1. Introduction: Why Market Crashes Create Millionaires

Market crashes are among the most emotionally painful experiences an investor can face.

How to invest during a market crash is one of the most important financial skills you can learn if you want to build long-term wealth in Tier-1 economies like the United States, United Kingdom, Canada, Australia, and Europe.

Market crashes are emotionally painful. Portfolios drop. News headlines turn negative. Social media spreads fear. Yet history shows that investors who understand how to invest during a market crash — instead of panicking — often achieve the strongest long-term returns.

In this complete 2026 guide, you will learn how to invest during a market crash safely, strategically, and confidently.

But here is a powerful and uncomfortable truth:

Every major market crash in history has created more long-term wealth than any bull market.

This is not motivational hype — it is a mathematical and historical fact.

What Does This Mean?

A bull market is a period when markets are rising, optimism is high, and asset prices are expensive. During these periods, most people feel confident, invest aggressively, and expect easy gains. However, future returns are often lower because assets are already priced high.

A market crash or bear market is the opposite — prices fall sharply, fear dominates, and pessimism is widespread. Yet this is when assets become undervalued, meaning their prices fall below their long-term economic value. When you buy at these lower prices, your potential long-term returns increase dramatically.

Over time, this effect compounds powerfully (see our complete guide to compound interest to understand how exponential growth works).

A Simple Example

Imagine two investors:

- Investor A invests $10,000 when markets are at all-time highs.

- Investor B invests $10,000 during a crash when markets are down 40%.

If the market eventually doubles from its crash low:

- Investor A’s $10,000 might grow to $15,000 or $18,000 over time.

- Investor B’s $10,000 could grow to $20,000 or more.

Same amount invested. Same market. Very different results — purely because of timing relative to fear.

The Wisdom of Warren Buffett

Warren Buffett, one of the most successful investors in history, summarized this perfectly:

“Be fearful when others are greedy, and greedy when others are fearful.”

Most people do the opposite. They feel confident when prices are high (greedy) and terrified when prices are low (fearful). This emotional cycle leads to:

- Buying high

- Selling low

- Repeating the pattern

This behavior destroys wealth.

Disciplined investors, however, do something very different. They:

- Continue investing during downturns

- Focus on quality assets

- Think long-term

- Ignore short-term noise

As a result, they often achieve life-changing financial outcomes.

What This Guide Will Teach You

This article will show you — in simple, clear, and detailed language — how to invest during a market crash without panic. You will learn:

- How to protect yourself financially before investing

- Why your brain works against you during crises

- How to use proven investment strategies like dollar-cost averaging

- How to identify strong investments when others are fearful

- How to stay emotionally calm and rational during extreme volatility

Whether you are a beginner investor or an experienced one, this guide will give you a step-by-step framework to:

✔ Protect your financial stability

✔ Avoid emotional mistakes

✔ Identify high-quality opportunities

✔ Build long-term wealth while others retreat

Let’s begin by understanding what a market crash actually is.

2. What Is a Market Crash? (In Plain English)

A market crash is a rapid and severe drop in stock market prices, usually defined as a decline of 20% or more in a major market index over a short period of time. Understanding what causes crashes is essential if you want to master how to invest during a market crash instead of reacting emotionally.

According to official inflation data from the U.S. Bureau of Labor Statistics inflation data, economic pressures such as rising prices and tightening monetary policy often contribute to downturns and market volatility.

What Is a Market Index?

A market index is a measurement that tracks the performance of a group of stocks, representing a specific market or segment of the economy. Examples include:

- S&P 500 (USA): Tracks 500 large U.S. companies

- FTSE 100 (UK): Tracks 100 major UK companies

- TSX Composite (Canada): Tracks the Canadian stock market

- ASX 200 (Australia): Tracks 200 major Australian companies

- STOXX Europe 600: Tracks large European companies

When these indexes fall sharply, it means the overall market is declining — not just one or two companies.

What Causes Market Crashes?

Market crashes do not happen randomly. They are usually triggered by a combination of economic, financial, political, and psychological factors, such as:

1. Economic Recessions

A recession is a period of declining economic activity, often marked by rising unemployment, lower consumer spending, and reduced corporate profits. When businesses earn less, their stock prices fall.

2. Financial Crises

This occurs when the financial system itself is under stress — for example, bank failures, credit freezes, or housing market collapses. The 2008 Global Financial Crisis is a prime example.

3. Geopolitical Events

Wars, pandemics, trade conflicts, or major political instability can create uncertainty and fear, leading investors to sell.

4. Sudden Shifts in Investor Confidence

Sometimes crashes happen simply because investors collectively lose confidence, even without a single clear event — this is often referred to as a panic or sentiment-driven crash.

Real-World Examples of Market Crashes

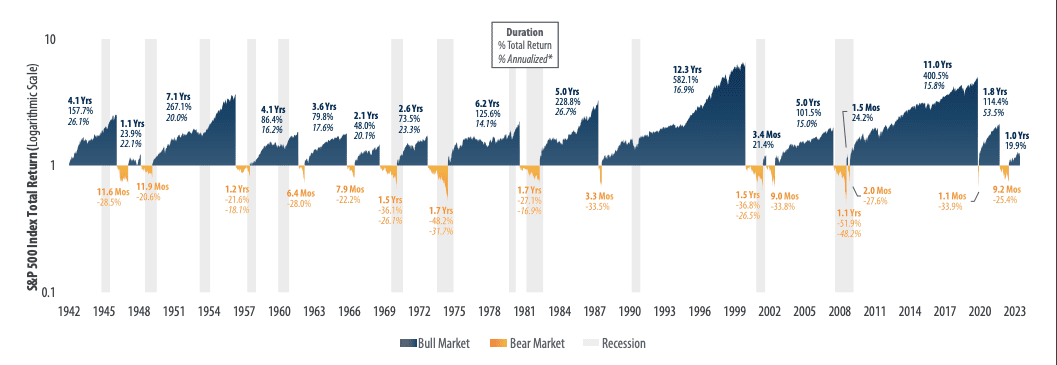

Let’s look at some of the most significant crashes in modern financial history:

📉 Dot-Com Crash (2000–2002)

Technology stocks were wildly overvalued based on hype rather than profits. When reality hit, the NASDAQ fell nearly 80%. Many companies disappeared, but survivors like Amazon eventually became giants.

📉 Global Financial Crisis (2008–2009)

Triggered by a housing bubble and risky financial products, major banks collapsed or were bailed out. Stock markets fell around 50%, but later recovered and reached new all-time highs.

UK investors can review monetary policy and economic data directly from the Bank of England.

Canadian readers can follow official economic updates via the Bank of Canada.

Australian investors can monitor interest rate decisions and economic conditions through the Reserve Bank of Australia.

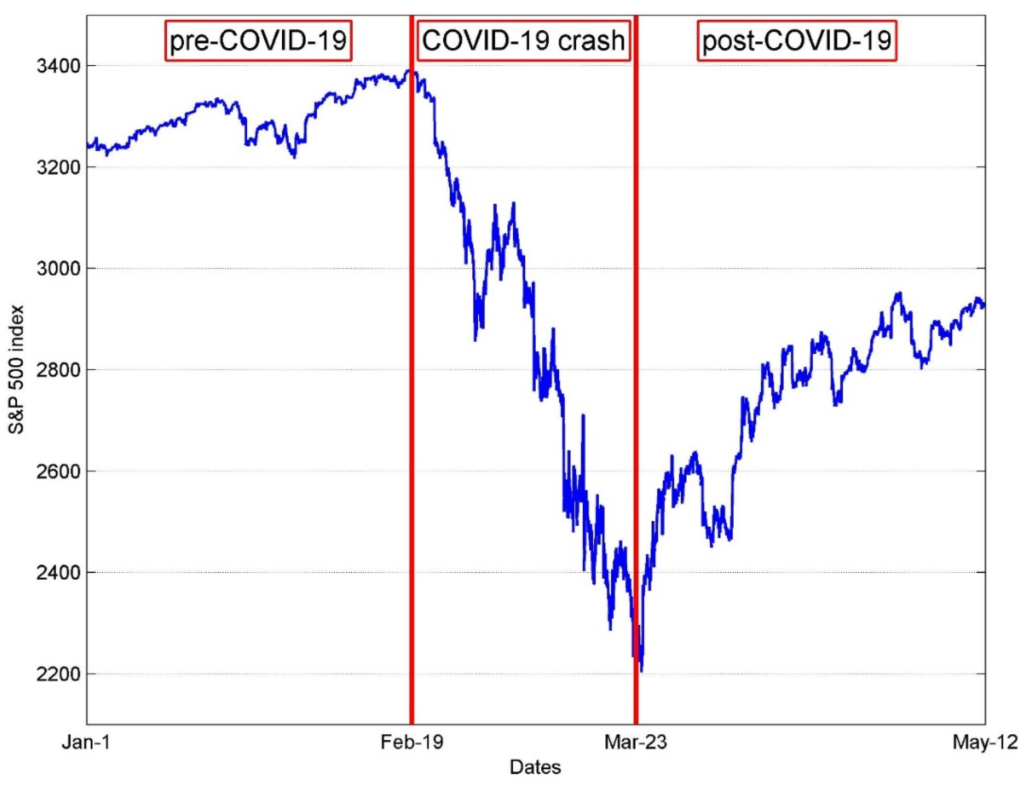

📉 COVID-19 Crash (2020)

Global markets fell over 30% in a matter of weeks due to pandemic fears. Within months, markets rebounded and entered one of the strongest bull markets in history.

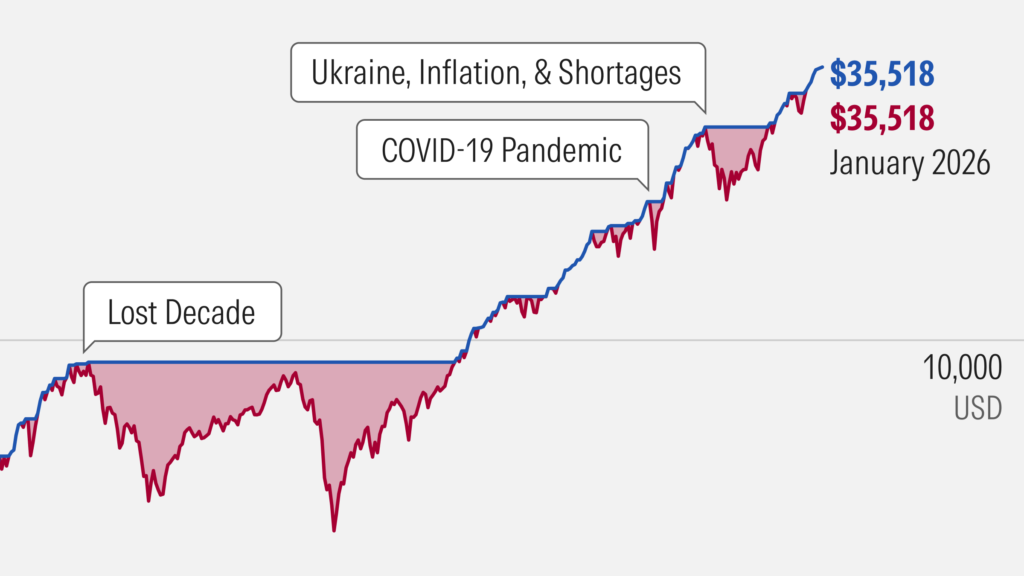

📉 Inflation-Driven Bear Market (2022)

High inflation and rising interest rates caused a broad market decline, particularly in technology and growth stocks.

What Happens After Crashes?

In every major crash:

- The economy eventually recovered

- Businesses adapted and grew

- Markets reached new all-time highs

This does not mean recovery is immediate or painless — but it is consistent.

Key takeaway:

A market crash is not the end of capitalism. It is a temporary repricing of assets — and often a massive long-term opportunity for disciplined investors.

3. Why People Panic (Behavioral Finance Explained)

Understanding why people panic during crashes is essential to learning how to stay calm and rational.

The field that studies how psychology affects financial decisions is called behavioral finance.

Why Humans Are Bad at Investing

Human brains evolved to survive physical danger — not to manage financial markets. Thousands of years ago, quick reactions to threats (like predators) were essential for survival. But in modern investing, those same instincts lead to poor decisions.

During market crashes, several psychological biases activate automatically.

Let’s break them down clearly.

🧠 Loss Aversion

Loss aversion means that people feel the pain of losing money much more strongly than the pleasure of gaining the same amount.

Example:

- Losing $1,000 feels about twice as painful as gaining $1,000 feels good.

This causes people to:

- Panic when their portfolio drops

- Sell just to “stop the pain”

- Lock in losses rather than waiting for recovery

Even if selling is logically harmful, emotionally it feels like relief — similar to stopping physical pain.

🧠 Recency Bias

Recency bias means we assume that what just happened will continue indefinitely.

Example:

- If the market has fallen for 6 months, people believe it will keep falling forever.

- If the market has risen for 6 years, people believe it will rise forever.

This bias causes:

- Fear during downturns

- Overconfidence during bull markets

In reality, markets are cyclical — they move in cycles, not straight lines.

🧠 Herd Mentality

Herd mentality means people follow what others are doing — especially in uncertain situations.

Example:

- If everyone around you is selling, you feel pressure to sell too.

- If everyone is excited and buying, you feel pressure to buy.

Humans are social creatures. When we see a crowd running, our brain assumes danger — even if we don’t know why.

In investing, this leads to:

- Selling at market bottoms

- Buying at market tops

🧠 Availability Bias

Availability bias means we judge how likely something is based on how easily examples come to mind.

During crashes:

- News is full of negative stories

- Social media amplifies fear

- Pessimistic opinions dominate

This makes disasters feel more likely and permanent than they actually are.

The Result of These Biases

Together, these psychological forces push investors to:

- Sell at the worst possible time

- Stop investing when prices are lowest

- Hoard cash indefinitely

- Miss market recoveries

Outcome:

They lock in losses and miss the most profitable periods in market history.

Understanding these biases doesn’t automatically remove them — but it gives you the awareness to override them consciously.

Learning how to invest during a market crash starts with understanding your own psychology.

4. The Biggest Mistakes Investors Make During Crashes

Now let’s clearly identify the most damaging mistakes investors make during market crashes — and why they hurt long-term wealth. When learning how to invest during a market crash, avoiding these mistakes is more important than finding the perfect stock.

❌ Mistake #1: Selling Everything in Fear

This is the most destructive mistake.

When investors panic-sell, they:

- Convert temporary losses into permanent losses

- Lose the opportunity to benefit from recovery

- Often struggle emotionally to reinvest later

Example:

An investor sells during a 40% market decline. The market then recovers and doubles over the next several years. The investor either stays out or re-enters later at higher prices, missing a large portion of the gains.

Selling during crashes is like abandoning a marathon halfway because you’re tired — even though the finish line is ahead.

❌ Mistake #2: Trying to “Time the Bottom”

Many investors believe:

“I’ll sell now and buy back when the market hits the bottom.”

This sounds logical — but in reality:

- No one knows where the bottom is

- By the time it feels “safe,” prices have often already risen

- Emotional fear prevents people from buying even at low prices

Example:

After the 2008 crash, many investors waited until markets “felt safe” — but markets had already risen significantly by the time they re-entered.

Timing the market requires being right twice — when to sell and when to buy back. Most people fail at both.

❌ Mistake #3: Stopping Contributions

Some investors stop investing during downturns because:

- They feel uncertain

- They fear further losses

- They want to “wait and see”

This is like refusing to buy groceries because they’re on sale — even though you’ll need them anyway.

By stopping contributions, investors:

- Miss buying assets at discounted prices

- Raise their long-term average cost

- Reduce the compounding effect of time

❌ Mistake #4: Switching to Cash Forever

Holding cash feels safe — but excess cash is expensive due to inflation.

Inflation reduces the purchasing power of money over time. For example:

- If inflation is 3% per year, $100 today is worth about $97 next year in real terms.

Holding large amounts of cash for too long:

- Erodes wealth

- Misses investment growth

- Creates a false sense of security

❌ Mistake #5: Chasing Risky Bets to Recover Losses

Some investors react to losses by:

- Taking extreme risks

- Investing in speculative stocks, cryptocurrencies, or leveraged products

- Hoping to “win back” lost money quickly

This behavior is emotionally driven and often leads to even larger losses.

It is similar to gambling — not investing.

Many of these behaviors are rooted in common investing myths (see our full Investing Myths guide to avoid costly errors).

The Good News

Avoiding these mistakes alone can dramatically improve your long-term returns — even without picking “perfect” investments.

5. Step 1: Protect Your Financial Foundation

Before investing aggressively during a market crash, you must ensure your financial foundation is strong.

This step is not optional — it is essential.

✅ Build or Maintain an Emergency Fund

If you don’t yet have one, start with our step-by-step Emergency Fund guide before investing aggressively. An emergency fund is a pool of money set aside for unexpected expenses, such as:

- Job loss

- Medical emergencies

- Car repairs

- Home repairs

It should be:

- Easily accessible

- Kept in cash or a high-yield savings account

- Not invested in volatile assets

Recommended size:

- At least 3–6 months of essential living expenses

- More (6–12 months) if your income is unstable or you are self-employed

Why this matters during a crash:

If you lose your job or face unexpected expenses during a market downturn, you won’t be forced to sell investments at a loss.

✅ Eliminate High-Interest Debt

High-interest debt — such as credit cards, payday loans, or personal loans — is financially toxic.

Example:

- A credit card charging 20% interest is effectively costing you 20% per year.

- Very few investments reliably earn 20% annually.

Paying off high-interest debt provides a guaranteed return equal to the interest rate — with zero risk.

✅ Secure Your Income

If your job or business income is unstable, your priority should be:

- Upskilling to increase employability

- Building secondary income streams

- Reducing fixed expenses

This improves your financial resilience — your ability to survive financial shocks without panic.

🛑 The Golden Rule

Only invest money during a crash that you will not need for at least 5–10 years.

If you might need the money sooner — for education, housing, or emergencies — it should not be invested in volatile assets like stocks. This financial stability is the foundation of any successful market crash investing strategy.

6. Step 2: Separate Signal from Noise

A critical part of how to invest during a market crash is ignoring emotional noise and focusing on financial fundamentals. During market crashes, information overload becomes dangerous.

News channels, social media, podcasts, and blogs constantly broadcast:

- Breaking news

- Expert opinions

- Predictions

- Speculation

Most of this is noise, not useful signal.

🔊 Noise (What to Ignore)

Noise includes:

- Daily stock price movements

- Sensational headlines (“Markets in Freefall!”)

- Short-term forecasts

- Emotional commentary

- Social media panic

These do not help you make better long-term investment decisions.

📡 Signal (What to Focus On)

Signal includes:

- Corporate earnings and profits

- Balance sheets and debt levels

- Cash flow

- Long-term economic trends

- Valuations (price relative to earnings, assets, or cash flow)

Instead of reacting emotionally, ask:

- Is the business still profitable?

- Does it have strong cash flow?

- Is its debt manageable?

- Does it have a competitive advantage?

- Will people still need its products or services in 10 years?

If the answers are mostly “yes,” then the price decline may represent an opportunity, not a danger.

A Simple Example

During the COVID-19 crash, many airline, travel, and hospitality stocks collapsed. Some companies were financially weak and failed. Others had strong balance sheets and survived — and later rebounded strongly.

Investors who separated signal from noise could identify which businesses were likely to survive and recover.

7. Step 3: Use Dollar-Cost Averaging Like a Professional

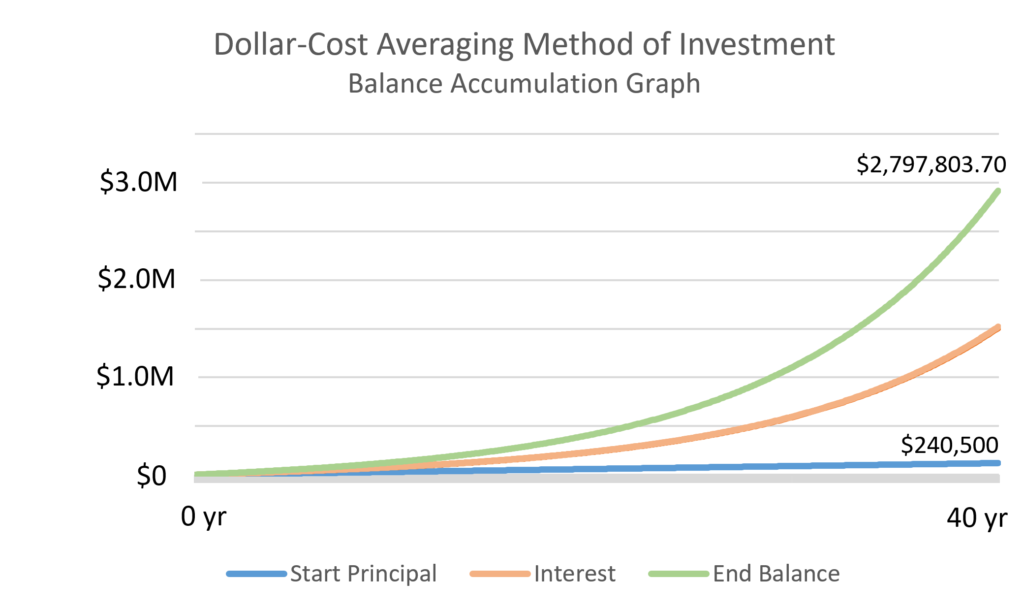

Dollar-Cost Averaging (DCA) is one of the most powerful and psychologically effective investment strategies — especially during market crashes. Dollar-cost averaging is one of the safest ways to invest during a downturn without trying to predict the bottom.

Long-term investing research from Vanguard consistently shows that disciplined, long-term investing outperforms market timing.

What Is Dollar-Cost Averaging?

Dollar-Cost Averaging means investing a fixed amount of money at regular intervals — regardless of market conditions.

Example:

You invest $500 every month into a diversified ETF.

- When prices are high, your $500 buys fewer shares.

- When prices are low, your $500 buys more shares.

Over time, your average cost per share decreases.

Why DCA Works So Well During Crashes

- Removes emotional timing decisions

You don’t have to guess when to buy — you buy automatically. - Takes advantage of falling prices

Lower prices mean more shares per dollar invested. - Creates discipline and consistency

Investing becomes a habit, not an emotional reaction. - Reduces regret

You won’t feel bad about “buying too early” or “too late” — because you buy continuously.

A Real-World Example

Suppose you invest $1,000 per month during a crash:

| Month | Market Level | Shares Bought |

|---|---|---|

| Jan | 100 | 10 |

| Feb | 80 | 12.5 |

| Mar | 60 | 16.7 |

| Apr | 70 | 14.3 |

| May | 90 | 11.1 |

Total invested: $5,000

Total shares: ~64.6

Average cost per share: ~$77.4

If the market later returns to 100, your investment is worth ~$6,460 — even though the market only returned to its original level.

Retirement Accounts and DCA

Most retirement plans — such as:

- 401(k) (USA)

- IRA / Roth IRA (USA)

- RRSP (Canada)

- Superannuation (Australia)

- ISA / SIPP (UK)

— already use DCA automatically through payroll contributions.

This is one reason why long-term retirement investors often outperform market timers.

8. Step 4: Focus on High-Quality Assets

Not all investments are equal — especially during crashes. A strong market crash investing strategy focuses on quality, not speculation.

When markets fall, weak businesses fail, while strong businesses survive and often thrive.

What Is a “High-Quality” Investment?

Let’s define this clearly.

🔹 High-Quality Stocks

You can also compare strategies in our detailed Growth vs Value Investing guide to determine which approach suits your risk tolerance. A high-quality stock typically has:

- Strong Balance Sheet

- Low debt relative to assets and earnings

- Plenty of cash reserves

- Consistent Profits and Cash Flow

- Generates money even during economic downturns

- Not dependent on constant borrowing

- Competitive Advantage (Moat)

- Brand strength

- Network effects

- Patents

- Cost leadership

- Trusted Management

- Proven leadership

- Ethical governance

- Clear strategy

- Diversified Revenue

- Global operations

- Multiple products or services

Examples:

Large consumer goods companies, healthcare companies, technology platforms, infrastructure providers, and utilities often display these characteristics.

🔹 High-Quality Funds and ETFs

For funds or ETFs, quality means:

- Broad diversification across countries, industries, and companies

- Low expense ratios (lower fees improve long-term returns)

- Long-term track record

- Transparent structure

Examples:

Broad market ETFs tracking the S&P 500, global stock indexes, or total market indexes.

🔹 High-Quality Bonds

For bonds, quality means:

- High credit rating (government or investment-grade corporate)

- Reliable interest payments

- Appropriate duration for your risk tolerance

High-quality bonds provide stability during crashes and help balance portfolio risk.

The Core Rule

During market crashes, quality survives — speculation dies.

Companies without profits, excessive debt, or fragile business models often fail during downturns. Quality businesses endure and recover.

9. Step 5: Build a Crash-Resistant Portfolio

If you truly want to know how to invest during a market crash, diversification is non-negotiable. A crash-resistant portfolio is not immune to losses — but it is designed to:

- Reduce volatility

- Recover faster

- Provide psychological comfort

- Support disciplined investing

Core Asset Classes Explained

Let’s define each major asset class clearly.

📈 Stocks (Equities)

Role: Long-term growth

Stocks represent ownership in companies. Over long periods, stocks historically provide the highest returns among major asset classes — but also the highest short-term volatility.

📉 Bonds (Fixed Income)

Role: Stability and income

Bonds are loans to governments or corporations. They pay interest and return principal at maturity. High-quality bonds tend to hold value or rise during stock market crashes.

💵 Cash

Role: Liquidity and opportunity

Cash provides safety, flexibility, and emergency coverage. It also allows you to invest when opportunities arise.

🏢 Real Assets (REITs, Commodities)

Role: Inflation protection

Real estate investment trusts (REITs) and commodities (like gold) often perform well during inflationary periods and provide diversification.

🧩 Alternatives (Optional)

Role: Diversification

Includes private equity, hedge funds, or other non-traditional assets. These are not necessary for most investors but can add diversification.

Example Balanced Portfolio (Moderate Risk)

- 60% Stocks (global, diversified)

- 25% Bonds

- 10% Real Assets

- 5% Cash

This portfolio:

- Grows over the long term

- Reduces volatility during downturns

- Provides liquidity for emergencies and opportunities

What Happens During a Crash?

- Stocks fall the most

- Bonds and cash provide stability

- Real assets may fluctuate

This naturally changes your asset allocation — and creates an opportunity to rebalance.

10. Step 6: Rebalance Instead of Retreating

Rebalancing means restoring your portfolio to its original asset allocation — regardless of market conditions. Rebalancing is a disciplined technique used by professionals when investing during a market crash.

What Is Rebalancing?

Suppose your target allocation is:

- 60% stocks

- 40% bonds

After a market crash:

- Stocks fall → now 45%

- Bonds rise → now 55%

Your portfolio is now out of balance.

Rebalancing means:

- Selling some bonds

- Buying more stocks

This returns your portfolio to:

- 60% stocks

- 40% bonds

Why Rebalancing Works

Rebalancing forces you to:

- Sell high (assets that have increased in value)

- Buy low (assets that have fallen in value)

This happens automatically — without emotional decision-making or market prediction.

When to Rebalance

- Time-based: Once or twice per year

- Threshold-based: When an asset class deviates by 5–10% from its target

Either approach works — consistency matters more than precision.

11. Step 7: Use Cash Strategically — Not Emotionally

Cash plays a crucial role in financial stability — but it must be used wisely.

Strategic Uses of Cash

- Emergency Fund

Covers unexpected expenses without selling investments. - Opportunity Fund

Allows you to invest during downturns when prices are low. - Portfolio Stabilizer

Reduces volatility and improves psychological comfort.

Emotional Uses of Cash

- Hoarding indefinitely out of fear

- Waiting forever for the “perfect” moment

- Avoiding investing due to anxiety

These behaviors protect you emotionally — but harm you financially.

A Balanced Approach

Hold enough cash to:

- Sleep well

- Cover emergencies

- Invest during opportunities

But not so much that:

- Inflation erodes your purchasing power

- You miss long-term growth

12. Step 8: Avoid Trying to Time the Bottom When You Invest During a Market Crash

Trying to buy at the exact market bottom is tempting — but extremely dangerous. Investors who try to perfectly time the bottom often fail at how to invest during a market crash effectively.

Why Timing the Bottom Fails

- No one knows the bottom

Not even professional investors. - Fear prevents action

Even when prices are low, fear often stops people from buying. - Markets recover before news improves

By the time things “feel safe,” prices have already risen.

The Cost of Missing the Best Days

Studies show that missing just a few of the best days in the market dramatically reduces long-term returns. According to historical S&P 500 return data , long-term equity markets have delivered strong returns despite multiple recessions and crashes.

Example:

If you invested in the S&P 500 for 30 years:

- Stay fully invested → ~10% annual return

- Miss the 10 best days → returns drop by more than 50%

And many of those best days occur during or immediately after crashes.

The Better Strategy

Stay invested.

Keep investing.

Rebalance.

Let time do the work.

13. Step 9: Learn from Past Crashes

History offers powerful lessons.

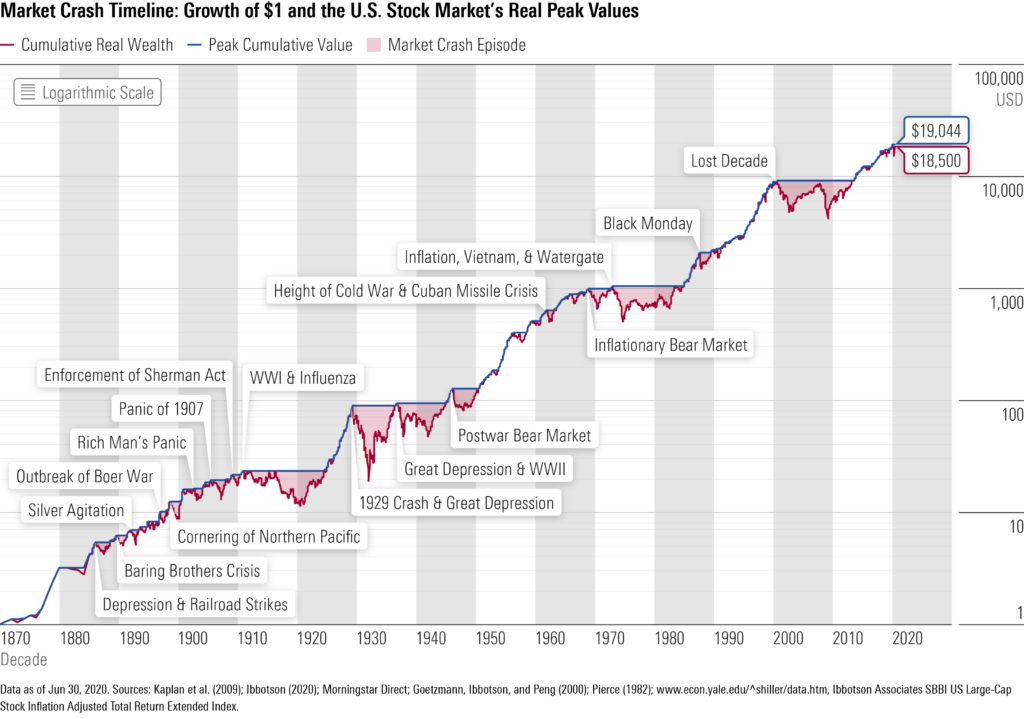

📉 The Great Depression (1929–1932)

- Markets fell ~89%.

- It took many years to recover — but recovery did occur.

- Long-term investors who stayed invested eventually achieved significant wealth.

📉 1970s Stagflation

- High inflation and slow economic growth.

- Stock markets struggled for years.

- Eventually, markets adapted and entered strong bull markets.

📉 Dot-Com Crash (2000–2002)

- Many technology stocks collapsed.

- Speculative companies disappeared.

- High-quality tech companies survived and became industry leaders.

📉 Global Financial Crisis (2008–2009)

- Markets fell ~50%.

- Massive fear dominated.

- Within a decade, markets reached new all-time highs — repeatedly.

📉 COVID Crash (2020)

- Markets fell ~34% in weeks.

- Recovered in months.

- Led to one of the strongest bull markets in history.

The Pattern

Every crash feels like:

“This time is different.”

Every recovery proves:

It wasn’t.

14. Step 10: The Psychology of Staying Calm Under Pressure

Long-term investing success depends far more on behavior than on intelligence or technical skill. Emotional discipline is the hidden secret behind successful investing during a market crash.

🧘♂️ Limit News Consumption

Constant exposure to negative news increases anxiety and impulsive decisions.

Instead:

- Check markets weekly or monthly.

- Avoid daily monitoring.

- Focus on long-term goals.

🧾 Write an Investment Policy Statement (IPS)

An Investment Policy Statement is a written plan that defines:

- Your financial goals

- Your time horizon

- Your risk tolerance

- Your asset allocation

- Your rules during crashes

Example:

“During market downturns, I will continue investing, rebalance annually, and avoid selling due to fear.”

This document acts as your emotional anchor.

🕰️ Zoom Out

Daily charts show chaos.

Long-term charts show growth.

Looking at 20-, 30-, or 50-year charts reminds you that:

- Markets rise over time.

- Crashes are temporary.

- Compounding rewards patience.

🧠 Reframe Crashes

Instead of thinking:

“I’m losing money.”

Think:

“Assets are on sale.”

This mental shift transforms fear into opportunity.

🤝 Get Accountability

A financial advisor, coach, or disciplined friend can:

- Provide perspective

- Prevent emotional mistakes

- Reinforce long-term discipline

15. A Simple Crash Investment Checklist

Use this checklist whenever markets fall:

☐ Emergency fund intact

☐ No high-interest debt

☐ Long-term goals unchanged

☐ Continue regular investments

☐ Rebalance portfolio

☐ Focus on quality assets

☐ Avoid emotional decisions

☐ Limit news consumption

☐ Review but don’t react

16. Frequently Asked Questions About How to Invest During a Market Crash

17. Final Thoughts: How to Invest During a Market Crash for Long-Term Wealth

Market crashes are not punishments — they are transfers of wealth.

They transfer wealth from:

- The emotional → to the disciplined

- The impatient → to the patient

- The fearful → to the strategic

If you:

✔ Protect your financial foundation

✔ Invest consistently

✔ Focus on quality

✔ Stay diversified

✔ Control your emotions

Then crashes become your greatest allies — not your enemies.

In 10, 20, or 30 years, you may look back and realize:

The best investments you ever made were during the times you felt the most afraid.

That is the paradox of investing — the moments that feel worst emotionally often deliver the best financial results.