Introduction: Why Most People Fail at Saving (And Why You Won’t)

Saving $10,000 a year without sacrificing your lifestyle may sound impossible — but with the right system, it becomes predictable and achievable.

In surveys across Tier-1 countries, the majority of adults:

- Live paycheck to paycheck,

- Have less than three months of emergency savings,

- Feel constant financial stress,

- Believe saving requires extreme sacrifice.

This belief is not only wrong — it is dangerous, because it stops people from even trying.

Let’s be honest.

Most financial advice feels like this:

“Cancel Netflix.”

“Stop eating out.”

“Never buy coffee.”

“Cut everything fun.”

That advice works on paper, but fails in real life, because humans are emotional, habitual, and comfort-seeking creatures. We don’t live on spreadsheets — we live in routines, relationships, and environments.

The moment saving feels like punishment, motivation collapses.

But here’s the truth:

You can save $10,000 a year without downgrading your lifestyle — if you change your system instead of your happiness.

This guide is designed for people living in Tier-1 economies, where:

- The cost of living is high,

- Convenience is built into daily life,

- Subscriptions are invisible but constant,

- Lifestyle inflation is normalized,

- And financial pressure is continuous.

Instead of teaching you how to “spend less,” this guide teaches you how to:

- Spend intentionally,

- Eliminate waste without eliminating joy,

- Optimize your financial flow,

- Automate your savings,

- Increase your income strategically, not exhaustingly.

This is not a budgeting guide.

👉 “If you’re new to budgeting, check out our guide on How to Create a Budget That Works.”

This is a financial system design guide.

Let’s build a $10,000-a-year savings system that works with your life, not against it.

Section 1: Why $10,000 a Year Is a Life-Changing Number

Before we talk about tactics, we need to talk about meaning.

Saving $10,000 a year isn’t just a number — it’s a psychological and financial threshold.

Let’s break it down:

- $833 per month

- $192 per week

- $27 per day

At first glance, that might feel overwhelming. But when you zoom out, most people unknowingly waste far more than $27 per day on:

- Convenience purchases,

- Overpriced subscriptions,

- Lifestyle creep,

- Unoptimized bills,

- Impulse spending.

In other words, this money is not missing — it’s leaking.

Why $10,000 Matters

Saving $10,000 a year changes your life in three major ways:

Scenario 1: Emergency Fund Security

An emergency fund is money set aside for unexpected expenses such as:

- Medical bills,

- Car repairs,

- Job loss,

- Home repairs,

- Family emergencies.

Financial experts recommend having 3–6 months of living expenses saved.

For example:

If your monthly expenses are $3,000:

- 3 months = $9,000,

- 6 months = $18,000.

Saving $10,000 a year means:

- You can fully fund your emergency buffer within 12–18 months,

- You no longer panic when life throws surprises,

- You stop relying on high-interest debt during emergencies.

This alone can eliminate financial anxiety.

👉 “Learn: How to Build an Emergency Fund Fast”

Scenario 2: Debt Freedom

Debt is one of the biggest barriers to wealth.

Let’s say you have:

- $8,000 in credit card debt at 22% interest,

- $12,000 in personal loans at 12% interest,

- $15,000 in auto loans at 7% interest.

Every year, you’re losing thousands in interest — money that produces no value.

Applying $10,000 annually toward debt means:

- Faster payoff,

- Less interest,

- More monthly cash flow,

- Higher credit score,

- Lower stress.

For example:

Paying off a $10,000 credit card balance at 22% saves you over $2,000 in interest over time.

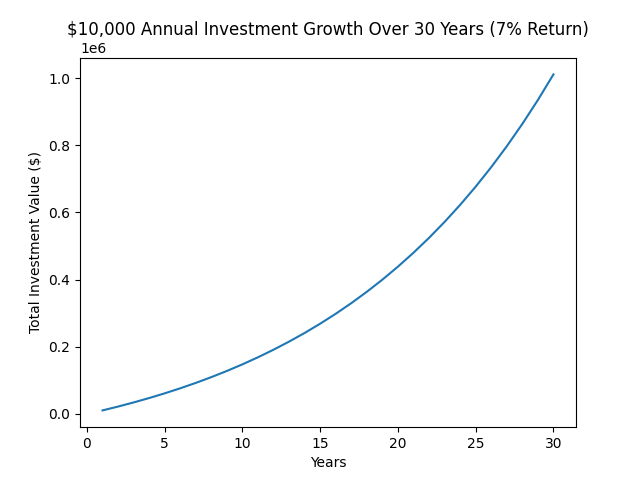

Scenario 3: Wealth Building Through Investing

Let’s assume you invest $10,000 per year at a conservative 7% average annual return.

Here’s what happens:

- After 8 years → ~$100,000

- After 15 years → ~$230,000

- After 25 years → ~$470,000

- After 30 years → ~$1,000,000+

That’s not magic — that’s compound interest, where your money earns money, and that money earns more money.

This is not about saving money.

This is about buying your future freedom.

Section 2: The Lifestyle-Preserving Savings Framework

Most people think saving money is about cutting spending.

In reality, saving money is about optimizing flow.

Instead of:

“Stop spending.”

We use:

“Spend intentionally and optimize silently.”

This framework has four pillars:

- Audit & Eliminate Invisible Money Leaks

- Replace High-Cost Habits with Equal-Value Alternatives

- Automate Savings Before You Can Spend

- Increase Income Without Increasing Burnout

Each pillar addresses a different part of your financial system:

- Pillar 1 removes waste,

- Pillar 2 preserves joy,

- Pillar 3 builds discipline through automation,

- Pillar 4 expands capacity through income growth.

Together, they create a system that saves $10,000+ per year without sacrificing lifestyle.

Let’s examine each pillar in depth.

Section 3: Pillar 1 — Audit & Eliminate Invisible Money Leaks

What Is a Money Leak?

A money leak is any recurring expense or spending habit that:

- Provides little to no real value,

- Goes unnoticed or unquestioned,

- Slowly drains your financial resources over time.

Unlike big purchases (like rent or a car), money leaks are:

- Small,

- Frequent,

- Invisible,

- Emotionally insignificant,

- But financially devastating over time.

Think of money leaks like a dripping faucet — one drop doesn’t matter, but over a year, it floods the room.

Step 1: Perform a Subscription & Recurring Expense Audit

In Tier-1 countries, the average adult spends $1,200–$2,500 per year on forgotten or underused subscriptions.

Examples include:

- Streaming services (Netflix, Hulu, Prime, Disney+, etc.)

- Cloud storage (Google Drive, iCloud, Dropbox)

- Gym memberships

- App subscriptions

- News or magazine sites

- Software tools

- Meal kits

- Delivery memberships

- Meditation apps

- Fitness apps

- Language apps

Many people subscribe during:

- Free trials,

- Promotions,

- Emotional moments (“I’ll start tomorrow”),

- Convenience decisions,

- Impulse actions.

And then… they forget.

Action Step:

Pull your bank and credit card statements for the last 3 months and list every recurring charge.

Create three columns:

- Service name

- Monthly cost

- Actual usage

Then ask:

- Do I use this weekly?

- Does this genuinely improve my life?

- Would I miss it in 30 days?

Cancel everything that:

- You rarely use,

- You forgot about,

- You don’t care about,

- You only keep out of habit.

But — and this is important — do not cancel things you truly value.

This is not about deprivation.

This is about alignment.

Example:

Sarah pays:

- $15/month for Netflix (uses daily),

- $12/month for Hulu (rarely uses),

- $10/month for a fitness app (never uses),

- $9/month for cloud storage she no longer needs.

She cancels Hulu, the fitness app, and cloud storage.

Monthly savings: $31

Annual savings: $372

And she didn’t lose anything she cared about.

Typical savings: $30–$150/month

Annual impact: $360–$1,800

Step 2: Optimize Utilities Without Downgrading Lifestyle

Utilities are essential — but that doesn’t mean they’re optimized.

Common utilities include:

- Internet

- Mobile plans

- Electricity

- Gas

- Water

- Trash services

- Insurance (auto, renters/home, health)

Most people:

- Stay with the same provider for years,

- Accept price increases passively,

- Never renegotiate,

- Assume switching is difficult,

- Fear losing service quality.

In reality, utility companies:

- Offer better deals to new customers,

- Provide loyalty discounts if asked,

- Have retention departments trained to offer savings,

- Compete aggressively for customers.

Action Plan:

Once per year:

- Call each provider.

- Ask for:

- Loyalty discounts,

- Promotional rates,

- Competitor matching.

- Compare rates online.

- Switch providers if necessary.

This does not reduce your quality — it reduces overpricing.

Example:

John pays:

- $95/month for internet,

- $110/month for mobile plans,

- $220/month for electricity.

He calls his providers and negotiates:

- Internet reduced to $70,

- Mobile plan reduced to $85,

- Electricity supplier switched to a lower rate.

Monthly savings: $170

Annual savings: $2,040

No lifestyle change — just smarter contracts.

Typical savings: $50–$200/month

Annual impact: $600–$2,400

Step 3: Optimize Insurance Without Losing Coverage

Insurance is necessary — but rarely optimized.

Most people:

- Overpay for coverage,

- Keep the same policies for years,

- Never shop around,

- Fear switching providers,

- Don’t understand their deductibles,

- Are unaware of bundling discounts.

Common insurance types:

- Auto

- Homeowners or renters

- Health

- Life

- Disability

- Travel

Action Plan:

Once per year:

- Get quotes from at least 3 providers,

- Compare coverage apples-to-apples,

- Increase deductibles slightly if you have an emergency fund,

- Bundle auto + home/renters where beneficial,

- Ask about loyalty, safety, and multi-policy discounts.

Example:

Maria pays:

- $210/month for auto insurance,

- $45/month for renters insurance.

She shops around and finds:

- Same coverage for $155/month auto,

- $28/month renters,

- With bundling discounts.

Monthly savings: $72

Annual savings: $864

No reduction in protection — only in price.

Typical savings: $40–$150/month

Annual impact: $480–$1,800

Total Pillar 1 Savings Potential:

$1,500 – $5,000 per year, with zero lifestyle downgrade.

This alone could get you halfway to your $10,000 goal.

Section 4: Pillar 2 — Replace, Don’t Remove

Most financial advice focuses on removal:

- Remove dining out,

- Remove entertainment,

- Remove shopping,

- Remove comfort.

But humans are not designed for constant removal.

Instead, we use replacement:

- Replace high-cost habits with equal-value alternatives,

- Replace low-value spending with high-value experiences,

- Replace impulse with intention.

This preserves your lifestyle while optimizing your finances.

Example 1: Dining & Food

Instead of:

“Stop eating out.”

Use:

“Eat out intentionally.”

Food is emotional, social, cultural, and enjoyable. Cutting it completely is unrealistic and unnecessary.

Optimization Strategies:

- Shift Timing

- Eat lunch instead of dinner at premium restaurants.

- Lunch menus are often 30–50% cheaper.

- Use Loyalty Programs

- Many restaurants offer:

- Points,

- Free meals,

- Birthday rewards,

- Referral bonuses.

- Many restaurants offer:

- Replace Low-Value Takeout

- Replace 2 takeout meals per week with 2 high-quality home meals.

- This doesn’t mean boring meals — it means intentional cooking.

- Use Grocery Delivery

- Prevent impulse purchases,

- Stick to your list,

- Save time and mental energy.

- Meal Prep Strategically

- Prep only the meals you dislike cooking.

- Keep variety — don’t eat the same meal all week.

Example:

Alex spends $700/month on dining and takeout.

He:

- Keeps his weekend restaurant dinners,

- Replaces 2 weekday takeouts with home meals,

- Uses lunch menus for premium restaurants,

- Uses grocery delivery.

New food spending: $450/month

Monthly savings: $250

Annual savings: $3,000

No lifestyle downgrade — just optimized habits.

Savings: $100–$300/month

Annual impact: $1,200–$3,600

Example 2: Entertainment & Experiences

Instead of:

“Stop going out.”

Use:

“Get more value per dollar.”

Entertainment includes:

- Movies,

- Concerts,

- Sports events,

- Theaters,

- Museums,

- Travel,

- Hobbies,

- Experiences.

You don’t need less entertainment — you need better value.

Optimization Strategies:

- Use Memberships & Passes

- Museums, zoos, theaters, gyms, and parks often offer annual passes that:

- Cost less than 3–4 visits,

- Provide unlimited access,

- Offer guest privileges.

- Museums, zoos, theaters, gyms, and parks often offer annual passes that:

- Attend Matinees

- Matinee shows and movies are often 30–60% cheaper than evening performances.

- Leverage Community Events

- Many cities offer:

- Free concerts,

- Free festivals,

- Outdoor movies,

- Cultural events,

- Public lectures.

- Many cities offer:

- Use Reward Points

- Travel rewards cards,

- Cashback programs,

- Credit card points,

- Loyalty programs.

- Plan Experiences in Advance

- Avoid last-minute pricing premiums.

Example:

Rachel spends $300/month on entertainment.

She:

- Switches to annual museum passes,

- Uses matinee tickets,

- Attends free city events,

- Uses reward points for concerts.

New spending: $180/month

Monthly savings: $120

Annual savings: $1,440

No less fun — just smarter fun.

Savings: $50–$150/month

Annual impact: $600–$1,800

Example 3: Shopping & Consumer Goods

Instead of:

“Stop buying things.”

Use:

“Buy smarter.”

Shopping includes:

- Clothing,

- Electronics,

- Home goods,

- Gadgets,

- Beauty products,

- Accessories.

Most waste comes from:

- Impulse purchases,

- Trend chasing,

- Low-quality items,

- Overbuying,

- Emotional shopping.

Optimization Strategies:

- Use Price Tracking Tools

- Track prices over time,

- Buy at historical lows,

- Avoid paying full price unnecessarily.

- Buy Off-Season

- Winter clothes in spring,

- Summer clothes in fall,

- Holiday decor after holidays.

- Choose Quality Over Quantity

- One high-quality item that lasts 5 years > five cheap items that break in 6 months.

- Use Cashback & Reward Cards

- Earn 1–5% back on purchases,

- Stack with discounts and coupons.

- Implement the 48-Hour Rule

- Wait 48 hours before buying non-essential items.

- Most impulse urges disappear within this time.

Example:

David spends $400/month on shopping.

He:

- Uses price tracking,

- Waits 48 hours before purchases,

- Buys higher-quality items,

- Uses cashback cards.

New spending: $250/month

Monthly savings: $150

Annual savings: $1,800

No reduction in enjoyment — just smarter buying.

Savings: $75–$200/month

Annual impact: $900–$2,400

Total Pillar 2 Savings Potential:

$2,700 – $7,800 per year, with no lifestyle downgrade — only smarter spending.

Section 5: Pillar 3 — Automate Your Savings Before You Can Spend

The biggest mistake people make is trying to save what’s left over at the end of the month.

The truth is:

There is never anything left over.

Spending expands to fill available money — a concept known as Parkinson’s Law.

So instead of:

“Save what’s left,”

We use:

“Save first, spend what remains.”

This is called Paying Yourself First.

Step 1: Pay Yourself First

Set up automatic transfers from your checking account to:

- A high-yield savings account,

- An investment account,

- An emergency fund.

Do this on payday — not after bills, not after spending, not when you “remember.”

Start with:

- $100–$200 per paycheck,

- Or 5–10% of your income,

- Increase gradually as your income grows.

You won’t miss what you never see.

Example:

Emma earns $4,000/month.

She sets:

- $300/month to savings,

- $200/month to investments.

Total: $500/month

Annual: $6,000 saved automatically.

She doesn’t “feel” poorer — her system simply adjusts.

Step 2: Use Multiple Savings Buckets

Instead of one giant savings account, create separate “buckets”:

- Emergency Fund

- Covers unexpected expenses.

- Goal: 3–6 months of expenses.

- Travel Fund

- For vacations and trips.

- Prevents debt-funded travel.

- Big Purchase Fund

- For cars, home upgrades, electronics, weddings, etc.

- Investing Fund

- For wealth building and retirement.

This creates:

- Psychological clarity,

- Motivation,

- Purpose-driven saving,

- Reduced guilt when spending from the right bucket.

Example:

Instead of thinking:

“I’m spending my savings,”

You think:

“I’m spending my travel fund — which is exactly what it’s for.”

Step 3: Use Round-Up & Micro-Saving Tools

These tools:

- Round your purchases to the nearest dollar,

- Transfer the difference to savings or investments,

- Sweep leftover balances at the end of the month.

For example:

- You buy coffee for $3.60,

- The app rounds up to $4.00,

- The extra $0.40 goes to savings.

Over time, these micro-savings add up without effort.

Typical savings: $500–$1,500 per year.

Total Pillar 3 Savings Potential:

$1,200 – $3,000 per year, entirely automated.

Section 6: Pillar 4 — Increase Income Without Increasing Burnout

Saving $10,000 per year doesn’t always require extreme frugality.

Sometimes, the fastest way to save more is to earn more — but in a way that doesn’t destroy your health, relationships, or mental well-being.

We avoid:

- 80-hour workweeks,

- Hustle culture,

- Burnout,

- Chronic stress,

- Sacrificing life for money.

Instead, we focus on:

- Leverage,

- Skills,

- Systems,

- Optimization,

- Scalability.

Strategy 1: Salary Optimization

Most people leave thousands of dollars on the table because they:

- Never negotiate,

- Stay in underpaid roles,

- Underestimate their market value,

- Fear rejection,

- Don’t research salaries.

Action Steps:

- Benchmark Your Role

- Use salary websites,

- Talk to recruiters,

- Network within your industry.

- Prepare a Data-Driven Case

- Document achievements,

- Quantify results,

- Show impact.

- Ask for Raises Regularly

- Annually or after major accomplishments.

- Apply Externally Every 2–3 Years

- Job switching often results in 10–30% pay increases.

Example:

Michael earns $60,000/year.

He researches his role and discovers the market range is $70,000–$85,000.

He applies externally and receives an offer for $75,000.

Increase: $15,000/year.

Even if he saves only 50% of that increase:

Savings: $7,500/year — without changing spending habits.

Typical increase: $3,000–$10,000 per year (often more).

Strategy 2: Skill-Based Side Income

Side income doesn’t have to mean:

- Driving all night,

- Working weekends,

- Sacrificing rest,

- Constant hustling.

Instead, we focus on skill leverage.

Examples:

- Freelancing (writing, design, coding, marketing),

- Consulting,

- Coaching,

- Tutoring,

- Teaching online,

- Content creation,

- Social media management,

- Virtual assistance,

- Copywriting,

- Data analysis,

- Web development.

The goal is:

- High value per hour,

- Low time investment,

- Flexible schedule,

- Skill-based compensation.

Even $200/week = $10,400/year.

Example:

Lisa works full-time in marketing.

She offers freelance social media management to two small businesses for $500/month each.

Side income: $1,000/month

Annual: $12,000.

Even saving half of this:

Savings: $6,000/year.

Strategy 3: Passive & Semi-Passive Income

Passive income means earning money with minimal ongoing effort after setup.

Examples:

- Dividend investing,

- Rental income,

- Digital products (ebooks, templates, courses),

- Affiliate marketing,

- Blogging,

- YouTube,

- Podcast monetization,

- Stock photography,

- Licensing.

While passive income often starts slow, it:

- Scales over time,

- Reduces dependency on labor,

- Creates financial resilience.

Example:

James creates a $29 online course and sells it to 10 people per month.

Monthly income: $290

Annual: $3,480.

Combined with other streams, this compounds into real wealth.

Total Pillar 4 Income Impact:

$3,000 – $15,000+ per year, depending on effort, skills, and strategy.

Section 7: The $10,000 System — Putting It All Together

Let’s build a realistic, achievable system.

Monthly Optimization Breakdown

| Category | Monthly Savings | Annual Impact |

|---|---|---|

| Subscriptions & Bills | $120 | $1,440 |

| Food & Dining | $200 | $2,400 |

| Shopping & Entertainment | $150 | $1,800 |

| Insurance Optimization | $100 | $1,200 |

| Automated Savings | $150 | $1,800 |

| Side Income | $200 | $2,400 |

| Total | $920/month | $11,040/year |

No suffering.

No deprivation.

Just optimization.

This system:

- Preserves lifestyle,

- Removes waste,

- Builds automation,

- Increases income,

- Compounds over time.

Section 8: Psychology — The Secret to Saving Without Stress

Most financial failure isn’t due to math — it’s due to emotion.

Understanding your psychology is just as important as understanding your numbers.

1. Avoid the All-or-Nothing Trap

The all-or-nothing mindset says:

“If I can’t do this perfectly, I won’t do it at all.”

This leads to:

- Overambitious goals,

- Early burnout,

- Guilt,

- Quitting.

Instead, aim for:

- Progress, not perfection,

- Systems, not willpower,

- Consistency, not intensity.

Missing one goal doesn’t break the system.

Quitting does.

2. Make Saving Visible and Rewarding

Human brains are motivated by:

- Progress,

- Rewards,

- Visual feedback.

Track your savings:

- Use charts,

- Use apps,

- Use spreadsheets,

- Use visual trackers.

Celebrate milestones:

- First $1,000 saved,

- First month of automation,

- First debt paid off,

- First investment made.

Reward yourself — strategically:

- Small treats,

- Experiences,

- Not financial sabotage.

3. Detach Identity from Spending

Many people unconsciously equate:

- Spending with success,

- Luxury with worth,

- Appearance with achievement.

This leads to:

- Lifestyle inflation,

- Financial stress,

- Endless comparison,

- Never feeling “enough.”

True wealth is not:

- Expensive things,

- Flashy purchases,

- Social validation.

True wealth is:

- Optionality (you can choose),

- Security (you are safe),

- Peace (you are calm).

Section 9: Common Mistakes That Kill Savings Goals

Avoid these traps:

1. Budgeting Without Automation

Relying on willpower alone leads to failure.

Without automation:

- You forget,

- You procrastinate,

- You overspend,

- You abandon goals.

Automation turns discipline into default behavior.

2. Cutting Joy Instead of Waste

Cutting joy leads to:

- Resentment,

- Burnout,

- Rebound spending,

- Quitting.

Cutting waste leads to:

- Effortless savings,

- Higher satisfaction,

- Sustainable progress.

3. Ignoring Income Growth

You can only cut so much.

You can earn infinitely more.

Ignoring income growth:

- Limits progress,

- Increases stress,

- Slows wealth building.

4. Not Reviewing Finances Quarterly

Life changes.

Expenses change.

Income changes.

Goals change.

Without regular review:

- You drift,

- Leaks return,

- Goals fade.

Quarterly reviews keep your system aligned.

5. Letting Lifestyle Creep Erase Gains

Lifestyle creep is when spending rises automatically with income.

You get a raise → you upgrade your lifestyle → your savings stay the same.

Instead:

- Save first,

- Upgrade intentionally,

- Keep progress compounding.

6. Saving Without Investing

Saving protects money.

Investing grows money.

Without investing:

- Inflation erodes purchasing power,

- Long-term wealth stagnates.

Savings alone won’t make you wealthy — systems will.

Section 10: Advanced Tier-1 Strategies for High Earners

If you live in a Tier-1 economy and earn above the median, your opportunity is even greater — but so is your risk of waste.

1. Tax Optimization

Taxes are one of your largest expenses — and one of the most optimizable.

Strategies include:

- Using tax-advantaged accounts (401(k), IRA, RRSP, TFSA, ISA, superannuation),

- Maximizing employer matches,

- Using health savings accounts (HSA),

- Using flexible spending accounts (FSA),

- Harvesting capital losses,

- Optimizing filing status,

- Claiming eligible deductions and credits.

Potential savings: $2,000–$10,000/year.

2. Credit Optimization

Better credit leads to:

- Lower interest rates,

- Cheaper insurance premiums,

- Better loan terms,

- More financial flexibility.

Strategies include:

- Paying bills on time,

- Reducing credit utilization,

- Refinancing high-interest loans,

- Using 0% APR offers strategically,

- Optimizing reward structures.

3. Lifestyle Design

Lifestyle design means intentionally designing your life to:

- Minimize stress,

- Maximize satisfaction,

- Optimize finances,

- Align with values.

Design a lifestyle where:

- Fixed costs are low,

- Variable spending is intentional,

- Income grows automatically,

- Savings happen invisibly,

- Happiness is not dependent on spending.

Section 11: The One-Year $10,000 Action Plan

Let’s translate theory into action.

Month 1: Financial Audit

- Track every expense,

- Cancel unused subscriptions,

- Identify money leaks,

- Create a baseline.

Month 2: Automation Setup

- Set up savings buckets,

- Automate transfers,

- Use round-up tools,

- Start paying yourself first.

Month 3: Food & Shopping Optimization

- Implement meal strategies,

- Apply shopping rules,

- Set spending boundaries,

- Optimize rewards.

Month 4: Insurance & Utilities Review

- Shop insurance rates,

- Adjust deductibles,

- Bundle policies,

- Negotiate utilities.

Month 5: Income Optimization

- Benchmark salary,

- Prepare raise requests,

- Apply externally if needed,

- Launch side income.

Months 6–12: Optimization & Scaling

- Increase savings rate,

- Invest surplus,

- Eliminate remaining inefficiencies,

- Review finances quarterly,

- Scale income streams.

Section 12: What Saving $10,000 a Year Actually Gives You

Let’s move beyond numbers.

Saving $10,000 a year gives you:

- Freedom from paycheck-to-paycheck stress

- Freedom to walk away from toxic jobs

- Freedom to invest in yourself

- Freedom to travel without guilt

- Freedom to handle emergencies without panic

- Freedom to help family

- Freedom to build generational wealth

It’s not about money.

It’s about control, choice, and peace.

Trusted Financial Resources

- Financial data from the Federal Reserve shows that a large percentage of households lack sufficient emergency savings.

- Tax strategies recommended by the Internal Revenue Service can help reduce liabilities and improve long-term financial planning.

- Long-term investing principles promoted by Vanguard Group emphasize low-cost index investing and disciplined wealth building.

- Budgeting and savings frameworks highlighted by the Organisation for Economic Co-operation and Development demonstrate the importance of consistent saving behavior.

Conclusion: You Don’t Need a New Lifestyle — You Need a New System

You don’t need to:

- Eat worse,

- Live smaller,

- Cancel your happiness,

- Or become financially obsessed.

You need a system that:

- Removes waste,

- Automates savings,

- Optimizes income,

- Preserves joy,

- Compounds over time.

Saving $10,000 a year without sacrificing your lifestyle isn’t just possible — it’s predictable when you design your financial system intentionally.

Start today.

Optimize silently.

And let your future self thank you.