1. Introduction: The Power of Passive Income Through Dividends

Dividend investing strategy is one of the most powerful ways to build passive income and long-term financial independence. Instead of relying solely on salary or active work, investors can create a system where their money generates consistent cash flow through dividend payments.

A well-designed dividend investing strategy allows investors to turn their portfolio into a long-term passive income machine that generates cash flow even during market volatility.

Imagine waking up every morning and discovering that income has quietly arrived in your brokerage account overnight. That is the power of a well-designed dividend investing strategy.

You didn’t have to work extra hours, negotiate a raise, sell a product, or trade stocks. The income simply showed up — automatically, predictably, and repeatedly.

That is the essence of dividend investing.

In 2026, financial independence is no longer just a dream for the wealthy. Middle-class families, young professionals, freelancers, and retirees alike are searching for reliable income streams that do not require constant effort. Traditional savings accounts no longer protect purchasing power because inflation steadily erodes the value of cash. Job security is uncertain, and market volatility can feel emotionally exhausting.

Dividend investing offers something rare:

Income + Stability + Growth + Psychological peace.

For investors in Tier-1 countries — including the United States, United Kingdom, Canada, Australia, and Western Europe — dividend investing is especially powerful because:

- Financial markets are well-regulated and transparent.

- Many companies have decades-long histories of paying and increasing dividends.

- Tax-advantaged investment accounts allow dividends to grow faster.

- Long-term economic growth supports business profitability and sustainability.

Dividend investing is not a shortcut to riches. Instead, it is a systematic wealth-building strategy that rewards discipline, patience, and long-term thinking. It turns your money into a productive asset that works for you around the clock.

This guide will teach you everything — from the most basic concepts to advanced strategies — so you can design a dividend portfolio that pays you for life.

2. What Is Dividend Investing? (Explained Simply)

At its core, dividend investing means buying shares of companies that regularly share part of their profits with shareholders in the form of dividends.

A dividend is a cash payment (or sometimes stock payment) made by a company to its shareholders, usually on a regular schedule (quarterly, semi-annually, or monthly).

In Simple Terms:

Instead of relying only on stock prices going up so you can sell later, dividend investing allows you to:

- Get paid just for owning the stock, and

- Continue getting paid even if you never sell.

This transforms investing from a speculative activity into an income-generating system.

Example:

Suppose you buy:

- 100 shares of a company paying $1 per share per year in dividends.

That means:

- You receive $100 per year in cash income.

Now, if the company increases its dividend to $1.10 per share next year:

- Your income rises to $110 per year, without buying more shares.

That’s called dividend growth — and it’s one of the most powerful wealth-building forces in investing.

What Can You Do With Dividends?

You can:

- Spend them to cover bills, rent, groceries, or travel.

- Reinvest them to buy more shares and grow future income.

- Save them to build financial security and emergency funds.

Dividend investing turns your portfolio into a cash-producing asset, similar to rental property — but without:

- Tenants

- Repairs

- Vacancies

- Property taxes

- Legal risks

Your “tenant” is the company — and it pays you simply for owning shares.

In essence, a dividend investing strategy focuses on generating consistent income from company profits rather than relying only on stock price appreciation.

3. How Dividends Work: The Mechanics Behind the Income

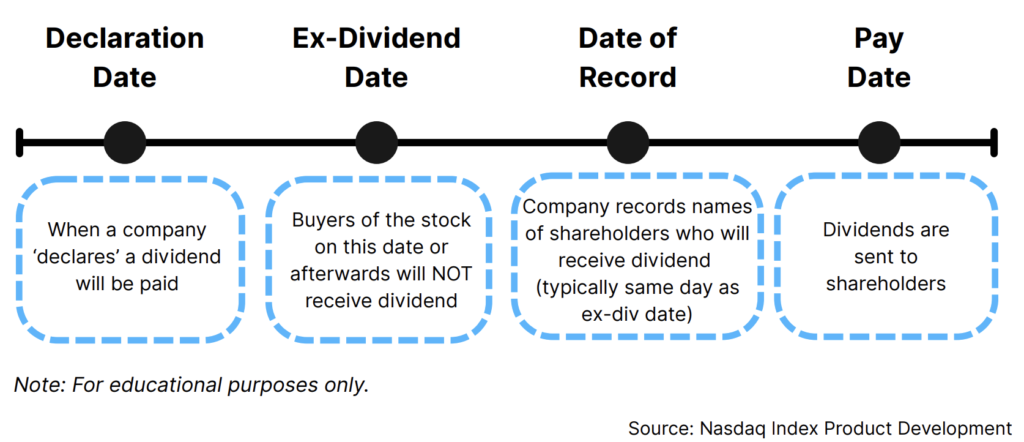

To truly master dividend investing, you must understand how dividend payments actually work. There are four key dividend dates every investor should know:

1️⃣ Declaration Date

This is when the company’s board of directors announces:

- The dividend amount

- The payment date

- The ex-dividend date

Once declared, the dividend becomes a legal obligation of the company.

2️⃣ Ex-Dividend Date

This is the most important date for investors.

If you buy the stock on or after the ex-dividend date, you will not receive the upcoming dividend.

If you own the stock before this date, you will receive the dividend.

3️⃣ Record Date

This is when the company checks its shareholder records to determine who is eligible to receive the dividend.

4️⃣ Payment Date

This is when the dividend is actually deposited into your brokerage account.

Example Timeline:

- Declaration Date: March 1

- Ex-Dividend Date: March 10

- Record Date: March 11

- Payment Date: March 25

If you purchase the stock on March 9, you receive the dividend.

If you purchase on March 10 or later, you do not.

How Often Are Dividends Paid?

- Quarterly – Most common in the U.S. and Canada

- Semi-annually – Common in the UK and Europe

- Monthly – Offered by some REITs, BDCs, and ETFs

Understanding this timing helps you plan cash flow and reinvestment strategies more effectively.

4. Why Dividend Investing Is Ideal for Tier-1 Investors

Dividend investing works everywhere, but it is especially powerful in developed economies because of structural advantages.

1️⃣ Strong Corporate Governance

Companies in Tier-1 markets operate under:

- Strict accounting standards

- Transparent financial reporting

- Regulatory oversight

This reduces the risk of:

- Fraud

- Misreported profits

- Unsustainable dividend promises

As a result, dividend payments are more reliable and predictable. Because of these advantages, building a dividend investing strategy in developed markets can provide both stability and long-term income growth.

2️⃣ Deep and Liquid Markets

In Tier-1 countries:

- You can buy and sell dividend stocks easily.

- There is always a buyer and seller.

- Bid-ask spreads are narrow.

This allows investors to:

- Rebalance portfolios efficiently.

- Exit positions without price manipulation.

3️⃣ Tax-Advantaged Investment Accounts

Governments in Tier-1 countries provide tax shelters that dramatically improve long-term returns.

Examples:

- USA: IRA, Roth IRA, 401(k)

- UK: ISA, SIPP

- Canada: TFSA, RRSP

- Australia: Superannuation

These accounts allow:

- Tax-free dividend income, or

- Tax-deferred compounding, which means more money stays invested and compounds faster.

4️⃣ Long-Term Economic Stability

Developed economies experience:

- Long-term GDP growth

- Strong consumer demand

- Stable legal systems

This supports:

- Corporate profitability

- Sustainable dividend growth

- Lower default risk

Dividend investing thrives in stable environments — which Tier-1 markets provide.

5. The Psychology of Dividend Income

One of the most underrated benefits of dividend investing is its psychological impact.

Most investors suffer emotionally during market downturns because:

- They rely entirely on stock prices rising.

- When prices fall, they feel like they are “losing money,” even if they haven’t sold.

- This leads to panic selling, market timing, and poor long-term decisions.

Dividend investors, however, experience something different.

Why Dividend Income Changes Investor Behavior:

- Even when markets fall, income continues.

- Cash keeps flowing into your account.

- This reinforces patience and long-term thinking.

Instead of asking:

“What is my portfolio worth today?”

Dividend investors ask:

“How much income did my portfolio generate this year?”

This mindset shift:

- Reduces stress

- Increases discipline

- Prevents emotional decisions

- Encourages long-term holding

It transforms investing from a speculative game into a business ownership mindset.

6. Types of Dividend Stocks

Not all dividend stocks are the same. Understanding the categories helps you build a diversified, resilient, and sustainable income portfolio.

🔹 1. Blue-Chip Dividend Stocks

Blue-chip stocks are large, well-established companies with:

- Strong brand recognition

- Stable earnings

- Long histories of dividend payments

These companies typically operate in essential industries such as:

- Consumer goods

- Healthcare

- Energy

- Financial services

Examples:

- Johnson & Johnson

- Coca-Cola

- Procter & Gamble

- Unilever

- Nestlé

These stocks offer:

- Reliable income

- Moderate yield

- Steady dividend growth

They form the foundation of most dividend portfolios.

🔹 2. Dividend Growth Stocks

These companies focus on:

- Consistently increasing their dividends over time

- Even if the current yield is modest

They often operate in:

- Technology

- Industrials

- Consumer discretionary

Dividend growth stocks offer:

- Lower initial income

- Higher long-term income growth

- Strong inflation protection

Over decades, these stocks often outperform high-yield stocks in total income.

🔹 3. High-Yield Dividend Stocks

These companies offer above-average dividend yields, often exceeding 6–8%.

However, high yield often signals:

- Business risk

- Earnings instability

- Financial distress

High-yield stocks must be analyzed carefully to ensure the dividend is sustainable.

🔹 4. REITs (Real Estate Investment Trusts)

REITs are companies that:

- Own income-producing real estate (offices, apartments, warehouses, data centers, retail, healthcare facilities).

- Are legally required to distribute most of their profits to shareholders.

Because of this structure, REITs often offer:

- High dividend yields

- Regular income

- Monthly or quarterly payments

Examples:

- Realty Income

- Digital Realty

- Public Storage

REITs provide real estate exposure without property ownership.

🔹 5. Utility Stocks

Utility companies provide essential services such as:

- Electricity

- Water

- Natural gas

They operate in regulated markets with:

- Predictable cash flows

- Stable demand

Utilities typically offer:

- Moderate yield

- Low volatility

- Reliable income

They act as a stability anchor in dividend portfolios.

7. Understanding Dividend Yield, Payout Ratio, and Growth Rate

These three metrics determine whether a dividend is attractive, sustainable, and profitable long-term.

1️⃣ Dividend Yield

Dividend yield measures how much income you receive relative to the stock price.

Formula:

Dividend Yield = Annual Dividend ÷ Stock Price

Example:

- Annual dividend = $2

- Stock price = $50

- Dividend yield = 4%

This means:

- You earn 4% per year in income, not counting price changes.

However:

- A high yield can signal distress.

- A falling stock price can artificially inflate yield.

Yield must always be evaluated alongside financial stability.

2️⃣ Payout Ratio

Payout ratio measures how much of a company’s earnings are paid out as dividends.

Formula:

Payout Ratio = Dividend ÷ Earnings

Example:

- Earnings per share = $5

- Dividend per share = $2

- Payout ratio = 40%

Interpretation:

- Below 60% → Generally sustainable

- 60–80% → Caution

- Above 80% → Risk of dividend cuts

REITs and utilities may have higher payout ratios due to business structure, but most companies should maintain conservative ratios.

3️⃣ Dividend Growth Rate

This measures how fast dividends increase annually.

Example:

- A company increases dividends by 6% per year.

Rule of 72:

- 72 ÷ 6 = 12 years

- Your dividend income doubles approximately every 12 years.

Dividend growth is critical because:

- It protects purchasing power from inflation.

- It compounds income over time.

8. Dividend Aristocrats, Kings, and Champions

Dividend Aristocrats are companies in the S&P 500 that have increased their dividends for at least 25 consecutive years. According to the S&P Global Dividend Aristocrats Index, these companies represent some of the most financially stable businesses in the market. These are elite groups of companies with extraordinary dividend track records.

🔹 Dividend Aristocrats

- 25+ consecutive years of dividend increases

- Must be part of the S&P 500

🔹 Dividend Kings

- 50+ consecutive years of dividend increases

🔹 Dividend Champions

- 25+ years of increases across the broader market

These companies have survived:

- Economic recessions

- Financial crises

- Wars

- Inflationary periods

- Market crashes

And still increased shareholder income.

They represent the gold standard of dividend reliability.

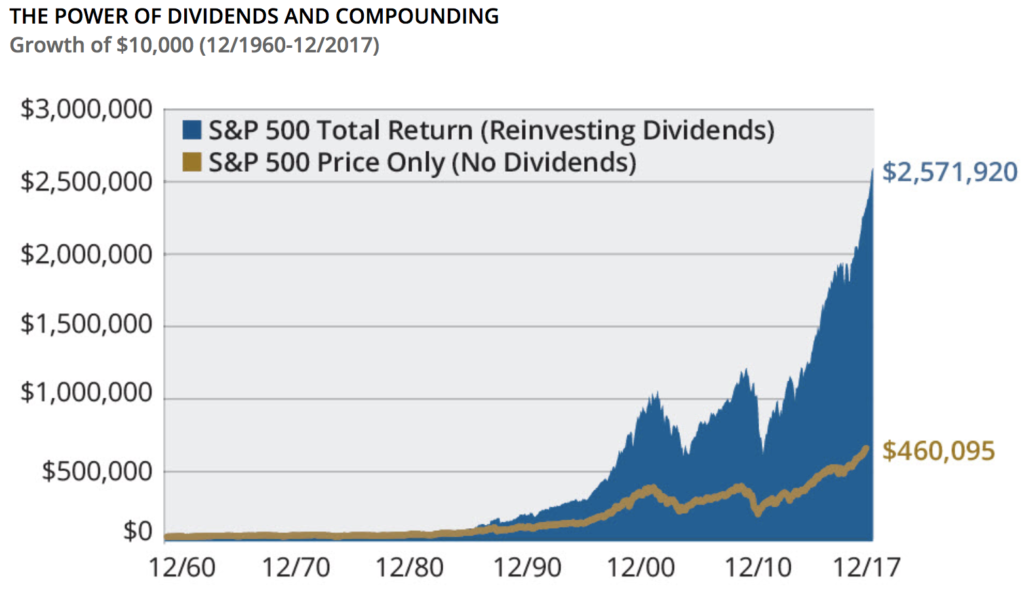

9. The Power of Compounding in a Dividend Investing Strategy

Dividend compounding occurs when you reinvest dividends to buy more shares, which then generate more dividends, creating a snowball effect.

This is the most powerful wealth-building mechanism in dividend investing.

What is Dividend Investing?

Dividend investing is a strategy where investors buy stocks that regularly pay cash distributions.

These payments create passive income that can supplement salary.

Investors who want to estimate their long-term returns can use the SEC compound interest calculator to simulate dividend reinvestment and portfolio growth over time.

Example:

- Initial investment: $10,000

- Dividend yield: 4% → $400/year

- Dividend growth: 6%

- Reinvest dividends annually

After 25 years:

- Portfolio value ≈ $54,000

- Annual income ≈ $2,200

- Total dividends received ≈ $30,000+

All from a single initial investment, without adding more money.

Why Compounding Is Exponential

In the early years:

- Growth feels slow.

In later years:

- Growth accelerates dramatically.

This is why:

- Time is more important than timing.

- Starting early matters more than investing large amounts later.

10. Dividend Reinvestment Plans (DRIPs)

A DRIP automatically reinvests your dividends into additional shares of the same stock.

Most brokerages and ETFs offer DRIPs with:

- No commissions

- Fractional shares

- Automatic execution

Benefits:

- Hands-free compounding

- Dollar-cost averaging

- Eliminates emotional decisions

DRIPs turn your portfolio into a self-reinforcing income machine. For long-term investors, DRIPs are a core component of an effective dividend investing strategy because they automate compounding.

11. Building a Dividend Investing Strategy Portfolio from Scratch

Step 1: Define Your Income Goal

Ask:

- How much income do I want annually?

- When do I want to receive it?

Example:

- Target income = $40,000/year

- Target yield = 4%

- Required portfolio = $1,000,000

This gives your investing a clear purpose. The best dividend investing strategy combines yield, dividend growth, and diversification across industries.

Step 2: Determine Your Risk Tolerance

- Higher yield → Higher risk

- Lower yield + higher growth → Lower risk

Your portfolio should match your:

- Emotional comfort

- Financial situation

- Time horizon

Step 3: Choose Your Asset Mix

A balanced dividend portfolio may include:

- 40% dividend growth stocks

- 25% REITs

- 20% high-quality high-yield stocks

- 15% dividend ETFs

This balances:

- Stability

- Income

- Growth

- Risk

Step 4: Invest Consistently

Invest:

- Monthly

- Quarterly

- Automatically

This approach:

- Reduces market timing risk

- Smooths entry prices

- Builds discipline

12. Asset Allocation for Dividend Investors

Asset allocation is the process of distributing your investments across different asset classes to manage risk and maximize returns. Proper diversification is a critical principle of any sustainable dividend investing strategy.

Example Allocation:

| Asset Class | Percentage |

|---|---|

| Blue-Chip Dividend Stocks | 35% |

| Dividend Growth Stocks | 25% |

| REITs | 20% |

| Dividend ETFs | 15% |

| Cash / Bonds | 5% |

This structure ensures:

- Income stability

- Growth potential

- Inflation protection

- Risk diversification

13. How Much Money Do You Need to Live Off Dividends?

One of the most common goals of a dividend investing strategy is to generate enough passive income to cover living expenses. The amount depends on:

- Lifestyle

- Location

- Spending habits

- Desired comfort

Example Scenarios:

🟢 Modest Lifestyle

- Annual expenses: $30,000

- Yield: 4%

- Required portfolio: $750,000

🔵 Comfortable Lifestyle

- Annual expenses: $50,000

- Yield: 4%

- Required portfolio: $1,250,000

🔴 High-Income Lifestyle

- Annual expenses: $80,000

- Yield: 4%

- Required portfolio: $2,000,000

These goals are achievable through:

- Consistent investing

- Dividend growth

- Compounding

- Tax-advantaged accounts

14. Dividend Investing for Different Life Stages

🔹 In Your 20s and 30s

Focus on:

- Dividend growth

- Lower yield, higher growth

- Full reinvestment

Goal: Maximize long-term compounding.

🔹 In Your 40s and 50s

Blend:

- Dividend growth

- Income stability

Goal: Increase income while preserving capital.

🔹 In Retirement

Focus on:

- Reliable income

- Lower volatility

- High-quality yield

Goal: Replace employment income without selling assets.

15. Tax Treatment of Dividends in Tier-1 Countries

Tax rules differ by country, but understanding them is essential to maximize after-tax income.

🇺🇸 United States

- Qualified dividends taxed at 0%, 15%, or 20% depending on income.

- Non-qualified dividends taxed as ordinary income.

- Tax-advantaged accounts (Roth IRA, 401(k), IRA) provide tax-free or tax-deferred growth.

🇬🇧 United Kingdom

- Annual dividend allowance is tax-free.

- Dividends taxed at varying rates based on income.

- ISAs and SIPPs provide tax-free dividend income.

🇨🇦 Canada

- Eligible dividends receive the Dividend Tax Credit, reducing tax liability.

- TFSA and RRSP shelter dividends from taxes.

🇦🇺 Australia

- Franking credits reduce or eliminate dividend taxes.

- Superannuation accounts offer favorable tax treatment.

Optimizing taxes increases net income, not just gross yield.

16. Common Dividend Investing Strategy Mistakes

Even a well-planned dividend investing strategy can fail if investors make common mistakes like chasing unsustainable yields.

❌ Chasing Yield

High yield often signals:

- Financial distress

- Unsustainable payouts

- Potential dividend cuts

Focus on sustainability, not headline yield.

❌ Ignoring Dividend Growth

A stock yielding 3% growing at 8% will outperform a static 6% yield over time.

❌ Overconcentration

Owning too many stocks in one sector increases risk.

Diversification protects income stability.

❌ Not Reinvesting Early

Skipping reinvestment in early years dramatically reduces compounding.

❌ Selling During Market Panic

Dividend investing is designed for long-term ownership, not short-term trading.

17. Dividend Investing vs. Growth Investing

| Feature | Dividend Investing | Growth Investing |

|---|---|---|

| Income | Immediate | None initially |

| Volatility | Lower | Higher |

| Compounding | Through reinvestment | Through price appreciation |

| Psychological comfort | High | Lower |

| Best for | Income seekers, retirees | Young investors, risk-takers |

The most resilient portfolios combine both strategies.

18. Real-World Examples of Successful Dividend Strategies

Example 1: The Long-Term Investor

- Invests $500/month

- Average yield: 3.5%

- Dividend growth: 7%

- Time horizon: 30 years

Results:

- Portfolio value ≈ $600,000+

- Annual income ≈ $30,000+

Example 2: The Early Retiree

- Invests aggressively for 15 years

- Builds $1 million dividend portfolio

- Average yield: 4%

Results:

- Annual income: $40,000

- Can retire without selling assets

19. How to Analyze a Dividend Stock Step-by-Step

Step 1: Check Dividend History

Look for:

- Consistency

- Growth

- No cuts during recessions

Step 2: Analyze Financials

Key metrics:

- Earnings growth

- Free cash flow

- Debt-to-equity ratio

Investors should also review dividend sustainability analysis from Morningstar, which provides detailed financial research, payout ratios, and long-term dividend safety ratings.

Step 3: Evaluate Payout Ratio

Prefer:

- 40–60% for most companies

- Up to 80% for REITs

Step 4: Assess Competitive Advantage

Look for:

- Strong brand

- Market leadership

- Switching costs

- Network effects

Step 5: Valuation

Do not overpay — even for great companies.

20. Advanced Dividend Strategies

Experienced investors often refine their dividend investing strategy using advanced income and diversification techniques.

🔹 Dividend Growth Ladder

Invest across companies with different growth rates and payout schedules to balance income and growth.

🔹 Sector Rotation

Shift exposure toward sectors with stronger dividend growth cycles.

🔹 Income Bucketing

Divide portfolio into:

- Stability bucket

- Growth bucket

- High-income bucket

🔹 Covered Call Writing

Generate additional income by selling call options on dividend stocks (advanced investors only).

21. Inflation and Dividend Income

Inflation reduces purchasing power, but dividend growth protects it. A strong dividend investing strategy focuses on companies that consistently grow dividends faster than inflation.

Inflation reduces purchasing power over time. Reliable data such as U.S. inflation data from the Bureau of Labor Statistics shows how rising prices impact long-term savings and investment income.

Example:

- Inflation: 3%

- Dividend growth: 6%

- Real income growth: 3%

This is why dividend growth matters more than raw yield.

22. Monthly Dividend Investing

Some investors prefer monthly income to align with budgeting needs.

Monthly payers include:

- Certain REITs

- Business Development Companies (BDCs)

- Monthly dividend ETFs

Benefits:

- Predictable cash flow

- Easier budgeting

- Psychological comfort

23. ETFs vs. Individual Dividend Stocks

Investors who want broad diversification can explore dividend ETFs listed on NASDAQ’s ETF database, which provides detailed fund performance, yield data, and expense ratios.

Dividend ETFs

Pros:

- Instant diversification

- Lower risk

- Low effort

Cons:

- Lower yield potential

- Less customization

Individual Stocks

Pros:

- Higher income potential

- Custom portfolio design

- Greater control

Cons:

- Requires research

- Higher risk if mismanaged

Most investors benefit from a hybrid approach.

Many investors combine both approaches when designing a diversified dividend investing strategy.

24. Building a Sleep-Well-at-Night (SWAN) Dividend Portfolio

A SWAN portfolio is designed to:

- Survive market crashes

- Deliver consistent income

- Reduce emotional stress

Key characteristics:

- High-quality companies

- Conservative payout ratios

- Long dividend histories

- Sector diversification

This portfolio lets you focus on living your life, not watching stock prices. A SWAN portfolio represents the most conservative version of a dividend investing strategy, prioritizing reliability and income stability.

25. Final Thoughts: Designing a Powerful Dividend Investing Strategy

A disciplined dividend investing strategy can transform your portfolio into a lifelong passive income engine. Dividend investing is not about beating the market — it’s about building freedom.

Freedom from:

- Financial stress

- Job dependency

- Market timing anxiety

Freedom to:

- Travel

- Spend time with family

- Retire early

- Pursue passion projects

By consistently investing in high-quality dividend-paying companies, reinvesting income, and allowing time to work its magic, you transform money into a machine that pays you for life.

This is how you truly earn money while you sleep.