

Every successful monthly income portfolio is built on three foundational pillars:

1️⃣ Stability

Stability means:

- Income arrives consistently

- Cash flow is predictable

- Income does not collapse during market volatility

Stable income sources include:

- Bonds

- Dividend ETFs

- Rental real estate

- Utilities and consumer staples stocks

Without stability, your income becomes unreliable—and unreliable income creates stress.

2️⃣ Growth

Growth ensures that:

- Your income increases over time

- Your purchasing power keeps up with inflation

- Your lifestyle improves, not stagnates

Growth comes from:

- Dividend growth stocks

- Real estate appreciation

- Business income

- Reinvested dividends

Without growth, inflation slowly destroys your income.

3️⃣ Diversification

Diversification means:

- Income comes from multiple sources

- You are not dependent on one asset, one company, or one market

- Risk is spread across sectors, industries, and geographies

Without diversification, one failure can destroy your income.

The Balance

A strong portfolio blends:

- Stable income

- Growing income

- Diverse income

Sacrificing any one of these makes your portfolio fragile.

5. Step 1: Assess Your Financial Foundation

Before investing, you must stabilize your financial base. Passive income is built on financial security, not financial chaos.

A. Emergency Fund

An emergency fund is money set aside for:

- Medical emergencies

- Job loss

- Unexpected expenses

- Car repairs

- Home repairs

You should have 3–6 months of living expenses in a high-yield savings account.

Example:

- Monthly expenses: $3,000

- Emergency fund target: $9,000–$18,000

Why this matters:

- It prevents you from selling investments during market downturns.

- It protects your passive income strategy.

- It gives you peace of mind.

B. High-Interest Debt

Debt with interest rates above 8–10% usually outpaces investment returns.

Pay off:

- Credit card debt

- Payday loans

- High-interest personal loans

Example:

- Credit card interest: 22%

- Investment return: 7%

- Paying off debt gives you a guaranteed 22% return—better than any investment.

Eliminating high-interest debt is the first step to building wealth.

C. Insurance Coverage

Insurance protects your financial system.

Ensure you have:

- Health insurance

- Disability insurance

- Life insurance (if you have dependents)

- Property insurance (home, rental, auto)

Passive income works only when your financial foundation is protected from catastrophic risk.

6. Step 2: Define Your Monthly Income Target

You cannot build what you do not define.

You must set a clear, measurable monthly income goal.

Step 1: Determine Your Expenses

List:

- Housing

- Utilities

- Food

- Transportation

- Insurance

- Entertainment

- Savings

- Travel

Example:

- Total monthly expenses: $3,500

Step 2: Define Your Income Goal

Decide:

- Do you want to supplement income?

- Replace income?

- Achieve full financial independence?

Example Goals:

| Goal | Monthly Target | Annual Target |

|---|---|---|

| Supplement income | $500 | $6,000 |

| Cover bills | $1,500 | $18,000 |

| Financial independence | $4,000 | $48,000 |

| Early retirement | $7,000+ | $84,000+ |

Step 3: Backward Calculation

To determine how much capital you need:

Formula:

Required Capital = Annual Income ÷ Expected Yield

Example:

- Desired income: $48,000/year

- Expected yield: 5%

$48,000 ÷ 0.05 = $960,000

This means you need approximately $960,000 invested to generate $4,000/month at a 5% yield.

This may sound intimidating—but:

- You don’t need it today.

- You build it over time.

- Compounding works exponentially.

How Much Money Do You Need for a Monthly Passive Income Portfolio?

The amount needed for a monthly passive income portfolio depends on your income goal and expected investment yield. For example, if you want $4,000 per month and your portfolio yields 5%, you would need approximately $960,000 invested.

7. Step 3: Understand Yield vs. Risk vs. Stability

This is one of the most misunderstood areas of investing.

Yield = Income Return

Yield is the percentage of income you earn on your investment.

Formula:

Yield = Annual Income ÷ Investment Amount

Example:

- Investment: $10,000

- Annual income: $500

Yield = $500 ÷ $10,000 = 5%

The Yield Trap

Many investors chase high yields (8%, 10%, 12%+) without understanding the risk.

High yield often means:

- The company is struggling

- The dividend may be cut

- The investment is highly volatile

- The income is not sustainable

This leads to:

- Income collapse

- Capital loss

- Emotional panic

- Long-term financial damage

The Ideal Balance

A strong monthly income portfolio targets:

- Moderate yield (4–7%)

- High reliability

- Long-term growth

This creates income that is:

- Sustainable

- Predictable

- Inflation-resistant

8. Step 4: Core Assets for a Monthly Passive Income Portfolio

These are the backbone of your monthly income portfolio.

🟢 Dividend Stocks

Dividend stocks are shares of companies that distribute a portion of their profits to shareholders.

How Dividend Stocks Work

- You buy shares in a company.

- The company earns profits.

- The company distributes part of those profits as dividends.

- You receive cash—usually quarterly or monthly.

Example:

- You invest $10,000 in a stock yielding 4%.

- Annual income = $400.

- Quarterly payments = $100 each.

- Some stocks pay monthly.

Best Dividend Sectors:

| Sector | Why It’s Reliable |

|---|---|

| Utilities | Essential services |

| Consumer staples | Everyday necessities |

| Healthcare | Non-discretionary demand |

| Telecommunications | Subscription-based income |

| Financials | Stable cash flow |

Benefits of Dividend Stocks:

- Income + capital appreciation

- Inflation protection

- Tax advantages (qualified dividends in the U.S.)

- Liquidity (easy to buy and sell)

Risks:

- Dividend cuts during recessions

- Market volatility

- Company-specific risk

- Sector downturns

🟢 REITs (Real Estate Investment Trusts)

REITs own and operate income-producing real estate and distribute at least 90% of taxable income to shareholders.

Why REITs Are Powerful

REITs provide:

- High yields (4–8%)

- Monthly or quarterly payments

- Real estate exposure without owning property

- Liquidity (publicly traded)

Types of REITs:

| Type | Example Properties |

|---|---|

| Residential | Apartments, single-family rentals |

| Commercial | Office buildings, retail centers |

| Industrial | Warehouses, logistics centers |

| Healthcare | Hospitals, medical offices |

| Data centers | Cloud storage facilities |

| Self-storage | Storage facilities |

Example:

- Investment: $20,000

- Yield: 6%

- Annual income: $1,200

- Monthly income: $100

Risks:

- Interest rate sensitivity

- Property market downturns

- Tenant risk

- Sector-specific declines

🟢 Bonds and Bond Funds

Bonds are loans you give to:

- Governments

- Corporations

- Municipalities

In return, you receive interest payments.

Types of Bonds:

| Type | Risk Level | Yield |

|---|---|---|

| Government bonds | Low | Low |

| Corporate bonds | Medium | Medium |

| Municipal bonds | Low–Medium | Low–Medium |

| High-yield bonds | High | High |

Benefits:

- Predictable income

- Lower volatility than stocks

- Capital preservation

- Portfolio stability

Drawbacks:

- Lower returns

- Inflation risk

- Interest rate risk

Bond funds and ETFs offer diversification and monthly distributions.

🟢 High-Yield Savings & Money Market Funds

These are low-risk, highly liquid cash-like investments.

Benefits:

- Capital preservation

- High liquidity

- Stable income

- Ideal for emergency funds

Drawbacks:

- Low yields

- Do not beat inflation over the long term

Best used as:

- Emergency fund storage

- Short-term income buffer

- Capital preservation

🟢 Dividend ETFs

Dividend ETFs bundle many dividend-paying stocks into a single fund.

Benefits:

- Instant diversification

- Professional management

- Lower risk than individual stocks

- Some pay monthly

Example:

- Invest $10,000 in a dividend ETF yielding 4%.

- Annual income = $400.

- Monthly income (if monthly ETF) ≈ $33.

9. Step 5: Alternative Monthly Income Streams

Once your core income is stable, you can add alternative income streams for higher yield and diversification.

🟡 Rental Real Estate

Rental property is one of the most powerful passive income generators.

Income Sources:

- Monthly rent

- Property appreciation

- Tax deductions

- Inflation hedging

Example:

- Purchase price: $250,000

- Down payment: $50,000

- Monthly rent: $1,800

- Monthly expenses: $1,200

- Net income: $600/month

Risks:

- Vacancies

- Maintenance costs

- Tenant issues

- Market downturns

Property managers can reduce workload, making income more passive.

🟡 Peer-to-Peer (P2P) Lending

You lend money to individuals or businesses through online platforms.

Returns:

- Typically 6–12%

Risks:

- Borrower defaults

- Platform risk

- Liquidity risk

- Economic downturns

Best used as a small portion of your portfolio.

🟡 Royalties

Royalties are recurring payments from intellectual property.

Sources:

- Books

- Courses

- Music

- Software

- Apps

- Digital products

Example:

- Create an online course.

- Sell for $100.

- Sell 50 copies/month = $5,000/month.

- Ongoing income with minimal maintenance.

🟡 Business Income

Owning a business that runs without your daily involvement can produce monthly income.

Examples:

- E-commerce stores

- SaaS businesses

- Franchises

- Content websites

- Licensing businesses

Benefits:

- High scalability

- High income potential

- Business equity growth

Risks:

- Operational risk

- Market competition

- Economic downturns

10. Step 6: Best Asset Allocation for a Monthly Passive Income Portfolio

A well-structured monthly passive income portfolio focuses on stable income sources that pay regularly.

The goal of a monthly passive income portfolio is to create predictable cash flow without relying on active work.

Diversification is essential when building a monthly passive income portfolio because income should come from multiple assets.

As your monthly passive income portfolio grows, reinvesting dividends accelerates compounding. Asset allocation determines:

- Risk

- Return

- Income stability

- Growth potential

Sample Allocation (Balanced Investor):

| Asset Class | Allocation | Purpose |

|---|---|---|

| Dividend Stocks | 30% | Growing income + dividends |

| REITs | 20% | High yield real estate income |

| Bonds | 20% | Stability and lower volatility |

| Dividend ETFs | 15% | Diversification and passive management |

| Real Estate | 10% | Inflation hedge and rental income |

| Alternative Income | 5% | P2P lending, royalties, etc. |

How to Adjust Allocation:

| Factor | Adjustment |

|---|---|

| Younger investor | Increase growth assets |

| Older investor | Increase stable income assets |

| Low risk tolerance | Increase bonds and ETFs |

| High risk tolerance | Increase real estate and alternatives |

| Need income now | Increase yield-focused assets |

Monthly Passive Income Portfolio Example

| Investment | Amount | Yield | Monthly Income |

|---|---|---|---|

| Dividend Stocks | $50,000 | 4% | $167 |

| REITs | $30,000 | 6% | $150 |

| Bonds | $20,000 | 3% | $50 |

Total Monthly Passive Income: $367

11. Step 7: Tax Efficiency for Tier-1 Countries

Taxes can destroy your passive income if not managed properly.

🇺🇸 United States

- Qualified dividends: 0–20% tax

- REIT income: Ordinary income tax

- Use tax-advantaged accounts:

- IRA

- Roth IRA

- 401(k)

🇬🇧 United Kingdom

- Dividend allowance

- ISA accounts for tax-free income

- Property income taxed separately

🇨🇦 Canada

- Dividend tax credit

- TFSA for tax-free growth

- RRSP for tax-deferred growth

🇦🇺 Australia

- Franking credits

- Superannuation accounts

- Capital gains discounts

🇪🇺 Western Europe

- Tax rules vary by country

- Use tax shelters where available

- Consult a tax advisor

12. Step 8: Automation & Reinvestment Strategy

Automation is the secret to building wealth without relying on motivation.

A. Automatic Contributions

Set up automatic monthly investments:

- From paycheck

- From bank account

- Into brokerage accounts

B. Dividend Reinvestment Plans (DRIPs)

DRIPs automatically reinvest dividends, accelerating compounding.

Example:

- Dividend income: $100/month

- Reinvested at 6% yield

- Over 20 years, reinvestment alone can double your income.

C. Rebalance Annually

Rebalancing:

- Restores target asset allocation

- Reduces risk

- Improves long-term returns

The Power of Reinvesting Passive Income

Reinvesting passive income is one of the most powerful ways to accelerate wealth creation.

Instead of spending dividends, interest, or rental income, investors reinvest that income

back into their portfolio to purchase more assets.

Over time, this creates a compounding effect where both the original investment and the

reinvested income generate additional returns.

Where:

- A = Final value of investment

- P = Initial investment

- r = Annual return rate

- n = Number of compounding periods per year

- t = Number of years invested

This formula explains how income reinvestment accelerates portfolio growth.

When dividends, interest, or rental income are reinvested, the earnings start generating additional returns. Over long periods, this compounding effect significantly increases both the portfolio value and monthly passive income.

Passive Income Compounding Growth Example

Assume:

Income reinvested every year

Initial investment: $100,000

Annual return: 5%

| Year | Portfolio Value | Annual Passive Income | Monthly Income |

|---|---|---|---|

| 1 | $105,000 | $5,250 | $437 |

| 5 | $127,628 | $6,381 | $531 |

| 10 | $162,889 | $8,144 | $678 |

| 20 | $265,329 | $13,266 | $1,105 |

| 30 | $432,194 | $21,609 | $1,800 |

Over time, the portfolio more than quadruples, dramatically increasing passive income.

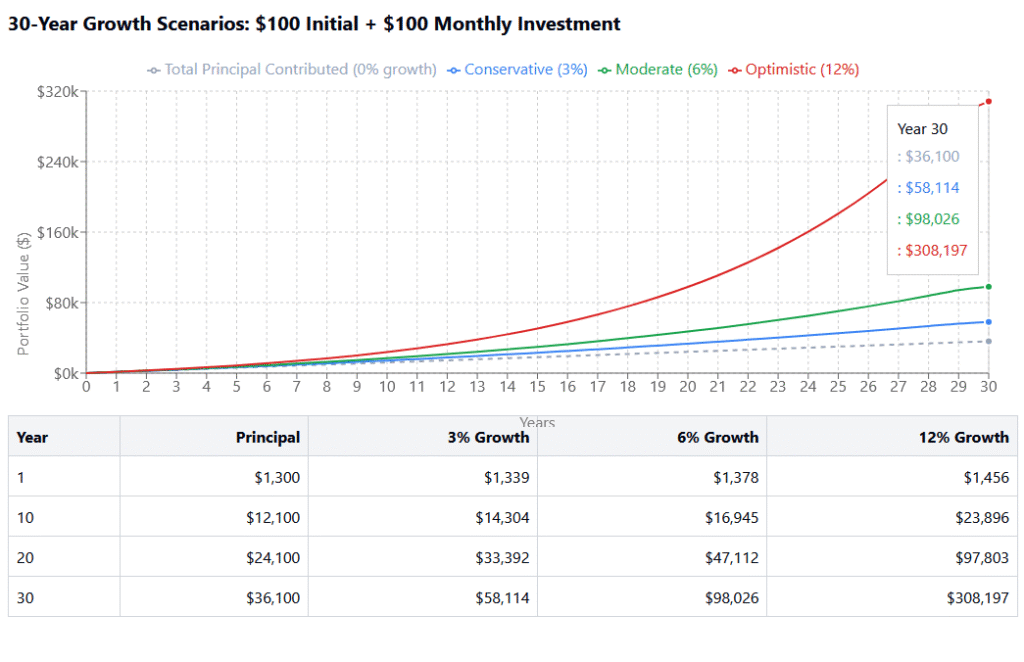

Chart Concept for Your Article

Create a line chart like this:

X-Axis: Years (0–30)

Y-Axis: Portfolio Value

Growth curve:

- Year 0 → $100k

- Year 10 → ~$163k

- Year 20 → ~$265k

- Year 30 → ~$432k

The curve should start slowly and accelerate upward, showing compounding.

13. Step 9: Inflation-Proofing Your Income

Inflation erodes purchasing power.

Example:

- $1,000/month today

- At 3% inflation, equivalent to $553/month in 20 years.

How to Protect Against Inflation:

- Invest in dividend growth stocks

- Own real assets (real estate, commodities)

- Avoid relying solely on fixed-income assets

Your goal: Income that grows faster than inflation.

14. Step 10: Risk Management and Diversification

Risk management protects your income during downturns.

Key Risk Management Principles:

- Never rely on one income source

- Diversify across:

- Asset classes

- Industries

- Geographies

- Income types

- Maintain emergency fund

- Avoid excessive leverage

Risk Management Tools:

- Position sizing

- Asset allocation

- Rebalancing

- Stop-loss orders (sparingly)

- Insurance

15. Sample Monthly Income Portfolios

🟢 Beginner Portfolio ($10,000)

| Asset | Amount | Yield | Monthly Income |

|---|---|---|---|

| Dividend ETF | $4,000 | 4% | $13 |

| REIT ETF | $3,000 | 6% | $15 |

| Bond Fund | $2,000 | 3% | $5 |

| High-Yield Savings | $1,000 | 4% | $3 |

| Total | $10,000 | — | $36/month |

🟡 Intermediate Portfolio ($100,000)

| Asset | Amount | Yield | Monthly Income |

|---|---|---|---|

| Dividend Stocks | $30,000 | 4% | $100 |

| REITs | $20,000 | 6% | $100 |

| Bonds | $20,000 | 3% | $50 |

| ETFs | $20,000 | 4% | $67 |

| Real Estate | $10,000 | 8% | $67 |

| Total | $100,000 | — | $384/month |

🔵 Advanced Portfolio ($1,000,000)

| Asset | Amount | Yield | Monthly Income |

|---|---|---|---|

| Dividend Stocks | $300,000 | 4% | $1,000 |

| REITs | $200,000 | 6% | $1,000 |

| Bonds | $200,000 | 3% | $500 |

| ETFs | $200,000 | 4% | $667 |

| Real Estate | $100,000 | 8% | $667 |

| Total | $1,000,000 | — | $3,834/month |

16. Common Mistakes That Kill Passive Income

- Chasing high yield without understanding risk

- Over-concentrating in one asset or sector

- Ignoring taxes

- Failing to reinvest

- Panicking during market downturns

- Not adjusting for inflation

- Lack of diversification

Avoid these mistakes, and your income will grow safely.

17. Real-Life Case Study: From $0 to $5,000/month

Meet Sarah, 34, Marketing Manager (USA)

- Starting savings: $15,000

- Monthly investment: $1,500

- Strategy: Dividend ETFs, REITs, rental property

Year 1:

- Portfolio: $33,000

- Monthly income: $110

Year 5:

- Portfolio: $135,000

- Monthly income: $520

Year 10:

- Portfolio: $420,000

- Monthly income: $1,800

Year 15:

- Portfolio: $780,000

- Monthly income: $3,500

Year 18:

- Portfolio: $1,000,000+

- Monthly income: $5,000+

Sarah achieved financial independence before age 52—without inheritance, speculation, or luck.

18. How Long Does It Take to Build a Monthly Passive Income Portfolio?

Timeline depends on:

- Savings rate

- Investment returns

- Income goals

- Starting capital

Estimated Timelines:

| Monthly Income Goal | Aggressive Saver | Average Saver |

|---|---|---|

| $500/month | 2–4 years | 4–7 years |

| $2,000/month | 5–8 years | 8–12 years |

| $5,000/month | 10–15 years | 15–25 years |

Passive Income Portfolio Growth Timeline diagram shows how a portfolio evolves from starting investor → financial independence.

Passive Income Portfolio Growth Timeline

Stage 1 — Foundation (Years 0–2)

Goal: Build the base of your portfolio

Focus on:

- Building an emergency fund

- Starting with index funds or dividend ETFs

- Investing consistently every month

Example:

| Investment | Amount |

|---|---|

| Savings | $10,000 |

| Dividend ETFs | $5,000 |

| Bonds | $3,000 |

Monthly passive income:

$50–$100

Main objective:

Develop the habit of investing.

Stage 2 — Income Acceleration (Years 3–7)

Goal: Grow dividend income

Portfolio expansion:

- Dividend stocks

- REITs

- Bond funds

- Real estate crowdfunding

Example portfolio:

| Asset | Value |

|---|---|

| Dividend Stocks | $40,000 |

| REITs | $20,000 |

| Bond Funds | $15,000 |

| Dividend ETFs | $25,000 |

Monthly passive income:

$300–$700

Strategy:

✔ reinvest dividends

✔ increase monthly contributions

✔ diversify income sources

Stage 3 — Income Growth (Years 8–15)

Goal: Let compounding work

Portfolio example:

| Asset | Value |

|---|---|

| Dividend Stocks | $150,000 |

| REITs | $60,000 |

| Bond Funds | $50,000 |

| ETFs | $100,000 |

Monthly passive income:

$1,500–$3,000

At this stage:

- dividends increase every year

- compounding accelerates

- income becomes meaningful

Stage 4 — Financial Independence (Years 15–25)

Goal: Income replaces salary

Portfolio size example:

| Asset | Value |

|---|---|

| Dividend Stocks | $400,000 |

| REITs | $150,000 |

| Bonds | $200,000 |

| ETFs | $250,000 |

Monthly passive income:

$4,000–$8,000

This level can cover:

- housing

- food

- healthcare

- travel

Stage 5 — Wealth Expansion (25+ Years)

Goal: Generational wealth

Portfolio example:

| Asset | Value |

|---|---|

| Dividend Stocks | $800,000 |

| REITs | $300,000 |

| Bonds | $400,000 |

| ETFs | $500,000 |

Monthly passive income:

$10,000+

At this stage:

- passive income exceeds expenses

- wealth continues growing

- assets can be passed to future generations

19. Frequently Asked Questions

❓ Is passive income truly passive?

Not entirely. It requires setup, monitoring, and occasional adjustments—but far less effort than active income.

❓ Can I live off dividends alone?

Yes, with sufficient capital, diversification, and reinvestment.

❓ Should I prioritize growth or income?

- Early years: prioritize growth.

- Later years: prioritize income.

❓ Is real estate better than stocks?

Neither is universally better. The strongest portfolios combine both.

❓ Can I start with $100?

Yes. Many platforms allow fractional investing and micro-investing.

20. Final Thoughts: Build Your Monthly Passive Income Portfolio

Building a monthly passive income portfolio is one of the most powerful steps toward financial independence.

Instead of trading time for money forever, a monthly passive income portfolio allows your investments to generate reliable income every month.

By combining dividend stocks, REITs, bonds, ETFs, and real estate, you can build a diversified monthly passive income portfolio that grows over time.

Start small, stay consistent, reinvest your income, and allow compounding to do the heavy lifting.

The sooner you start building your monthly passive income portfolio, the sooner your money begins working for you.