Value Investing Explained: The Complete Guide to Finding Undervalued Stocks and Building Long-Term Wealth

Introduction

Value investing is one of the most respected and successful investment strategies ever developed. For nearly a century, investors have used value investing principles to identify undervalued companies, minimize risk, and generate substantial long-term returns.

Many of the world’s greatest investors—including Benjamin Graham and Warren Buffett—built their fortunes using this strategy.

Unlike speculative trading, which focuses on short-term price movements, value investing focuses on determining what a business is truly worth and purchasing it only when it is available at a discount.

For investors in Tier-1 countries such as the United States, Canada, the United Kingdom, Australia, Germany, France, Switzerland, Japan, and Singapore, value investing remains one of the most effective methods for building wealth over decades.

This comprehensive guide explains every important concept, term, strategy, example, and case study associated with value investing.

What Is Value Investing?

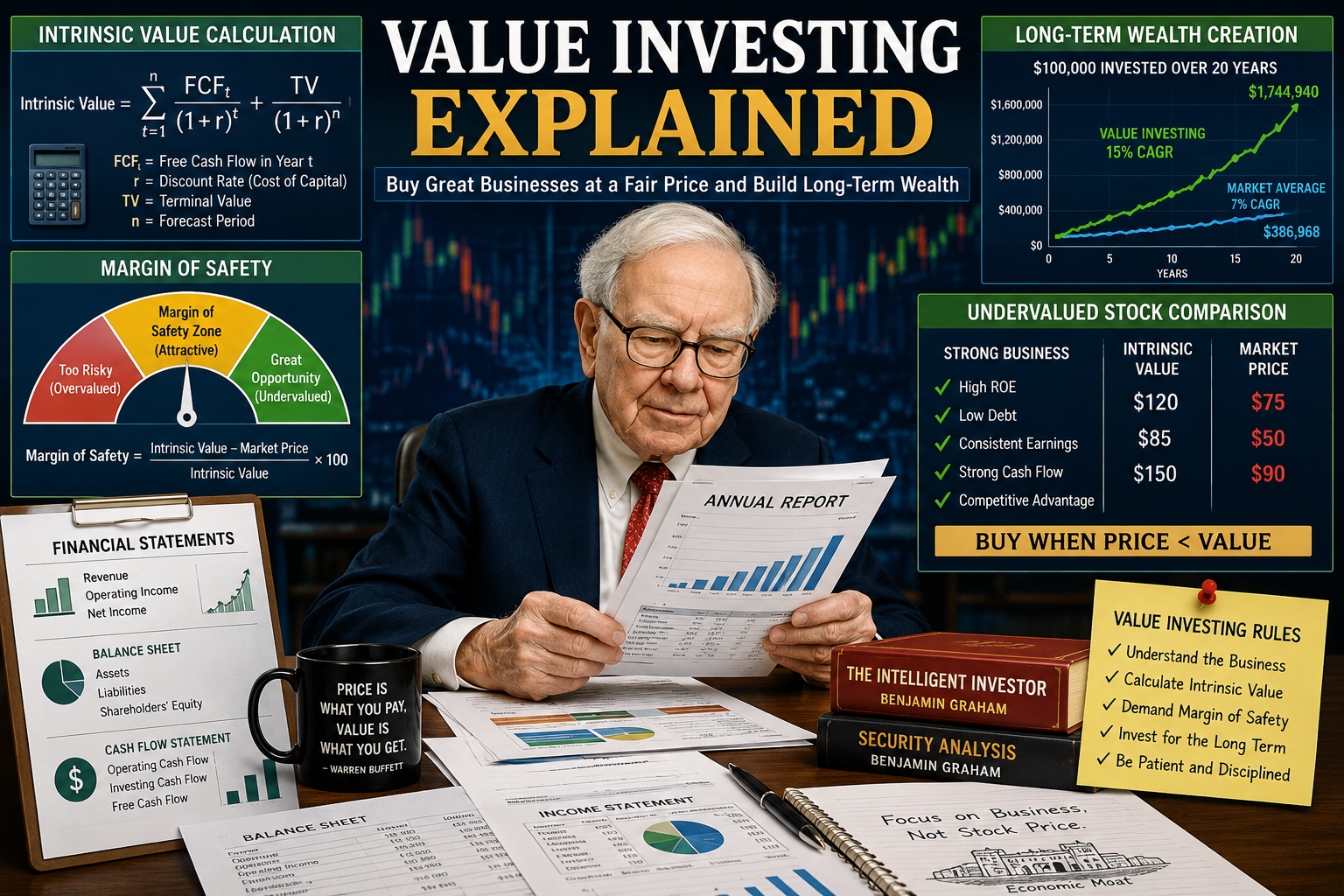

Value investing is an investment strategy that involves buying stocks that trade below their intrinsic value.

Let’s break down this definition word by word.

Value

Value means the true worth of something.

For example:

Imagine a house worth $500,000 based on its location, condition, and rental income.

If the owner is forced to sell quickly and offers it for $400,000, the house has not become less valuable.

Instead, it is temporarily underpriced.

Value investors look for the same situation in the stock market.

Investing

Investing means allocating money today with the expectation of receiving greater value in the future.

Examples include:

- Stocks

- Bonds

- ETFs

- Real estate

- Private businesses

The goal is wealth creation rather than short-term speculation.

Intrinsic Value

Intrinsic value is the actual economic value of a company based on:

- Earnings

- Assets

- Cash flow

- Growth potential

- Competitive advantages

Intrinsic value differs from market price.

This distinction forms the foundation of value investing.

Why Does Value Investing Work?

Many people assume stock markets are perfectly efficient.

However, markets are run by humans.

Humans experience:

- Fear

- Greed

- Optimism

- Pessimism

- Panic

- Euphoria

These emotions often cause stock prices to become disconnected from business fundamentals.

A value investor takes advantage of these pricing mistakes.

Example

A company may be worth $100 per share.

Because of temporary bad news:

- Stock price falls to $70.

The company remains fundamentally strong.

A value investor sees an opportunity.

The Origin of Value Investing

The concept was developed by Benjamin Graham during the 1920s and 1930s.

After witnessing the devastating effects of the Wall Street Crash of 1929, Graham sought a disciplined method of investing.

His research led to two revolutionary ideas:

- Intrinsic Value

- Margin of Safety

These principles later influenced Warren Buffett.

Understanding Intrinsic Value

Intrinsic value is arguably the most important concept in value investing.

It answers one simple question:

What is this company actually worth?

Intrinsic value considers:

Earnings

How much profit the company generates.

Cash Flow

How much actual cash enters the business.

Assets

What the company owns.

Liabilities

What the company owes.

Future Growth

Potential expansion opportunities.

Competitive Position

Ability to maintain profitability.

Market Price vs Intrinsic Value

One of the most important distinctions investors must understand is:

| Term | Meaning |

|---|---|

| Market Price | What investors currently pay |

| Intrinsic Value | What the company is actually worth |

The two are rarely identical.

Example

Company Value:

$150 per share

Current Market Price:

$100 per share

Discount:

$50

This difference creates opportunity.

Margin of Safety Explained

Margin of Safety is the cornerstone of value investing.

It protects investors from:

- Forecasting errors

- Economic downturns

- Unexpected business problems

Formula

Margin of Safety = Intrinsic Value − Market Price

Example

Intrinsic Value:

$200

Market Price:

$140

Margin of Safety:

$60

Percentage:

30%

The larger the margin of safety, the lower the risk.

Characteristics of a Good Value Stock

Value investors typically look for companies with:

Strong Balance Sheets

Healthy financial condition.

Consistent Earnings

Stable profitability over many years.

Positive Cash Flow

Regular cash generation.

Low Debt

Manageable financial obligations.

Durable Competitive Advantage

Long-term protection from competitors.

Attractive Valuation

Reasonable stock price relative to earnings.

Important Financial Metrics Used by Value Investors

Price-to-Earnings Ratio (P/E Ratio)

One of the most popular valuation metrics.

Definition

Shows how much investors are paying for every dollar of earnings.

Formula

P/E = Stock Price ÷ Earnings Per Share

Example

Stock Price:

$50

EPS:

$5

P/E Ratio:

10

Investors are paying $10 for every $1 of earnings.

Price-to-Book Ratio (P/B Ratio)

Measures stock price relative to net assets.

Formula

P/B = Market Price ÷ Book Value

Useful for:

- Banks

- Insurance companies

- Financial institutions

Free Cash Flow (FCF)

Cash remaining after business expenses and capital expenditures.

Strong free cash flow often indicates:

- Financial strength

- Dividend sustainability

- Growth capacity

Return on Equity (ROE)

Measures management effectiveness.

Formula

ROE = Net Income ÷ Shareholder Equity

Higher ROE generally indicates better capital allocation.

Economic Moats

A concept popularized by Warren Buffett.

An economic moat is a sustainable competitive advantage.

Examples include:

Brand Power

Examples:

- Coca-Cola

- Nike

Network Effects

Examples:

- Visa

- Mastercard

Switching Costs

Examples:

- Enterprise software providers

- Cloud infrastructure providers

Customers find it difficult to switch.

The Psychology Behind Value Investing

Value investing is as much about behavior as finance.

Most investors:

- Buy when prices rise

- Sell when prices fall

Value investors do the opposite.

During Bull Markets

Most investors become greedy.

Value investors become cautious.

During Bear Markets

Most investors panic.

Value investors search for bargains.

This psychological discipline often creates superior returns.

Case Study 1: Warren Buffett and Coca-Cola

One of the greatest value investing examples occurred in 1988.

Buffett identified Coca-Cola as:

- Globally recognized

- Highly profitable

- Consistently growing

The market underestimated the company’s future earnings power.

Berkshire Hathaway purchased a massive stake.

Over the following decades:

- Stock price increased dramatically

- Dividends grew substantially

- Investment value multiplied many times

Lesson:

Great businesses can still become undervalued.

Case Study 2: American Express Crisis

During the 1960s, American Express faced a major scandal.

Investors panicked.

Stock prices declined significantly.

Buffett analyzed the situation and concluded:

- Brand remained strong

- Customers remained loyal

- Long-term economics were intact

He invested heavily.

The market eventually recovered.

Lesson:

Temporary problems often create value opportunities.

Case Study 3: The Global Financial Crisis

During the 2008 financial crisis:

- Markets crashed

- Fear dominated headlines

- Quality companies traded at huge discounts

Many value investors purchased shares in:

- Banks

- Industrial firms

- Consumer companies

When markets recovered:

- Returns were extraordinary

Lesson:

The best opportunities often appear during periods of maximum fear.

Value Investing vs Growth Investing

| Factor | Value Investing | Growth Investing |

|---|---|---|

| Focus | Undervalued companies | Fast-growing companies |

| Risk | Lower | Higher |

| Dividends | Common | Less common |

| Time Horizon | Long-term | Long-term |

| Valuation | Cheap | Expensive |

Neither approach is inherently better.

Many successful investors combine both.

Value Investing vs Speculation

Value investing and speculation are often confused.

They are completely different.

| Value Investing | Speculation |

|---|---|

| Based on fundamentals | Based on predictions |

| Long-term focus | Short-term focus |

| Lower risk | Higher risk |

| Intrinsic value analysis | Market timing |

Value investors purchase businesses.

Speculators purchase price movements.

Common Value Investing Strategies

Deep Value Investing

Buying stocks trading significantly below intrinsic value.

Often found during recessions.

Dividend Value Investing

Focuses on:

- Undervalued stocks

- Reliable dividend payments

Popular among retirees.

Contrarian Investing

Going against market sentiment.

Buying when others are fearful.

Quality Value Investing

Combines:

- Strong companies

- Attractive valuations

Many modern investors prefer this approach.

Red Flags Value Investors Avoid

Excessive Debt

High debt increases bankruptcy risk.

Declining Industry

Cheap stocks in dying industries may remain cheap forever.

Accounting Problems

Financial statement irregularities can indicate fraud.

Weak Cash Flow

Profits without cash generation can be dangerous.

Building a Value Investing Portfolio

A diversified portfolio may include:

Large-Cap Companies

Stable and established businesses.

Dividend Stocks

Provide recurring income.

International Stocks

Increase diversification.

Value ETFs

Offer broad exposure.

Examples include funds tracking value indexes.

Modern Value Investing in Tier-1 Countries

Today’s markets differ from Graham’s era.

Investors now have access to:

- Real-time financial data

- AI-powered analysis

- Advanced valuation models

- Global diversification

Yet the core principles remain unchanged:

- Determine intrinsic value.

- Buy below intrinsic value.

- Demand a margin of safety.

- Hold patiently.

Common Mistakes New Value Investors Make

Confusing Cheap With Value

A low stock price does not automatically mean a bargain.

Ignoring Business Quality

Even cheap companies can fail.

Lack of Patience

Value investing may take years to work.

Following Market Hype

Popular stocks are not always good investments.

Overtrading

Frequent buying and selling often reduces returns.

Benefits of Value Investing

Lower Downside Risk

Margin of safety provides protection.

Proven Historical Success

Used successfully for nearly a century.

Long-Term Wealth Creation

Encourages disciplined investing.

Reduced Emotional Decision-Making

Focus remains on business fundamentals.

Challenges of Value Investing

Requires Patience

Returns may take years.

Requires Analysis

Financial statement knowledge is essential.

Market Can Stay Irrational

Undervalued stocks may remain undervalued for extended periods.

Not Every Cheap Stock Recovers

Research remains critical.

How Beginners Can Start Value Investing

Step 1:

Learn financial statements.

Step 2:

Understand valuation metrics.

Step 3:

Study successful investors.

Step 4:

Analyze businesses rather than stock charts.

Step 5:

Focus on long-term ownership.

Step 6:

Maintain diversification.

Step 7:

Invest consistently.

The Golden Rules of Value Investing

- Buy businesses, not ticker symbols.

- Focus on intrinsic value.

- Demand a margin of safety.

- Ignore short-term market noise.

- Think independently.

- Be patient.

- Manage risk first.

- Avoid emotional decisions.

- Continuously learn.

- Let compounding work over decades.

Conclusion

Value investing remains one of the most powerful wealth-building strategies available to investors in Tier-1 countries. Developed by Benjamin Graham and perfected by Warren Buffett, it focuses on a simple but powerful principle:

Buy a dollar’s worth of value for less than a dollar.

By understanding intrinsic value, margin of safety, financial statements, economic moats, and investor psychology, individuals can make more informed investment decisions and avoid the emotional traps that harm most investors.

While markets constantly evolve, the fundamental principles of value investing remain timeless. Investors who consistently purchase high-quality businesses at attractive prices and hold them patiently are often rewarded with significant long-term wealth, making value investing one of the most enduring and respected approaches in modern finance.